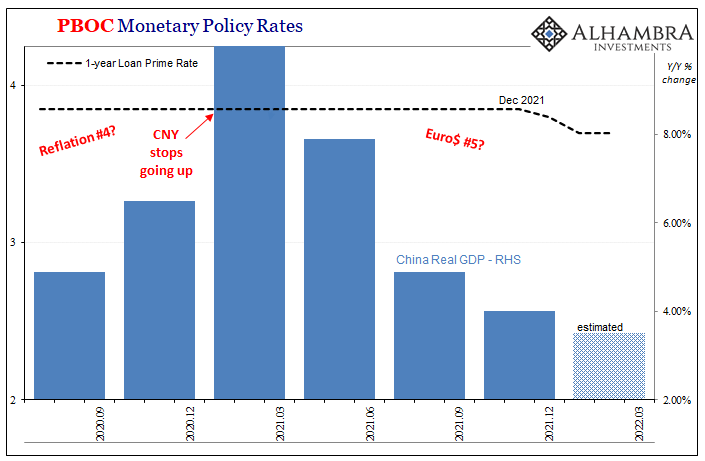

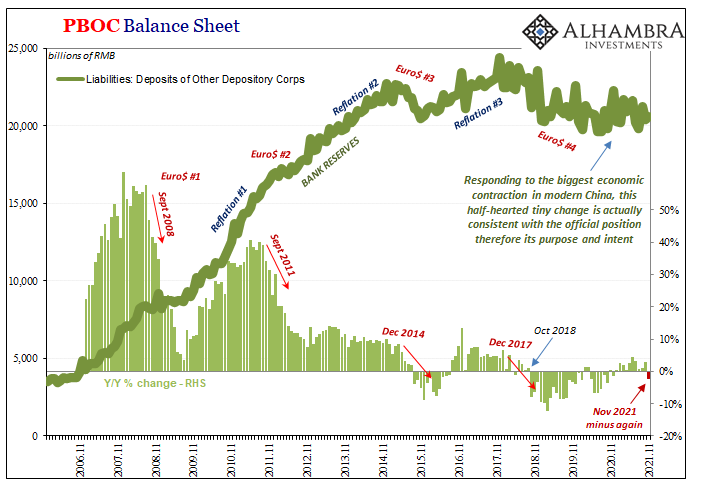

This week will almost certainly end up as a clash of competing interest rate policy views. Everyone knows about the Federal Reserve’s upcoming, the beginning of what is intended to be a determined inflation-fighting campaign for a US economy that American policymakers worry has been overheated. The FOMC will vote to raise the federal funds range (and IOER plus RRP) for the first time since December 2018 Over in China, however, it’s nearly certain to be the opposite. The Chinese central bank, PBOC, has already cut several of its benchmarks dating back to last year. In December 2021, authorities there surprised many (vast majority) of Western observers when they reduced required reserves (RRR) and then the MLF leading to a decline in the LPR (loan prime rate). The

Topics:

Jeffrey P. Snider considers the following as important: $CNY, 5.) Alhambra Investments, bonds, China, currencies, dollar shortage, economy, EuroDollar, Featured, Federal Reserve/Monetary Policy, lending, loans, Markets, newsletter, PBOC, rate cuts, RMB

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| This week will almost certainly end up as a clash of competing interest rate policy views. Everyone knows about the Federal Reserve’s upcoming, the beginning of what is intended to be a determined inflation-fighting campaign for a US economy that American policymakers worry has been overheated. The FOMC will vote to raise the federal funds range (and IOER plus RRP) for the first time since December 2018

Over in China, however, it’s nearly certain to be the opposite. The Chinese central bank, PBOC, has already cut several of its benchmarks dating back to last year. In December 2021, authorities there surprised many (vast majority) of Western observers when they reduced required reserves (RRR) and then the MLF leading to a decline in the LPR (loan prime rate). |

|

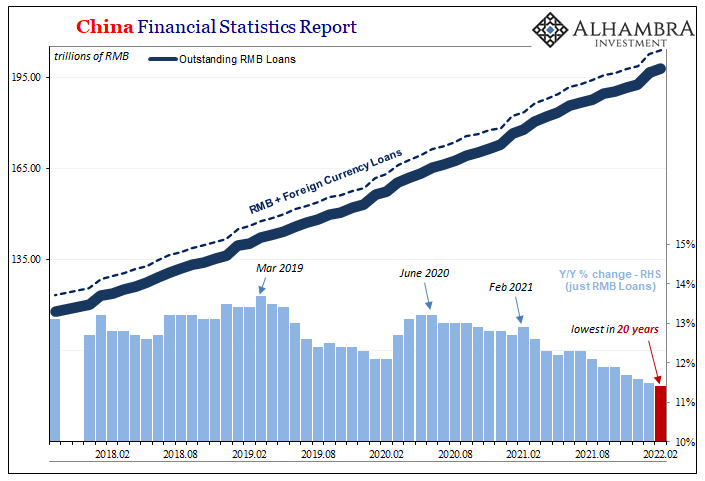

| The latter was followed by a second reduction in January. Last month, the PBOC held off on a third rate cut hoping that the Chinese situation had, to use Li Keqiang’s term, stabilized.According to the latest from China’s Financial Statistics Report on lending during February 2022, those hopes were dashed.

Overall RMB loans to domestic borrowers increased 11.4% year-over-year, rising to 197.9 trillion rmb. These numbers may sound solid, but that annual growth rate was less than anticipated while also representing the lowest yearly change in just about two decades (May 2002). |

|

| Worse, this continues a trend which showed up – like a whole bunch of problems – in March 2021. Total RMB loan growth has been steadily decelerating for an entire year already, with PBOC policy shifts including those rate cuts mentioned above not producing the “stability” government authorities have been publicly seeking.

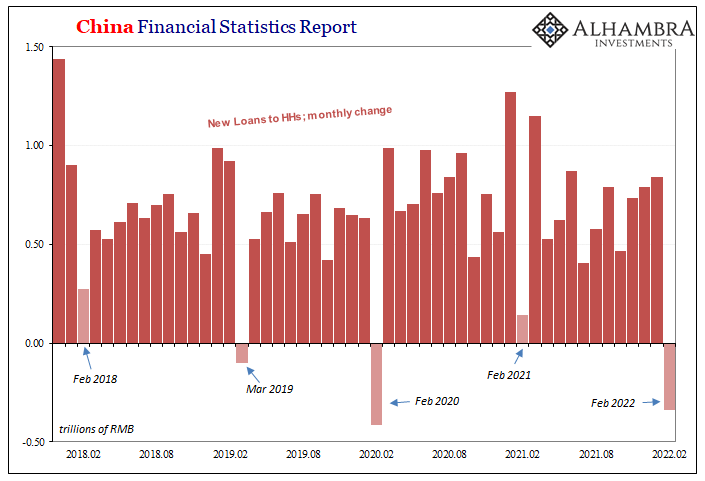

On the contrary, the February Financial Statistics Report contained a nasty downside surprise which partly explains the topline RMB loan figures. Loans to households declined sharply, falling by 336 billion rmb from January (below). Though January to February is typically a seasonal low point as far as new lending is concerned, this year’s change is far closer to February 2020 (COVID lockdown) than February 2018 (starting into Euro$ #4) or even March 2019 (the downturn from Euro$ #4). |

|

| The reason for the decline in loans to households was the first ever drop in long-term credit for the category – a proxy for mortgages therefore a worrisome sign about the real potential for the Chinese system given its (former) reliance on real estate for much of its upward growth and ability to better weather volatile global economic factors.As a result, it is now widely expected the PBOC will announce more rate cuts (MLF most likely, and very likely another RRR reduction, too) this week before early next Monday morning (Beijing time) a third drop in the LPR. |  |

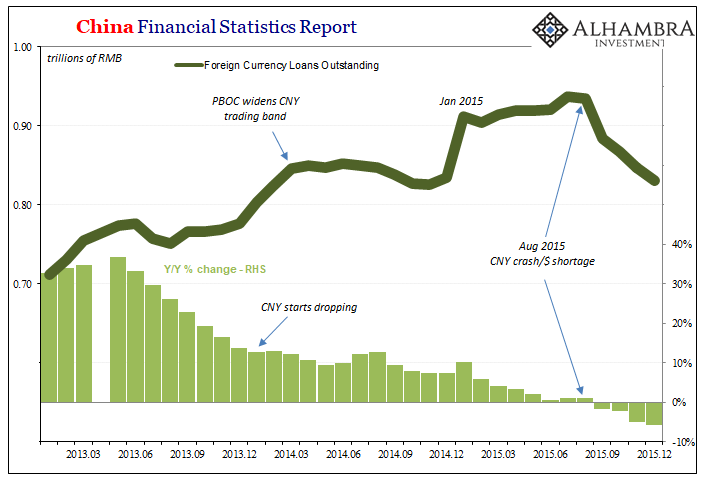

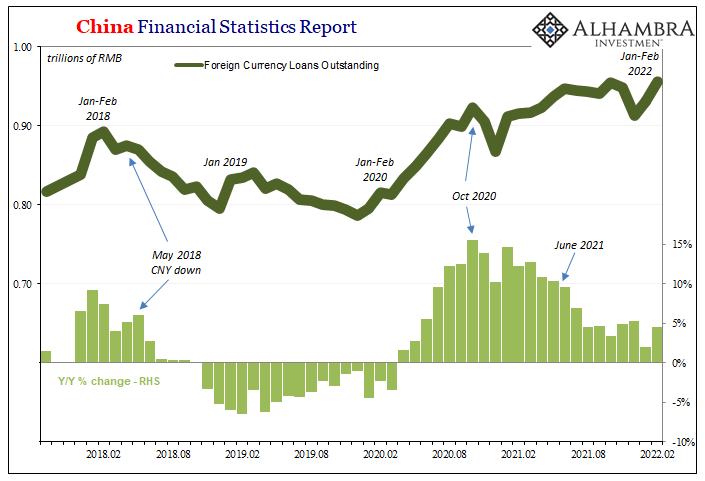

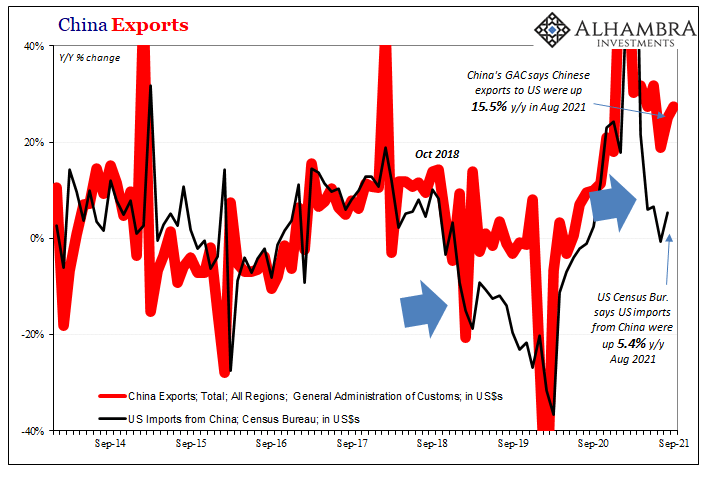

| China’s Financial Statistics also contain more data to complete a still-developing global downside case – foreign currency loans to domestic Chinese borrowers. Though it is a much smaller subset of total financial credit, the trend(s) in lending by foreign currency merely reinforces the links between what otherwise might appear to be distinctly different systems.Going back two prior “cycles”, from the middle months of 2013 (the “summer of SHIBOR”) right onto 2015, the dramatic swings in foreign currency loans matched near perfectly the full-on financial and economically destructive development of Euro$ #3 and all its various symptoms – especially its worst parts in the final few months of 2015.

Begun a year and a half prior, foreign lenders clearly became more and more adverse just as similar indications (dollar shortage) were expressed in US$ markets worldwide – from flattening yield and money curves, up to and including the US$’s exchange value against CNY and many others. While many here in the West remained utterly convinced of US economic and financial risks tipped toward overheating and inflation throughout 2014 and even into 2015, this had been another clear and corroborating sign of the opposite potential worldwide (eventually). |

|

| The setup and reversal in 2018 (Euro$ #4) was even more extreme, including the downdraft in CNY and the global consequences which followed in a matter of months.The Chinese then moving opposite to Mr. Powell (like his predecessors) were dealing with weakness and worse which has consistently reached China first before plowing into the rest of the global system.

Markets sided with China, or at least understood what was happening to the Chinese was almost certain to happen here before too much longer regardless of the Federal Reserve’s oft-stated confidence in its projections going the other way. As you can see above, foreign currency loans into China have noticeably decelerated again going back to last summer (along with a bunch of other things), indicating global eurodollar setbacks already building throughout the last half of last year (consistent with other data such as TIC). |

|

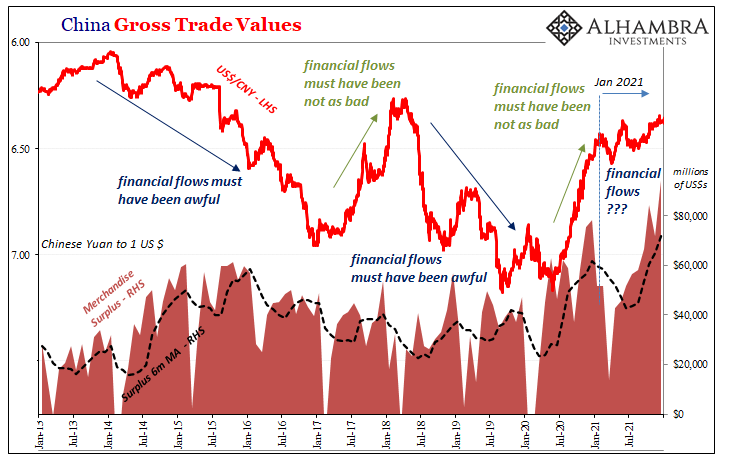

Remember, too, China’s trade surplus therefore merchandise dollar inflows remained at historic levels meaning that foreign currency credit inflows are to some significant extent higher than they would otherwise have been on a financial basis alone. That’s also true for the January-February months when many of these loans get done, typically a positive start in them each and every year (2022 no exception).

Put all these together, and you’ve got China’s credit system continuing to decelerate dramatically along with a global credit/money proxy indicating the same for the world’s financial shape as a whole. The second half of 2021 wasn’t a continuation of massive inflation potential, rather it was a downside economic drive which didn’t stop at the end of the calendar.

On the contrary, there’s every reason to believe the downside risks are what’s rising even if alongside the US CPI, which is why Chinese policy rates will keep moving in the “wrong” direction sparking what should be a very troubling disconnect. Though there may be an ocean in between, despite the Fed’s intentions there isn’t actually much economic or financial distance.

Only time.

You Might Also Like

The Hawks Circle Here, The Doves Win There

The Hawks Circle Here, The Doves Win There

2022-01-26

We’ve been here before, near exactly here. On this side of the Pacific Ocean, in the US particularly the situation was said to be just grand. The economy was responding nicely to QE’s 3 and 4 (yes, there were four of them by that point), Federal Reserve Chairman Ben Bernanke had said in the middle of 2013 it was becoming more than enough, creating for him and the FOMC coveted breathing space so as to begin tapering both of those ongoing programs.A full and complete recovery he believed was on schedule if not getting way ahead of it.

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)

2022-01-14

A full part of the inflation hysteria, the first one, was the dollar’s looming crash. The currency was, too many claimed, on the verge of collapse by late 2017, heading downward and besieged on multiple fronts by economics and politics alike.

Taper Rejection: Mao Back On China’s Front Page

Taper Rejection: Mao Back On China’s Front Page

2021-12-29

Chinese run media, the Global Times, blatantly tweeted an homage to China’s late leader Mao Zedong commemorating his 128th birthday. Fully understanding the storm of controversy this would create, with the Communist government’s full approval, such a provocation has been taken in the West as if just one more chess piece played in its geopolitical game against the United States in particular.No. The Communists really mean it. Mao’s their guy again.

No. Let's recall that Chairman Mao• slaughtered thousands of his political adversaries in early 1930s• exterminated hundreds of thousands of landlords in early 1950s• starved 45 million peasants to death in Great Leap Forward• murdered 2 million in the Cultural Revolution— TheSeeqer (@TheSeeqer) December 26, 2021

When Deng Xiaoping

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

2021-12-25

If there is a better, more fitting way to head into the Christmas holiday in the United States than by digging into the finances and monetary flows of the People’s Bank of China, then I just don’t want to know what it is. Contrary to maybe anyone’s rational first impression that this is somehow insane, there’s much we can tell about the state of the world, the whole world and its “dollars”, right from this one key data source.

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

2021-11-03

Bring on the tantrum. Forget this prevaricating, we should want and expect interest rates to get on with normalizing. It’s been a long time, verging to the insanity of a decade and a half already that keeps trending more downward through time. What’s the holdup?

Short Run TIPS, LT Flat, Basically Awful Real(ity)

Short Run TIPS, LT Flat, Basically Awful Real(ity)

2021-10-28

Over the past week and a half, Treasury has rolled out the CMB’s (cash management bills; like Treasury bills, special issues not otherwise part of the regular debt rotation) one after another: $60 billion 40-day on the 19th; $60 billion 27-day on the 20th; and $40 billion 48-day just yesterday.

Inflating Chinese Trade

Inflating Chinese Trade

2021-10-15

There was never really any answer given by the Chinese Communists for why their own export data diverged so much from other import estimates gathered by its largest trading partners. Ostensibly different sides of the same thing, it’s not like anyone asked Xi Jinping to weigh in; they report what numbers they have and consider them authoritative.

Tapering Or Calibrating, The Lady’s Not Inflating

Tapering Or Calibrating, The Lady’s Not Inflating

2021-10-07

We’ve got one central bank over here in America which appears as if its members can’t wait to “taper”, bringing up both the topic and using that particular word as much as possible. Jay Powell’s Federal Reserve obviously intends to buoy confidence by projecting as much when it does cut back on the pace of its (irrelevant) QE6.

Tags: $CNY,Bonds,China,currencies,dollar shortage,economy,EuroDollar,Featured,Federal Reserve/Monetary Policy,lending,Loans,Markets,newsletter,PBOC,rate cuts,RMB