It’s a broken a record, the macro stylus stuck unable to move on, just skipping and repeating the same spot on the vinyl. Since Xi Jinping’s lockdowns broke it, as it’s said, when Xi is satisfied there’s zero COVID he’ll release the restrictions and that will fix everything. The economy will go right back to good, like flipping a switch. Where have we heard that before? Everywhere, actually, but especially in China. Whether early last year, last August, and now again over the past few months, focus has been (intentionally) maintained on overly aggressive pandemic policies as the catchall for every bad number and vibe. . Just last week, the country’s National Bureau of Statistics (NBS) reported a substantial decline for Industrial Profits, typically a particularly

Topics:

Jeffrey P. Snider considers the following as important: $CNY, 5.) Alhambra Investments, China, currencies, economy, Featured, Federal Reserve/Monetary Policy, industrial profits, Markets, newsletter, PBOC, Xi Jinping

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| It’s a broken a record, the macro stylus stuck unable to move on, just skipping and repeating the same spot on the vinyl. Since Xi Jinping’s lockdowns broke it, as it’s said, when Xi is satisfied there’s zero COVID he’ll release the restrictions and that will fix everything. The economy will go right back to good, like flipping a switch.

Where have we heard that before? Everywhere, actually, but especially in China. Whether early last year, last August, and now again over the past few months, focus has been (intentionally) maintained on overly aggressive pandemic policies as the catchall for every bad number and vibe. |

. |

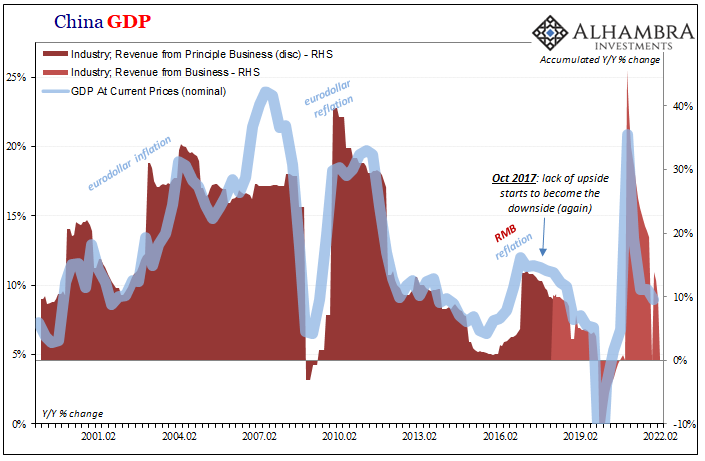

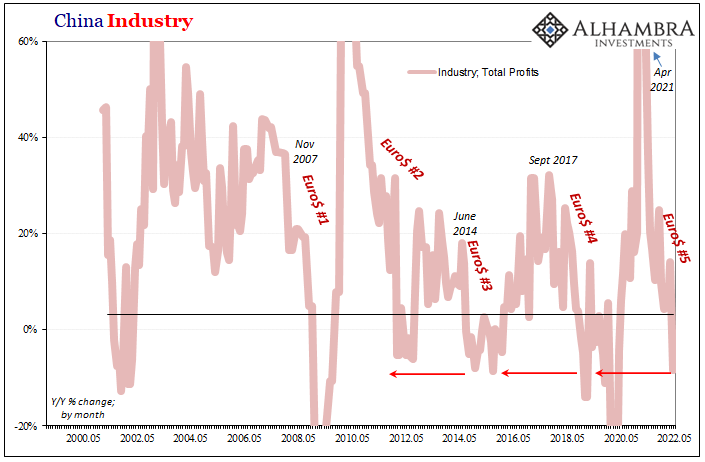

| Just last week, the country’s National Bureau of Statistics (NBS) reported a substantial decline for Industrial Profits, typically a particularly ominous macro signal. Despite all attempts to move away from the configuration, as you can plainly see (below) China’s entire economy remains – at root – an industrial/export-driven machine. Industry does well, predicated upon global demand, the Chinese as a whole do well.

Industry revenues in April 2022? Just 1.5% y/y. Total profits? A harmful -8.5%. |

. |

Officials at the NBS, however, quite purposefully draw our focus to the lockdown aspect of these plainly undesirable industrial. Don’t fret, just give it a few months:

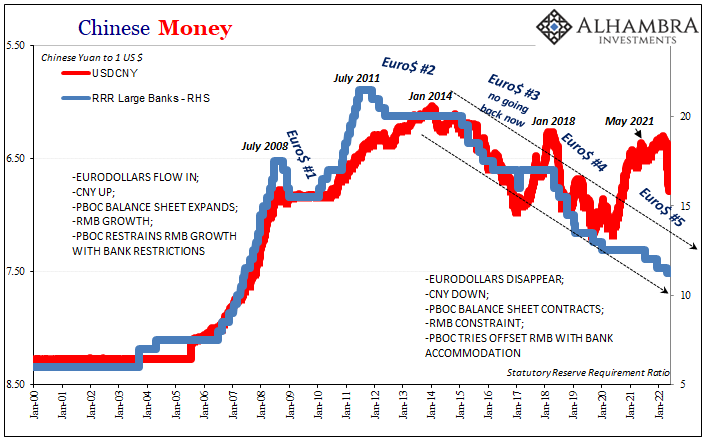

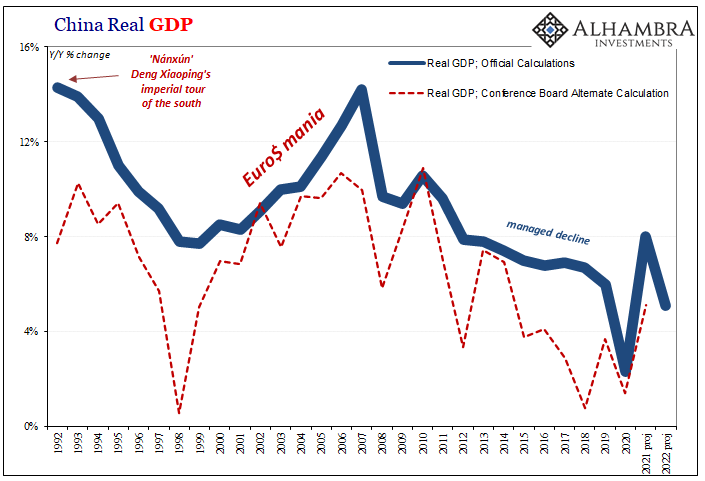

However, you would only assume that once the quarantines are lifted the economy goes back to doing well. And we are all repeatedly invited to make such an assumption. But was it actually doing well before any of the lockdowns were implemented? That, not the lockdowns, is the thing. By every single measure, every account the NBS spits out, China has been on a more than yearlong slide. Industrial profits like revenues didn’t just start falling off with the Shanghai closures. Instead, they really began to fall down right when Euro$ #5 showed up. |

. |

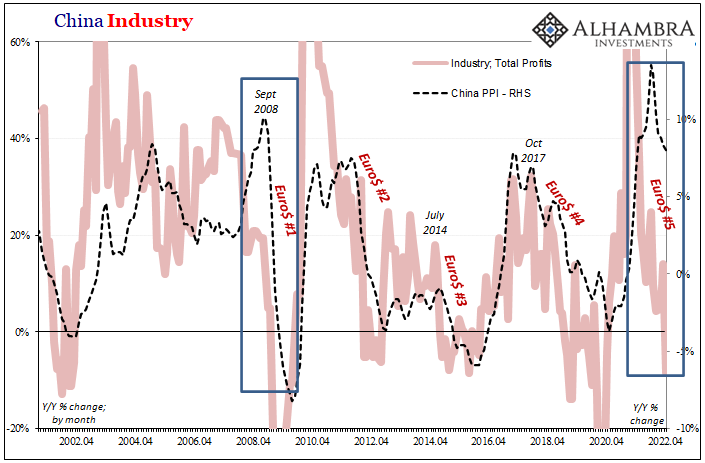

| Even producer prices in China appear to be reaching a reckoning of the prolonged demand weakening; in a way that’s reminiscent of the summer of 2008 (I’m not claiming the Great “Recession” and GFC1 are being repeated in 2022, only pointing out that Chinese industry and price pressures haven’t historically diverged but when they do they converge on industrial demand rather than “inflation”).

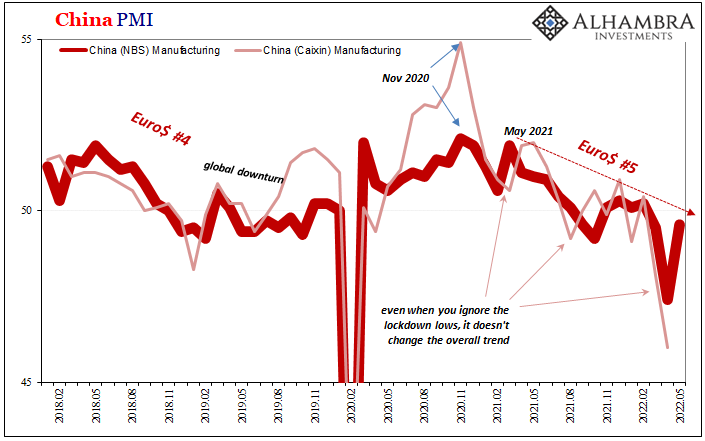

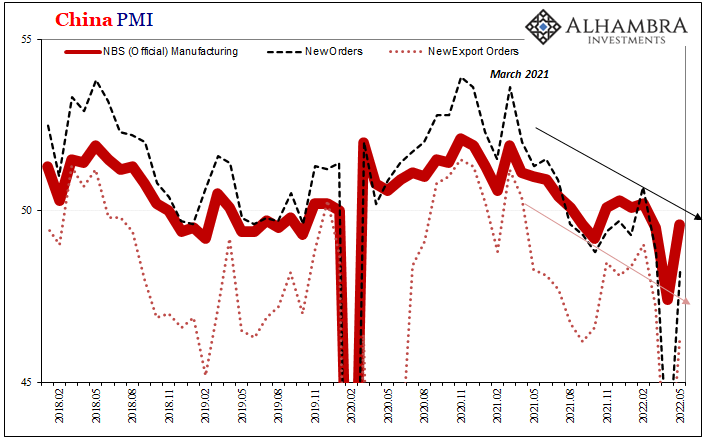

Thus, if you focus only on the lows presented by the one-off months when Xi’s regime is most restrictive, you miss the larger, otherwise unmistakable (and unmistakably worse than 2018-19) inclination – which, again, I believe is the true point. And it is one that gets replicated series after series. Whereas industrial profits and revenues were yet to begin shaking off their Shanghai in the April figures, the NBS is now turning the calendar toward May data when Xi’s mood apparently improved. Over the weekend, the official PMI figures showed that, yep, April was bad when China was “fighting the coronavirus” then May got better as the pandemic situation purportedly recovered. |

. |

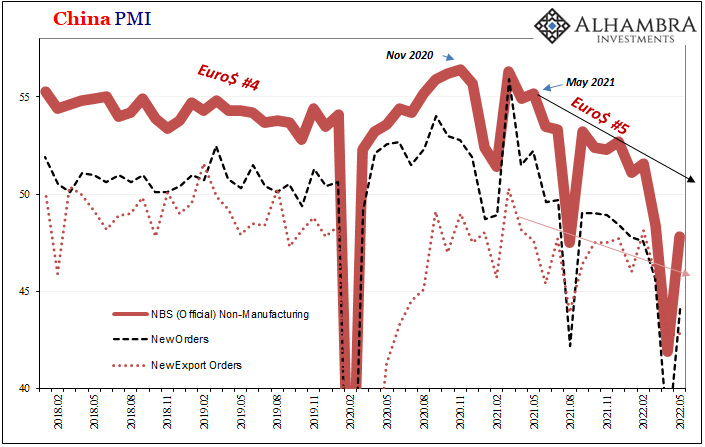

| According to the NBS, its General PMI (comprehensive output) rose sharply to 48.4 from its April awful of 42.7. The non-manufacturing rebounded from 41.9 in April to 47.8 for May; manufacturing 47.4 to 49.6.If that’s all you see, an April to May improvement, you might indeed extrapolate growing positives further into June and beyond. Maybe even full, complete, and world-giving recovery.

Yet, April to May isn’t the priority to consider; rather, it’s all the months leading up to April which advise therefore caution about what trend to follow mostly likely will follow. The pre-lockdown baseline remains as clear as ever, and that is the global problem. |

. |

| While it may seem impressive, the General PMI’s almost six-point rise, for example, at 48.4 it’s still less than March’s 48.8 and nowhere close to the ~53 or 54 level which in 2019 was already too-low being consistent with a worldwide downturn into recession.

Ignore every one of those prior extreme downside, single-month lockdown lows. Put them totally out of your mind, follow instead from way back to the earliest parts of last year and then post-May 2021. Zero-COVID didn’t make that line, the months when that pursuit was driven to insanity merely struck new and temporary lows underneath it. |

. |

. |

|

| Every instance when quarantines were imposed, it had been widely claimed China’s economy would bounce right back. It never once did; the slide continued and continues to this month.

Nobody is asking why the bounce-back doesn’t happen, and mostly because everyone on both sides of the Pacific, apparently, insist on deriving their views and expectations of and for the global economy from various CPIs; the globe can’t be working its way decidedly into this kind of weak-demand recession, it is, we’re told, being blistered with inflation from one corner to the next. Ironically, though, not according to China’s CPI. The latter also consistent with all the other NBS data which says lockdowns aren’t the issue and never really have been. Weak and weakening demand independent of the pandemic, that’s what’s been in all the data since last year. Not a recent month of authoritarianism, more than a year of Euro$ #5 and all that goes with it. The politics of COVID aren’t driving China’s economy to lows, they are, once properly assessed, exposing the political (over)reactions to China’s irresistible wrong way condition. |

. |

You Might Also Like

Synchronized Not Coronavirus

Synchronized Not Coronavirus

2022-05-19

There is an understandable tendency to just write off this weekend’s disastrous Chinese data as nothing more than pandemic politics. After all, it has been Emperor Xi’s harsh lockdowns spreading like wildfire across China rather than any disease (why it has been this way, that’s another Mao-tter).

The (less) Dollars Behind Xi’s Shanghai of Shanghai

The (less) Dollars Behind Xi’s Shanghai of Shanghai

2022-04-25

What everyone is saying, because it’s convenient, is that China’s zero-COVID policies are going to harm the economy. No. Economic harm of the past is the reason for the zero-COVID policies. As I showed yesterday, the cracking down didn’t just show up around 2020, begun right out in the open years beforehand, born from the scattering ashes of globally synchronized growth.

Shanghai’s Current Plight Began in 2017

2022-04-23

The first chapters to China’s new story now playing out in Shanghai were written down in October 2017. Planning for them had begun years earlier, their author Xi Jinping requiring more research before committing them to paper. Communist authorities there had grown increasingly concerned about the lack of growth potential for its political system by then utterly dependent for a quarter-century on the economy growing.

China More and More Beyond ‘Inflation’

China More and More Beyond ‘Inflation’

2022-04-17

If only the rest of the world could have such problems. Chinese consumer prices were flat from February 2022 to March, even though gasoline and energy costs predictably skyrocketed. According to China’s NBS, gas was up 7.2% month-over-month while diesel costs on average gained 7.8%.

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed

2022-03-16

This week will almost certainly end up as a clash of competing interest rate policy views. Everyone knows about the Federal Reserve’s upcoming, the beginning of what is intended to be a determined inflation-fighting campaign for a US economy that American policymakers worry has been overheated.

The Hawks Circle Here, The Doves Win There

The Hawks Circle Here, The Doves Win There

2022-01-26

We’ve been here before, near exactly here. On this side of the Pacific Ocean, in the US particularly the situation was said to be just grand. The economy was responding nicely to QE’s 3 and 4 (yes, there were four of them by that point), Federal Reserve Chairman Ben Bernanke had said in the middle of 2013 it was becoming more than enough, creating for him and the FOMC coveted breathing space so as to begin tapering both of those ongoing programs.A full and complete recovery he believed was on schedule if not getting way ahead of it.

Taper Rejection: Mao Back On China’s Front Page

Taper Rejection: Mao Back On China’s Front Page

2021-12-29

Chinese run media, the Global Times, blatantly tweeted an homage to China’s late leader Mao Zedong commemorating his 128th birthday. Fully understanding the storm of controversy this would create, with the Communist government’s full approval, such a provocation has been taken in the West as if just one more chess piece played in its geopolitical game against the United States in particular.No. The Communists really mean it. Mao’s their guy again.

No. Let's recall that Chairman Mao• slaughtered thousands of his political adversaries in early 1930s• exterminated hundreds of thousands of landlords in early 1950s• starved 45 million peasants to death in Great Leap Forward• murdered 2 million in the Cultural Revolution— TheSeeqer (@TheSeeqer) December 26, 2021

When Deng Xiaoping

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

2021-12-25

If there is a better, more fitting way to head into the Christmas holiday in the United States than by digging into the finances and monetary flows of the People’s Bank of China, then I just don’t want to know what it is. Contrary to maybe anyone’s rational first impression that this is somehow insane, there’s much we can tell about the state of the world, the whole world and its “dollars”, right from this one key data source.

Tags: $CNY,China,currencies,economy,Featured,Federal Reserve/Monetary Policy,industrial profits,Markets,newsletter,PBOC,Xi Jinping