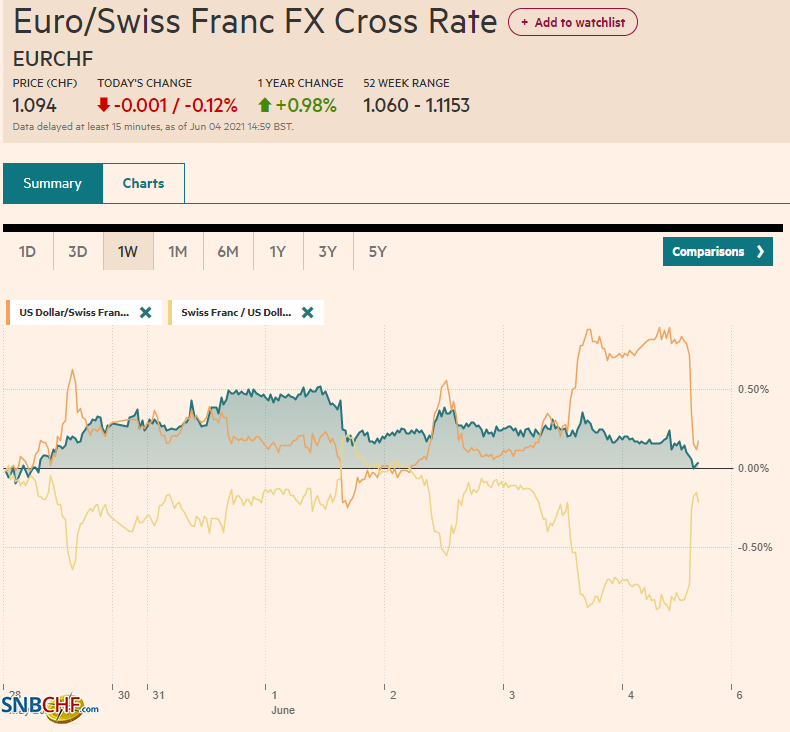

Swiss Franc The Euro has fallen by 0.12% to 1.094 EUR/CHF and USD/CHF, June 04(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Stronger than expected US employment data, ahead of today’s monthly report and compromise proposal on corporate tax by the White House to help secure a deal on infrastructure sent US bond yields and the dollar high. Late dollar shorts were forced to cover. The greenback is mixed now, with the yen, sterling, and Antipodeans slightly firmer. The Norwegian krone, Canadian dollar, and euro are still heavy. The dollar is rising against most emerging market currencies, though, of note, the Turkish lira is stabilizing after losing about 1.25% yesterday, its largest loss in four weeks. The

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, Brazil, Chile. Taxes, China, Currency Movement, EUR/CHF, Featured, G7, India, jobs, Mexico, newsletter, Russia, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.12% to 1.094 |

EUR/CHF and USD/CHF, June 04(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Stronger than expected US employment data, ahead of today’s monthly report and compromise proposal on corporate tax by the White House to help secure a deal on infrastructure sent US bond yields and the dollar high. Late dollar shorts were forced to cover. The greenback is mixed now, with the yen, sterling, and Antipodeans slightly firmer. The Norwegian krone, Canadian dollar, and euro are still heavy. The dollar is rising against most emerging market currencies, though, of note, the Turkish lira is stabilizing after losing about 1.25% yesterday, its largest loss in four weeks. The JP Morgan Emerging Market Currency Index is slipping for the second consecutive session and is practically flat on the week. China, Australia, and New Zealand equities rose ahead of the weekend, but most other markets in the Asia Pacific region fell, while Tokyo was mixed. European bourses are mixed, with the Dow Jones Stoxx 600 hovering around the record high set on Tuesday. US futures are little changed, and the 10-year Treasury yield is around 1.63%, about a three basis point increase on the week. The two-year yield is poking above 16 bp for the first time in three weeks. European bonds are quiet. Note that rating decisions are expected today from Moody’s for Russia and Turkey, while Fitch assesses Italy and DBRS, Germany. Gold, which had traded as high as $1910 yesterday, extended the biggest drop in four weeks and fell to almost $1856 before finding a bid in Asia. Even if little changed, oil prices are firm, with the July WTI contract hovering around $69 a barrel, consolidating a 4.25% gain this week. |

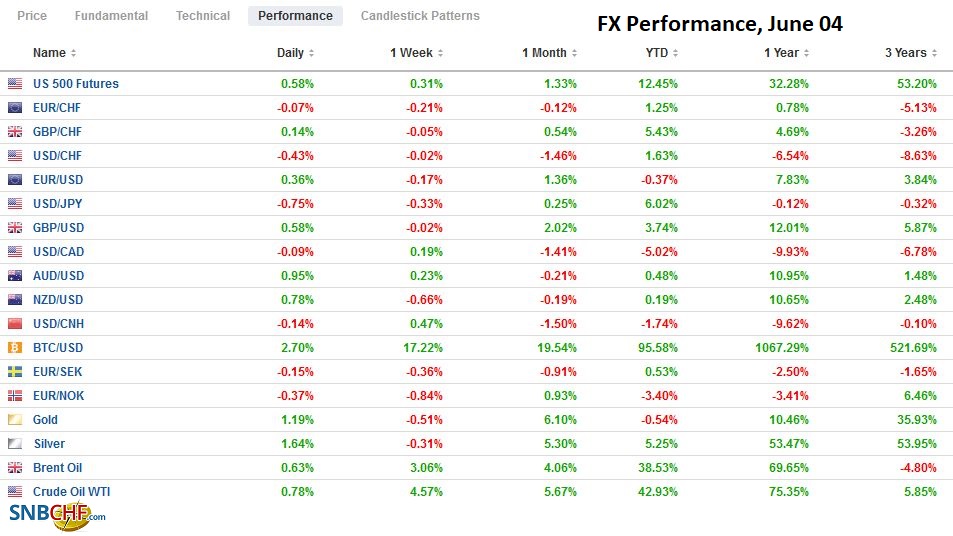

FX Performance, June 04 - Click to enlarge |

Asia Pacific

Japan’s household spending in April was stronger than expected, rising 13% year-over-year. The acceleration from 6.2% in March illustrates the powerful base effect. On a seasonally adjusted basis, spending rose by a minor 0.1%, though it is the third consecutive monthly increase. The extended emergency into June and the weakness in income point to continued challenges ahead. Many economists expect the world’s third-largest economy may be contracting still. On the other hand, the pace of vaccinations is accelerating, and a stronger recovery is expected in H2.

As widely anticipated, the Reserve Bank of India kept its repo at 4% but adjusted other dimensions of its monetary policy. It announced a Q3 bond-buying of INR1.2 trillion (~$16.4 bln) after completing INR1 trillion purchases this quarter. The central bank also extended its liquidity facility for businesses especially hit hard by the pandemic. As a result, the fiscal year’s GDP forecast was cut to 9.5% from 10.5%. The RBI now sees inflation finishing the year just above 5%. The latest print, for April, stood at 4.3%.

The US will prohibit new purchases of equities in 59 Chinese companies as of August 2. This looks like a net add of 11 new businesses from what was inherited from the previous administration. The Biden administration has put the initiative on stronger legal footing and made the policy clearer and more transparent. It will be run by the US Treasury, with input by State and Defense Departments. It will be updated on a rolling basis.

The dollar rose to almost JPY110.35 in early Asia before stalling. It is holding above JPY110.00, and there is an expiring option for $440 mln at JPY109.90. The attempt to rechallenge the year’s high set at the end of March near JPY111 appears to require a further increase in US yields.

The Australian dollar consolidated yesterday’s sell-off that brought it to its lowest level since mid-April, a little below $0.7650. Yesterday’s fall, about 1.3%, was the largest since mid-May. The next important support is in the $0.7580-$0.7600 area.

The greenback rose against the Chinese yuan for the fourth session this week. The cumulative gain of about 0.66% was the largest since last September. The dollar approached the 20-day moving average (~CNY6.4140) for the first time since mid-April. We had suggested potential into the gap from May 24-25 found between CNY6.4150 and CNY6.4180. A move above there targets the CNY6.4400-CNY6.4550 area. Today’s fixing was the tightest this week. At CNY6.4072, it compares with the median forecast in Bloomberg’s survey of CNY6.4074.

Europe

The G7 finance minister meets today. The focus is on coordinating the tax reform position that can be presented to the G20 and OECD. The US is downplaying expectations. As we discuss below, the minimum tax of the revised US proposal of 15% needs to be understood within the context of US domestic politics. Previously, the OECD had been discussing a minimum rate of 12.5%, which would have avoided the pushback by Ireland. There seems to be greater interest in Europe to address the problem that some companies with a large internet presence do not pay taxes to local authorities for local sales. There does appear to be an agreement to reform this process and not just apply it to US tech giants, but the thresholds of revenues and profits appear to still be debated. Separately, the UK host is pushing hard for an agreement to impose some environmental impact/risks reporting by large businesses.

Yesterday’s announcement that one of Russia’s sovereign wealth funds would complete its shift away from the US dollar had little market impact. It seemed a more symbolic defiant move ahead of the Biden-Putin meeting on June 16. To be sure, it is not Russia abandoning the dollar as much as it has been the US sanction regime that has tightened. The National Well-Being Fund will shift its dollar holdings, estimated to be less than $35 bln to the central bank. No market operation is necessary. The central bank manages the allocation of its reserves and has been authorized to buy gold too. Although there is a perennial fear that the dollar’s reserve role will change, the fact of the matter is that as of the end of last year, foreign central banks held more dollars than ever before in reserves (~$7 trillion). The US Treasury’s TIC data, which is not comprehensive, showed Russia’s Treasury bond holdings at $4 bln in March, down from $10 bln at the end of 2019 and $102.5 bln at the end of 2017. We argue that a move out of Treasuries and into European bonds and gold comes at the cost of yield, transparency, and liquidity.

The euro peaked on Monday near $1.2255. It is testing the $1.2100 area in late morning turnover in Europe. There is a 1.14 bln euro option at $1.21 that expires a little after the US jobs report. Today could be the fourth consecutive losing session, and yesterday’s loss was the biggest since April 30. The next target is around $1.2050, a (38.2%) retracement of the rally since the March 31 low. Below there, support is expected in the $1.1985-$1.2000 area. The $1.2140 area offers the initial cap.

Sterling posted a bearish outside down day yesterday, but follow-through selling was limited to a few ticks, and it has returned above $1.4100. It is holding below the 20-day moving average (~$1.4140) for the first time since mid-April. It needs to resurface above it to stabilize the tone into next week.

United StatesTo boost the chances of forging a deal with Republicans on a substantial infrastructure bill, the White House offered to amend its call to unwind Trump’s tax cuts on corporations and lift the tax schedule back to 28%. The problem with the tax hike is not that Republicans oppose it. Rather, it is that Biden has not persuaded all of the Democrat Senators of the merit. The compromise is a 15% minimum tax–there is no minimum now, but the average effective tax rate is of profitable businesses is even lower, according to some estimates. We had underscored the linkage between Biden’s domestic agenda and the reversal of the US position at the OECD/G20. Biden first proposed a 21% minimum corporate tax rate. The lack of sufficient support spurred a compromise of a 15% global minimum. The G7 finance ministers are coalescing around this now. |

U.S. Participation Rate, May 2021(see more posts on U.S. Participation Rate, ) Source: Investing.com - Click to enlarge |

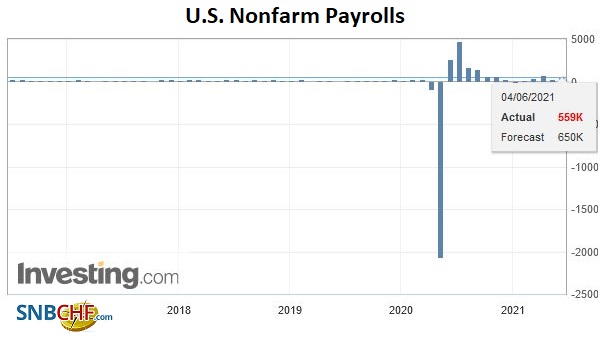

U.S. Nonfarm Payrolls, May 2021(see more posts on U.S. Nonfarm Payrolls, ) Source: Investing.com - Click to enlarge |

|

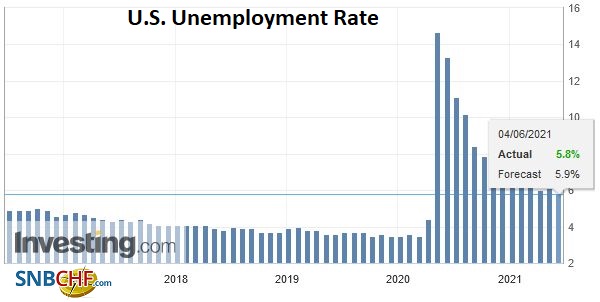

U.S. Unemployment Rate, May 2021(see more posts on U.S. Unemployment Rate, ) Source: Investing.com - Click to enlarge |

|

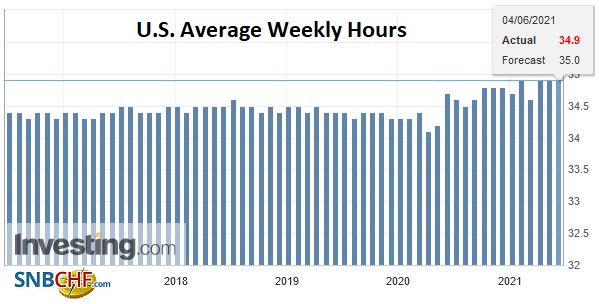

U.S. Average Weekly Hours, May 2021(see more posts on U.S. Average Weekly Hours, ) Source: Investing.com - Click to enlarge |

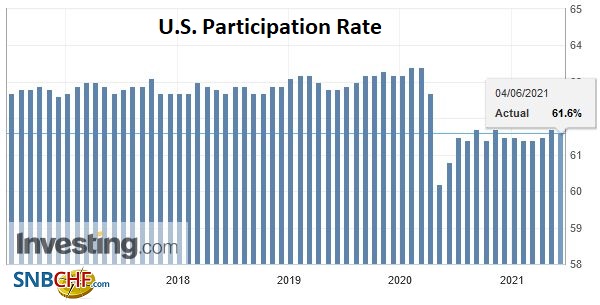

The unexpectedly mediocre April job report presaged a string of disappointing data that included retail sales, industrial production, housing starts, durable goods orders, and personal expenditures. Even under normal times, employment data can be volatile and subject to statistically significant revisions. While the market often does not focus on data revisions, a large upward revision to the April series coupled with a robust May report would be a powerful cocktail. Note that there have been more references to talking about tapering at the coming meetings since the big miss in the April report. Just like the Fed is looking through the near-term uptick in inflation, it is looking through the volatility of the monthly employment report. The four-week moving average of weekly jobless claims has halved since late last year. They remain elevated but significant progress has been made. The median forecast in Bloomberg’s survey has crept up and now is just north of 670k. The surge in the ADP private-sector estimate to 978k was above expectation but partly blunted by the downward revision to the April series (to 654k from 742k). It is still a multiple of the government’s initial estimate of 218k private-sector job growth. Confidence that the combination of fiscal/monetary stimulus and the widespread vaccination and re-open is accelerating growth, we look for a strong report and upward revisions to the April estimate. Like last time, though, the initial move in the markets may be a head fake.

Canada’s April employment report was also disappointed. It lost 207k jobs, of which nearly 130k were full-time positions. It is expected to have shed employment again last month. If it does, the Bank of Canada may temper its rhetoric at next week’s meeting. Recall that at its last meeting (April 21), it announced it would slow its bond purchases and anticipated the output gap would be closed in H2 22. As early as mid-March, the market was discounting the better part of 75 bp of interest rate hikes over the next two years. Since the April announcement, the market has moved broadly sideways between around 65-75 bp of tightening priced in. However, during the same time, the Canadian dollar has appreciated by almost 2% to bring the year-to-date appreciation to over 5%, the strongest of the major currencies. The Bank of Canada has expressed concern recently about the loss of competitiveness of further currency appreciation. The Canadian dollar has stalled near $0.8330 (~CAD1.20), an important chart area. It could mark the neckline of a large topping pattern that would signal a move back to parity and beyond over time.

The US dollar set a new four-year low on Tuesday, a little above CAD1.20, and jumped to CAD1.2120 yesterday. It closed above the 20-day moving average for the first time since April 20, the day before the Bank of Canada’s hawkish announcement. Follow-through buying is pressing into the CAD1.2130 area. Resistance is seen in the CAD1.2145 area, and a break of it would signal a test on the CAD1.22 area, the high from mid-May.

The Mexican peso also remains under pressure after falling by 1.3% yesterday. The dollar is trading near MXN20.20 in Europe. Nearby resistance around MXN20.22 does not look particularly strong, and the risk may extend toward the early May highs a little above MXN20.30. The legislative and local elections this weekend may keep players on edge, but so will its proxy for the region as a whole. Peru’s presidential run-off has weighed on the sol. Chile’s legislature may consider a bill that allows entire pension savings to be withdrawn, and this undermined the peso yesterday and triggered a sharp 4% sell-off in local shares. It leaves Brazil as the regional favorite. Brazil reports May services and composite PMI. Both are likely to have remained below the 50 boom/bust level. The dollar fell for the sixth consecutive session yesterday against the Brazilian real and is approaching strong support near BRL5.00.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-06-07

Update June 04 2021: SNB intervening. Sight Deposits have risen by +0.3 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

FX Daily, June 03: Don’t Believe Sino-American Thaw or Fed’s Corporate Bond Divestment is a Policy Signal

FX Daily, June 03: Don’t Believe Sino-American Thaw or Fed’s Corporate Bond Divestment is a Policy Signal

2021-06-03

Market participants appear to be biding their time ahead of tomorrow’s US jobs report as they digest recent developments. The dollar is firmer, equities are mixed, and benchmark bond yields are a little firmer. China and Hong Kong shares continue their recent underperformance, while most of the large markets in the Asia Pacific region edged higher.

FX Daily, June 01: CNY Softens after PBOC’s Move; Equities Advance on Stronger World Outlook

FX Daily, June 01: CNY Softens after PBOC’s Move; Equities Advance on Stronger World Outlook

2021-06-01

The US dollar fell against most major currencies following the PBOC’s modest move to reduce the upward pressure on the yuan. Follow-through selling was seen earlier today, and sterling reached a new three-year high. However, the dollar found a bid in the European morning, while the Scandi currencies held on to most of their earlier gains.

FX Daily, May 31: China Raises Reserve Requirement for FX, Stemming the Yuan’s Rise

FX Daily, May 31: China Raises Reserve Requirement for FX, Stemming the Yuan’s Rise

2021-05-31

US and UK markets are closed for holidays today, contributing to the rather subdued price action today. The MSCI Asia Pacific Index rallied two percent last week, the most in three months, and most markets began off the week with modest gains. Japan, Australia, and Singapore, for notable exceptions.

FX Daily, May 25: Softer Yields Weigh on the Greenback

FX Daily, May 25: Softer Yields Weigh on the Greenback

2021-05-25

The decline in US 10-year rates to two-week lows below 1.59% is helping rebuild bullish enthusiasm for stocks and weighing on the US dollar. The NASDAQ reached two-week highs yesterday, and almost all the large markets in the Asia Pacific region rose, though India struggled.

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

2021-05-12

The markets remain on edge. Asia Pacific and US equities have yet to find stable footing, and inflation fears are elevated. The foreign exchange market has turned quiet as the dollar consolidates its recent losses.

FX Daily, May 11: Stocks Slide but Little Demand for Safe Havens

FX Daily, May 11: Stocks Slide but Little Demand for Safe Havens

2021-05-11

The sell-off in US shares yesterday has triggered sharp global losses today, and there is no flight into fixed income as benchmark yields are higher across the board. Nor is the dollar serving as much as a safe haven. It is mostly softer against the major currencies.

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

2021-01-19

Overview: The animal spirits are on the march today. Equities are mostly higher, peripheral European bonds are firm, and the dollar is mostly softer. After posting the first back-to-back decline this year, the MSCI Asia Pacific Index bounced back today, led by a 2.7% gain in Hong Kong (20-month high) and a 2.6% rise in South Korea’s Kospi.

Tags: #USD,$CNY,Brazil,Chile. Taxes,China,Currency Movement,EUR/CHF,Featured,G7,India,jobs,Mexico,newsletter,Russia,USD/CHF