Swiss Franc The Euro has risen by 0.13% to 1.0965 EUR/CHF and USD/CHF, June 02(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The US dollar is enjoying broad, even if not large, gains today following yesterday’s recovery from three-year lows against sterling and four-year lows against the Canadian dollar. The greenback is firmer against all the major currencies. The Australian and New Zealand dollars the weakest, even though Australia reported stronger than expected Q1 GDP and its stock market was among the strongest in the region with a 1% gain. Emerging market currencies are also weaker. Turkey’s president, who has dismissed four central bank officials in the past two months, renewed his call for rate

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, autos, Currency Movement, EUR/CHF, Eurozone Producer Price Index, Featured, Federal Reserve, newsletter, U.K., USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.13% to 1.0965 |

EUR/CHF and USD/CHF, June 02(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

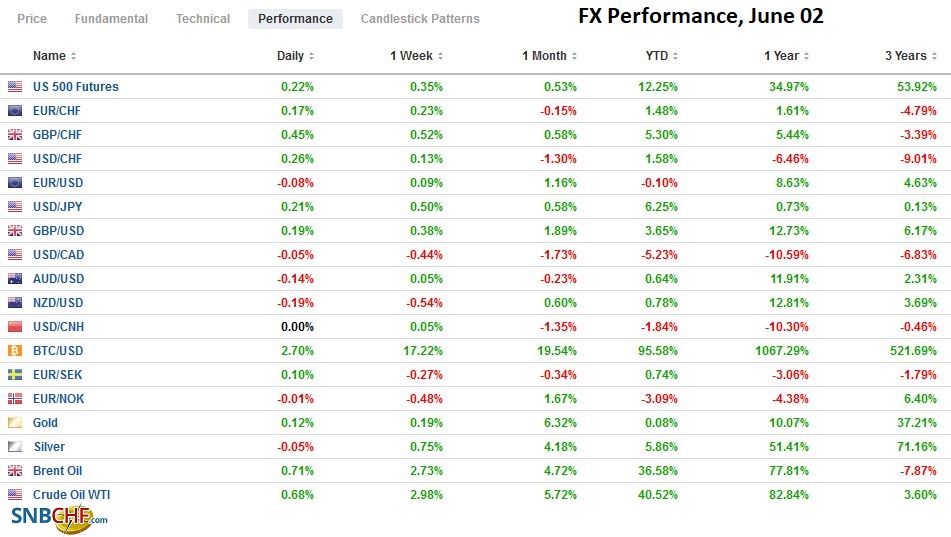

FX RatesOverview: The US dollar is enjoying broad, even if not large, gains today following yesterday’s recovery from three-year lows against sterling and four-year lows against the Canadian dollar. The greenback is firmer against all the major currencies. The Australian and New Zealand dollars the weakest, even though Australia reported stronger than expected Q1 GDP and its stock market was among the strongest in the region with a 1% gain. Emerging market currencies are also weaker. Turkey’s president, who has dismissed four central bank officials in the past two months, renewed his call for rate cuts and spurring a slide in the lira to new record lows. The Israeli shekel is also heavy ahead of the deadline for the opposition to propose a new coalition. The JP Morgan Emerging Markets Currency Index is lower for the second consecutive session. It has not suffered back-to-back losses since May 11-12. Asia Pacific equities were mixed, with China, Hong Kong, and India heavy. Philippine shares rallied more than 3% as social restrictions eased and foreign investment returned. Europe’s Dow Jones Stoxx 600 is firm but consolidating new yesterday’s record high. US futures are little changed. The US 10-year yield is little changed after pulling back from near 1.64% yesterday. It is holding above 1.60% but had closed below it in three of last week’s five sessions. European yields are a touch firmer today. Gold is struggling to maintain the foothold above $1900, and oil prices are firm, with July WTI solidifying its hold on the $68-handle. China’s ability to stem the rise of industrial commodities is being tested. Iron ore gained for the fourth consecutive session, and steel rebar has risen in three of the past four sessions. Copper is off for the second session, and lumber prices fell in the US yesterday for the sixth consecutive session. The CRB Index is at its best level since 2015. |

FX Performance, June 02 - Click to enlarge |

Asia Pacific

Australia’s economy expanded by 1.8% quarter-over-quarter in Q1 21, which was a little faster than expected, and Q4 20 GDP was revised to 3.2% from 3.1%. Consumption and residential investment accounted for almost two-thirds of the growth. The relaxation of social restrictions spurred demand for services while the purchases of goods slipped. Savings were tapped. However, the second-most populous state (Victoria) has re-imposed and extended a lockdown that warns of slower growth in the current quarter. In addition to household consumption, inventories were rebuilt (0.7 percentage-point contribution to GDP). With inventory-sales ratios returning to pre-crisis levels, it is unlikely to be repeated.

The vaccination efforts in Japan are accelerating. The seven-day average of vaccines has quadrupled over the past couple of weeks. Reports suggest that Japan is now vaccinating around half a million people a day, and now more than 10% of the population has at least one jab. Some work suggests that after a country surpasses the 10% mark that the stock market rallies. Japanese officials seek to double the inoculation rate to one million a day by the middle of the month.

A small base for the dollar has been formed around JPY109.30-JPY109.40 in recent days. Although it briefly traded above JPY110 at the end of last week, it has not mustered the strength so far this week. There is a $1.23 bln option struck that expires tomorrow.

The Australian dollar rose to a five-day high just shy of $.07775 and was greeted with strong selling pressure that knocked it through yesterday’s low near $0.7730. A close below there would constitute a bearish outside day. Initial support is seen around $.7700. Last week’s low was set near $0.7675.

The Chinese yuan fell for the third consecutive session, though the losses are minor. The onshore yuan eased by about 0.05% today to bring the three-day decline to about 0.25%. The reference rate was set at CNY6.3773, back to the more normal deviation from the bank model’s survey by Bloomberg of CNY6.3777.

Europe

The UK has been given the approval to begin the ascension process to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). Japan’s foreign minister Nishimura confirmed the decision. If the UK were to join, the CPTPP would equal the EU in terms of the GDP covered. The UK enjoyed a trade surplus with the CPTPP members in Q1. China has made some preliminary overtures toward wanting to join as well. When then-President Trump withdrew from negotiations, he noted that both Democrat candidates (Clinton and Sanders) had opposed the TPP during the 2016 campaign. The Biden administration shows little interest in re-joining. Instead, it appears it is seeking to strengthen bilateral ties. The first two foreign leaders to be hosted by the White House are from the region (Japan and South Korea).

As we noted yesterday, the Nationwide Building Society index showed house prices were rising at their fastest pace since 2014. Deputy Governors of the Bank of England, Cunliffe and Ramsden, expressed concern. It clearly is on their radar screen for considering to pullback stimulus. Last month the BOE announced it was slowing its bond purchases. The 10.9% year-over-year gain in May was double the rise anticipated by economists. Other countries, including Canada, Australia, and New Zealand, are also wrestling with surging house prices. House prices are rising rapidly in the US as well, but the Federal Reserve appears to be in no hurry to reduce the mortgage-backed securities it is buying every month ($40 bln).

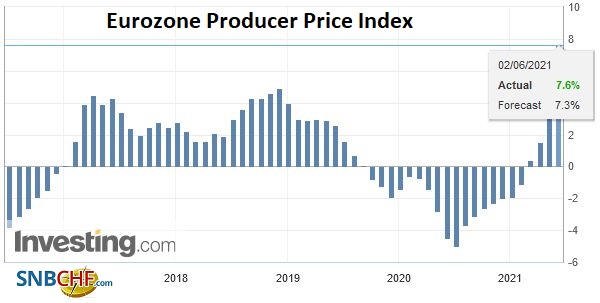

EurozoneEurozone producer prices rose 1% in April to bring the year-over-year rate to 7.6% from 4.3% in March. Yesterday’s preliminary May CPI reading of 2% was a touch higher than expected. The ECB meets next week, and there is much teeth-gnashing whether it will slow its bond purchases from the accelerated pace over the past three months. We caution against exaggerating the significance of the decision. The PEPP program runs through the end of next March, and most importantly, over the past three months, the euro, yields, and premia over Germany have widened. The euro reversed lower yesterday after briefly trading above $1.2250. It left a bearish shooting star candlestick in its wake, and follow-through selling today has taken the single currency to $1.2170 to test the 20-day moving average. It has not closed below this moving average in nearly a month. The month-end induced low from last week was slightly below $1.2135. The $1.2125 area represents the midpoint of last month’s rally. Sterling recorded a bearish outside down day yesterday, trading on both sides of Monday’s range and settling below Monday’s low. Selling today has extended the losses to $1.4125, near its 20-day moving average. Sterling has not closed below the 20-day average since April 30. A convincing break of the $1.4090 area signals a test on $1.40. |

Eurozone Producer Price Index (PPI) YoY, April 2021(see more posts on Eurozone Producer Price Index, ) Source: Investing.com - Click to enlarge |

America

Pressure on the very short-end of the US curve has been evident for some time, but now a key threshold has been violated, which in turn can see a policy response. The effective Fed funds rate (weighted average) slipped to five basis points at the end of last week. When the Fed funds are within five basis points of its lower bound, the Fed has moved to secure the floor by raising the rate it pays on reserves (all reserves, not just on the excess reserves) and/or tweak the rate on the reverse repo operations. The uncertainty about the Fed’s response seemed to have impacted the T-bill sales where the three-month bill was sold for two basis points while the six-month bill went for 3.5 bp.

The US and Mexico report May auto sales today. US auto sales are expected to slow from the heady 18.51 mln unit pace in April to 17.40 mln last month. In the first four months of 2021, US sales have averaged 17.14 mln (seasonally adjusted annual pace). This compares with 13.4 mln last year and 16.76 mln in 2019. Mexico’s domestic vehicle sales averaged 85.7k a month through April. In the same period last year, sales averaged almost 83k, while in the January-April period in 2019, sales were averaged 107.9k.

The US Beige Book, prepared for the June 15-16 FOMC meeting, will be released. It is expected to provide anecdotal evidence that despite April’s disappointing employment data and some weakness in data surprise models, the US growth is accelerating with labor shortages and supply chain disruptions evident. Fed officials are saying that talks about tapering can begin in the coming months. Most market observers, according to surveys, see this starting in earnest either in late August or the September 21-22 FOMC meeting.

The US dollar slipped to new four-year lows against the Canadian dollar. Still, key support at CAD1.20 held, and the greenback staged an impressive bounce, leaving behind a bullish hammer candlestick. Buying today has been limited. The 20-day moving average (~CAD1.2095) remains intact. The US dollar was testing it last week but has not closed above it since April 20, the day before the Bank of Canada delivered a hawkish surprise to the market. Above the CAD1.2100 area, the upper end of the recent range is seen closer to CAD1.2145.

The US dollar also recorded an outside up day against the Mexican peso yesterday, and follow-through buying today lifted it above MXN20.00 for the first time this week. The pre-weekend high was near MXN20.0770. The latest polls for this weekend’s election shows the AMLO’s Morena party, which has 48% of the seats (239) in the lower chamber, is likely to be close to a supermajority (334 seats) when combined with the coalition partners (Green Party and Worker’s Party).

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-06-07

Update June 04 2021: SNB intervening. Sight Deposits have risen by +0.3 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

FX Daily, June 04: US and Canada Report on Jobs as G7 Fin Mins Talk Taxes

FX Daily, June 04: US and Canada Report on Jobs as G7 Fin Mins Talk Taxes

2021-06-04

Stronger than expected US employment data, ahead of today’s monthly report and compromise proposal on corporate tax by the White House to help secure a deal on infrastructure sent US bond yields and the dollar high. Late dollar shorts were forced to cover.

FX Daily, June 03: Don’t Believe Sino-American Thaw or Fed’s Corporate Bond Divestment is a Policy Signal

FX Daily, June 03: Don’t Believe Sino-American Thaw or Fed’s Corporate Bond Divestment is a Policy Signal

2021-06-03

Market participants appear to be biding their time ahead of tomorrow’s US jobs report as they digest recent developments. The dollar is firmer, equities are mixed, and benchmark bond yields are a little firmer. China and Hong Kong shares continue their recent underperformance, while most of the large markets in the Asia Pacific region edged higher.

FX Daily, June 01: CNY Softens after PBOC’s Move; Equities Advance on Stronger World Outlook

FX Daily, June 01: CNY Softens after PBOC’s Move; Equities Advance on Stronger World Outlook

2021-06-01

The US dollar fell against most major currencies following the PBOC’s modest move to reduce the upward pressure on the yuan. Follow-through selling was seen earlier today, and sterling reached a new three-year high. However, the dollar found a bid in the European morning, while the Scandi currencies held on to most of their earlier gains.

FX Daily, May 31: China Raises Reserve Requirement for FX, Stemming the Yuan’s Rise

FX Daily, May 31: China Raises Reserve Requirement for FX, Stemming the Yuan’s Rise

2021-05-31

US and UK markets are closed for holidays today, contributing to the rather subdued price action today. The MSCI Asia Pacific Index rallied two percent last week, the most in three months, and most markets began off the week with modest gains. Japan, Australia, and Singapore, for notable exceptions.

FX Daily, May 26: RBNZ Joins the Queue, while Yuan’s Advance Continues

FX Daily, May 26: RBNZ Joins the Queue, while Yuan’s Advance Continues

2021-05-26

The decline in US rates and the doves at the ECB pushing back against the need to reduce bond purchases next month have seen European bond yields unwind most of this month’s gain. The inability of US shares to hold on to early gains yesterday did not deter the Asia Pacific and European equities from trading higher.

FX Daily, May 20: Market Stabilize after Yesterday’s Tumultuous Session

FX Daily, May 20: Market Stabilize after Yesterday’s Tumultuous Session

2021-05-20

US equity indices finished lower, but the real story was their recovery. Asia Pacific equities were mixed, with Australia’s 1.5% rally leading the recovery in some markets, including Tokyo and Singapore. Europe’s Dow Jones Stoxx 600 is up a little more than 0.5% near mid-session, led by information technology and industrials, while energy and financials lagged with small gains.

FX Daily, May 18: Risk Appetites Return Bigly

FX Daily, May 18: Risk Appetites Return Bigly

2021-05-18

In Asia, equities markets rallied strongly, led by the more than 5% gain in Taiwan, the most in over a year as Monday’s 3% drop was more than overcome. The Nikkei gained more than 2% despite the deeper than expected contraction in Q1 GDP. Hong Kong, South Korea, and India also rose more than a 1% gain as tech came roaring back.

Tags: #USD,$CNY,autos,Currency Movement,EUR/CHF,Eurozone Producer Price Index,Featured,federal-reserve,newsletter,U.K.,USD/CHF