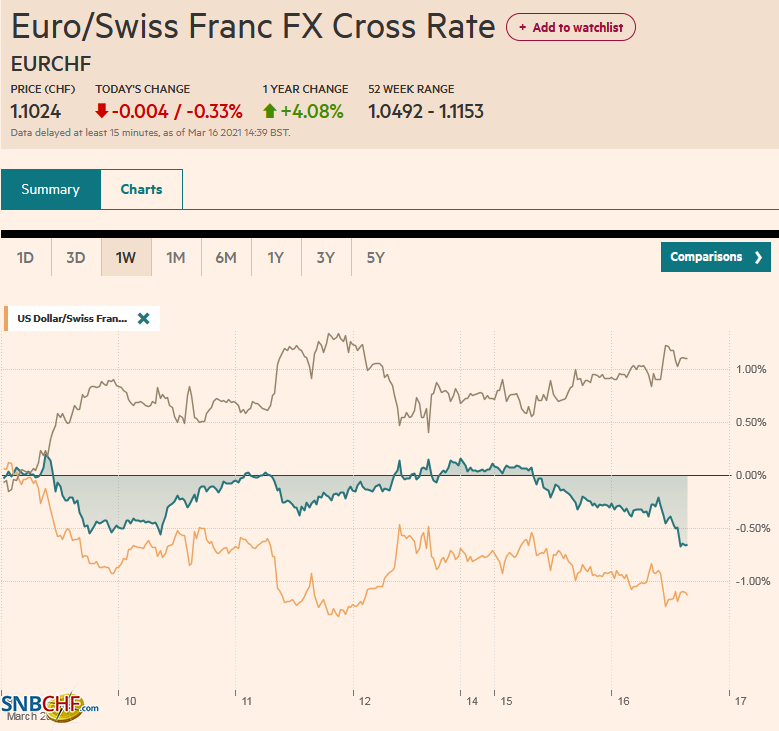

Swiss Franc The Euro has fallen by 0.33% to 1.1024 EUR/CHF and USD/CHF, March 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Yesterday’s new record highs in the S&P 500 and Dow Jones Industrial helped set the tone for today’s advance in the Asia Pacific region and Europe. The MSCI Asia Pacific Index snapped a two-day decline, with other major markets rising today. The Dow Jones Stoxx 600 had edged to new highs as it continues to approach the pre-pandemic high, which is a little less than 2% away. US shares are trading with a firmer bias. Arguably helped by the third consecutive decline in oil prices, benchmark yields are little changed in the US (~1.60%) and Europe. Australia and New Zealand’s 10-year

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Australia, capital flows, China, Currency Movement, Featured, newsletter, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.33% to 1.1024 |

EUR/CHF and USD/CHF, March 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

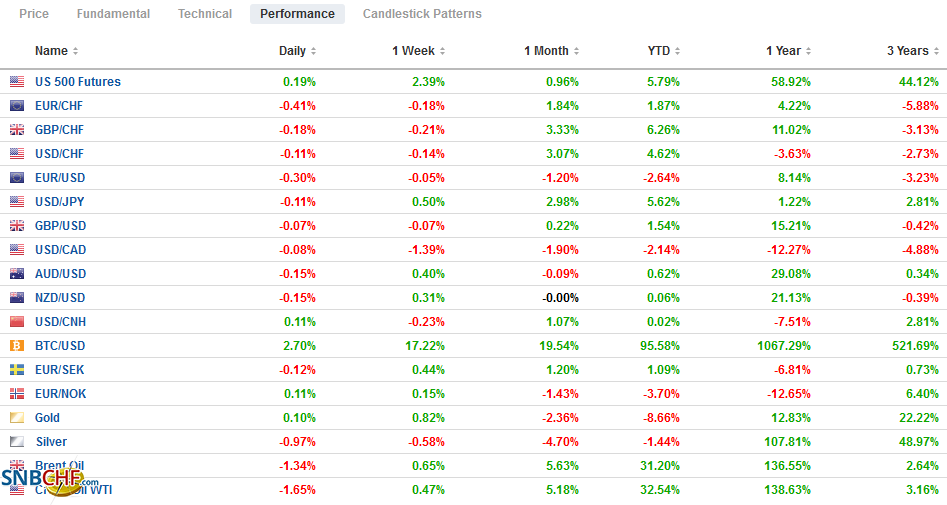

FX RatesOverview: Yesterday’s new record highs in the S&P 500 and Dow Jones Industrial helped set the tone for today’s advance in the Asia Pacific region and Europe. The MSCI Asia Pacific Index snapped a two-day decline, with other major markets rising today. The Dow Jones Stoxx 600 had edged to new highs as it continues to approach the pre-pandemic high, which is a little less than 2% away. US shares are trading with a firmer bias. Arguably helped by the third consecutive decline in oil prices, benchmark yields are little changed in the US (~1.60%) and Europe. Australia and New Zealand’s 10-year yields fell 8-10 bp. The dollar is mostly firmer. Sterling, the dollar-bloc, and the Norwegian krone are bearing the brunt, while the Swiss franc and Swedish krona are the most resilient. Emerging market currencies are mixed. Most of the liquid and accessible EM currencies, but the Turkish lira are trading heavily, and the JP Morgan Emerging Market Currency Index is giving back yesterday’s gains. Gold is trading quietly near last week’s high ($1740) |

FX Performance, March 16 - Click to enlarge |

Asia Pacific

The US Treasury’s International Capital report showed China bought nearly $23 bln of US Treasury bonds in January. It was the third month of purchases and the most since 2017. Its holdings stand at $1.095 trillion, the highest level since October 2019. Japan’s holdings of Treasuries increased by $25.4 bln, snapping a five-month divestment streak. These two largest holders of US Treasury bonds increased their holding by nearly $49 bln, which turns out to match the sales of Treasury bonds by the Caribbean banking centers, a proxy for hedge funds.

Outside of China’s apparent crackdown on Alibaba, forcing it shed of media assets, Australian developments dominate the news from the region today. First, the minutes from the recent central bank meeting tighten the link between policy and the labor market. The minutes indicated that it would take wage growth above 3% to be consistent with the inflation target, which is unlikely before 2024. It said it would re-evaluate the 3-year yield target later this year. The issue here is whether to continue to target the April 2024 bond or shift to the November 2024 bond. Second, reports indicate that Facebook has struck a multi-year revenue deal with News Corp and Sky after last year’s dispute. Third, US officials have formally linked its relations with China to Beijing’s economic coercion of Australia for the first time. Australian goods have been targeted by Beijing as a protest over Canberra’s pro-US foreign policy.

The dollar is in about a 20-pip range against the yen below JY109.30. Yesterday’s nine-month high was a little higher, near JPY109.35. As we have argued, at the risk of over-simplification, the key seems to be Treasuries and oil prices. The Australian dollar is trading heavier and set to test yesterday’s low near $0.7700, where a A$455 mln option is set to expire. The Aussie stalled near $0.7800 at the end of last week. A break of the $0.7690-area could signal a retest on last week’s low near $0.7620. The PBOC’s dollar fixing at CNY6.5029 was in line with the projections. The dollar is straddling the CNY6.50-level.

Europe

Formal Brexit is not even three months old, and the EU seeks a judicial decision on the UK’s delay in implementing part of the new trade agreement. Starting April 1, sending food from the rest of the UK to Northern Ireland, which remains part of the common market, required special customs paperwork. The UK argues this is temporary, operational steps done to minimize disruptions. The UK has unilaterally waived this provision and intends, according to reports, to do the same with parcels and claims it is temporary and operational measures done to minimize disruptions. The EC sees this in the context of UK threats last September to override part of the Northern Ireland Protocol. It began infringement proceedings then but dropped them after the Johnson Government retreated, which helped make possible the trade deal struck in December. Also, the EC is taking action under the dispute resolution mechanism of the treaty, which requires the formation of an arbitration panel.

| Meanwhile, UK and US 10-year yields are up around 60-70 bp this year, while the 10-year German Bund yield has risen barely 25 bp. This means that the UK premium over Germany has widened above 110 bp for the first time since October 2019. It has not been much above 120 bp since mid-2016. The UK premium over German for two-year money is pushing above 80 bp, which it has not done since Q1 20. It was closer to 120 bp on the eve of the pandemic. Sterling has appreciated by around 5% against the euro here in 2021. The inverse correlation (rolling 60 days) of the cross to the rate differential is the strongest in several years. That said, the cross has carved a shelf near GBP0.8550 over the last several days. The market may be turning a bit cautious ahead of the BOE meeting later this week. The 2-year Gilt yield is near the middle of the 5-15 bp range that has confined it over the past couple of weeks. |

Germany ZEW Economic Sentiment, March 2021(see more posts on Germany ZEW Economic Sentiment, ) Source: investing.com - Click to enlarge |

The euro barely reacted to news of the somewhat better-than-expected German ZEW survey (March expectations 76.6 vs. 71.2 in February, and the current assessment at -61.0 vs. -67.2). As other surveys have shown, expectations are running well ahead of the assessment of the current situation. Thus far, the euro has been confined to about a quarter of a cent below $1.1940. In fact, it continues to trade within last Friday’s range (~$1.1910-$1.1990). There is an option for almost 800 mln euros at $1.19 that expires today. Sterling is trading with a heavier bias. It is testing one-week lows near $1.3800. Some link it to position-squaring ahead of the BOE meeting. The March 5 low near $1.3780 was the low for cable since February 12. There is an expiring option for almost GBP800 mln at $1.3750. The euro is recovering against sterling today to push above the 20-day moving average (~GBP0.8625), which it has not closed above since January 7.

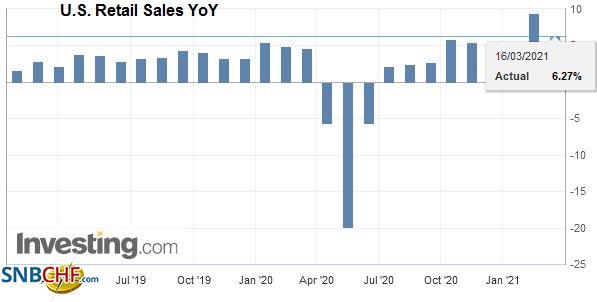

AmericaAhead of the FOMC outcome tomorrow, the US reports February retail sales and industrial output figures today. In some ways, the data is a bit irrelevant in the sense that the economy is going to be boosted by the new fiscal stimulus, and funds have already begun to be transferred. The Atlanta and NY Fed GDP trackers see Q1 GDP at 8.4% and 8.6%, respectively. Still, it is all but impossible for retail sales to match the 5.3% headline rise seen in January. It was fueled by a 10% month-over-month rise in income, thanks to government payments, which also saw a $1.3 bln paydown of consumer credit (the first decline since last May). We already know that auto sales were considerably weaker in February. The seasonally adjusted annual rate fell from 16.63 mln in January o 15.67 mln in February, the weakest since last August. We also already know that gasoline prices surged in February, accounting for around half the rise of February CPI. Even excluding gasoline, autos, food services, and building materials, the core may have contracted after a heady 6.0% rise in January. |

U.S. Retail Sales YoY, February 2021(see more posts on U.S. Retail Sales, ) Source: investing.com - Click to enlarge |

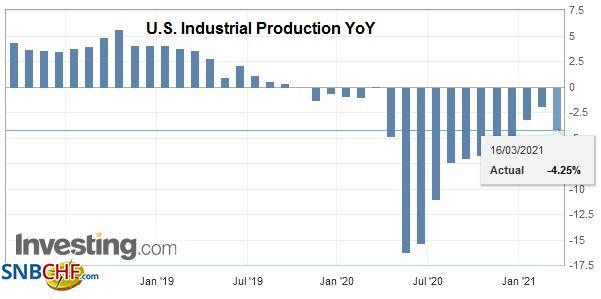

| The US lost 1.385 mln manufacturing jobs last March and April and gained 816k back before the end of the year (~59%). In January, when manufacturing output rose by 1.0% and industrial production increased by 0.9%, the US lost 14k manufacturing jobs. In February, manufacturing jobs increased by 21k, but manufacturing output is expected to have risen by only 0.2%, and the broader measure of industrial production may have increased by 0.3%. Once closely watched for signals of an over-heating economy, capacity utilization rate is forecast to ease to 75.5% in February from 75.6% in January. It stood at 77.2% at the end of 2019 and has not been above 80% since 2008. |

U.S. Industrial Production YoY, February 2021(see more posts on U.S. Industrial Production, ) Source: investing.com - Click to enlarge |

Canada and Mexico have light economic calendars today. Canada reports January portfolio flows ahead of tomorrow’s February CPI. Foreign investors bought a net of C$127 bln of Canadian securities last week, more than three-times more than in 2019 (~C$36 bln). In January 2020, foreign investors were net buyers of C$17 bln of Canadian securities. It is unlikely to have matched it this year. The US dollar fell to new three-year lows yesterday near CAD1.2440. It is consolidating in a narrow range below CAD1.2500 now. Yesterday’s high was near CAD1.2515, and resistance extends toward CAD1.2520. A break of it could see CAD1.2550-CAD1.2560. The focus in Mexico is on next week’s central bank meeting and the new oil discovery. The dollar is trading within the range seen at the end of last week. The upper end of the range is in the MXN20.93 area, and the lower end of the range is a little below MXN20.60. Meanwhile, the Mexican government has indicated it will challenge last week’s court decision to suspend the recent electricity law. Brazil reports FGV inflation figures today ahead of tomorrow’s central bank meeting. Most economists expect a 50 bp increase in the Selic rate to 2.5%.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-03-15

Update March 15 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.3 bn. compared to last week, this means the SNB is selling euros and dollars.

FX Daily, February 4: Negative Rates and the Bank of England: Having Your Cake and Eating it Too

FX Daily, February 4: Negative Rates and the Bank of England: Having Your Cake and Eating it Too

2021-02-04

Overview: The euro has been sold through $1.20 for the first time since December 1 and has now given back roughly half of the gains scored from the US election (~$1.16) to the early January high (~$.1.2350). More broadly, the greenback is bid against most of the major currencies, with the Australian dollar more resilient after reported record iron ore exports and all but a handful of emerging market currencies.

FX Daily, January 22: Faltering Friday

FX Daily, January 22: Faltering Friday

2021-01-22

Fear that social restrictions may have to be broadened and extended is helping spur a wave of profit-taking and de-risking, which has also been encouraged by disappointingly high-frequency data. The equity rally seemed to falter a bit in the US, as the S&P 500 eked out a minor 0.03% gain yesterday.

FX Daily, December 10: Brexit and US Stimulus are Unresolved as Attention Turns to the ECB

FX Daily, December 10: Brexit and US Stimulus are Unresolved as Attention Turns to the ECB

2020-12-10

Overview: US threats to break-up Facebook and the stalled stimulus talks spurred profit-taking in US shares yesterday and is dampening enthusiasm today. The MSCI Asia Pacific Index fell for the third time this week, and Europe’s Dow Jones Stoxx 600 is little changed.

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

2020-12-02

The selling pressure that drove the dollar lower yesterday has abated, and the greenback is paring yesterday’s loss, though the dollar-bloc currencies are showing some resilience. EC negotiator Barnier briefed ministers that the same three issues that have bedeviled the trade talks with the UK remain unresolved (fisheries, level playing field, and a conflict resolution mechanism).

FX Daily, November 20: US Treasury-Fed Dispute Spurs Handwringing but Immediate Market Impact was Exaggerated

FX Daily, November 20: US Treasury-Fed Dispute Spurs Handwringing but Immediate Market Impact was Exaggerated

2020-11-20

Overview: News that the stimulus talks between the House Democrats and Senate Republicans was the excuse traders were looking for to extend the US equity gains yesterday, but shortly after the close, confirmation that Treasury was not going to agree to extend several Fed facilities sent stocks reeling.

FX Daily, November 12: Nervous Calm in the Capital Markets

FX Daily, November 12: Nervous Calm in the Capital Markets

2020-11-12

There is a nervous calm in the capital markets today. The equity rally in the Asia Pacific region stalled to end an eight-day rally, though the Nikkei’s rally remains intact.

FX Daily, October 9: Animal Spirits Return

FX Daily, October 9: Animal Spirits Return

2020-10-09

Overview: The on-again-off-again fiscal stimulus in the US is back on as the White House now supports a broad stimulus program, but not as big as the Democrats $2.2 trillion package. It is the narrative being cited as the rebuilding of risk appetites is the wobble earlier in the week.

Tags: #USD,Australia,capital flows,China,Currency Movement,Featured,newsletter,U.K.