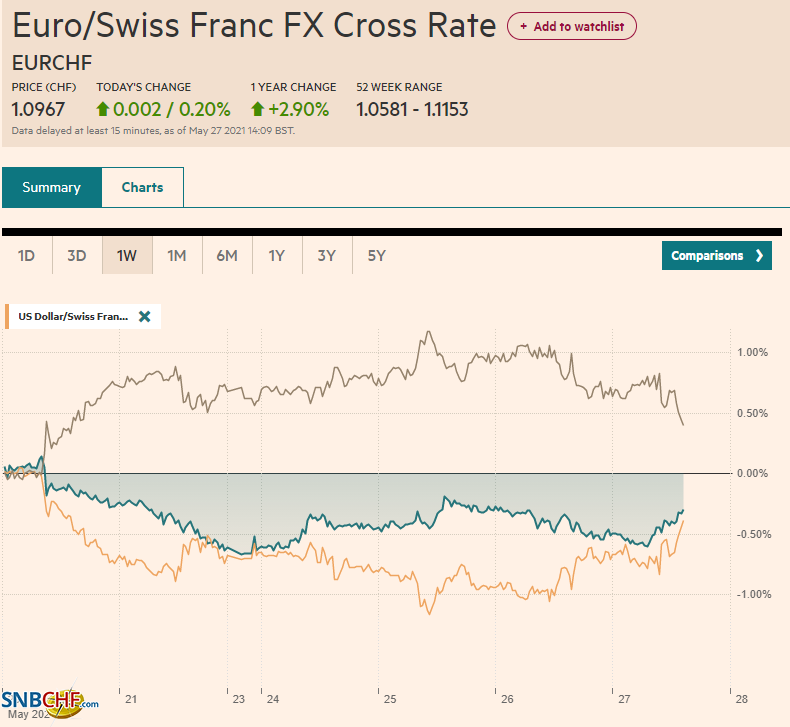

Swiss Franc The Euro has risen by 0.20% to 1.0967 EUR/CHF and USD/CHF, May 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Dollar demand linked to the month-end gave the greenback a bit of a reprieve, helped by firmer bond yields. Some momentum players may have been forced out of the euro and yen when the .22 and JPY109 levels yielded. However, follow-through dollar buying has been limited, and it has come back a little softer but broadly so. The US 10-year yield has steadied after the 1.55% level held for the second session, though the upside has been limited to a few basis points. European benchmark yields are narrowly mixed after the recent declines, encouraged ostensibly by the doves pushing back

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, China, Currency Movement, ECB, EUR/CHF, Featured, newsletter, Poland, South Korea, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.20% to 1.0967 |

EUR/CHF and USD/CHF, May 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Dollar demand linked to the month-end gave the greenback a bit of a reprieve, helped by firmer bond yields. Some momentum players may have been forced out of the euro and yen when the $1.22 and JPY109 levels yielded. However, follow-through dollar buying has been limited, and it has come back a little softer but broadly so. The US 10-year yield has steadied after the 1.55% level held for the second session, though the upside has been limited to a few basis points. European benchmark yields are narrowly mixed after the recent declines, encouraged ostensibly by the doves pushing back against a slowing of ECB bond purchases next month. Asia Pacific equities were mixed. Japan, South Korea, Hong Kong, and Taiwan markets eased, while China, Australia, and India rose. The Nikkei fell for the first time in six sessions, led by chemical companies and banks, amid concern that the formal emergency will be extended for a few more weeks in at least Tokyo and Osaka. Of note, the easing of social restrictions sent the Philippines stock market up 5.1% to bring the three-day advance to 8%., and lifting the peso the most among emerging market currencies today. European shares are edging higher, and the Dow Jones Stoxx 600 is trying to extend its advance for a sixth session, but this week’s gains have been minor, less than 0.3%. US futures are a little heavier. Industrial commodities, including iron ore and steel rebar, continued their downside correction, while lumber prices fell for the third session in the US yesterday. Oil is consolidating in narrow ranges, with the July WTI in about a 30-cent range on either side of $65.80. Gold stalled yesterday after reaching almost $1914, the highest level since mid-January. It is holding above $1890, but the upside momentum has not been rekindled. |

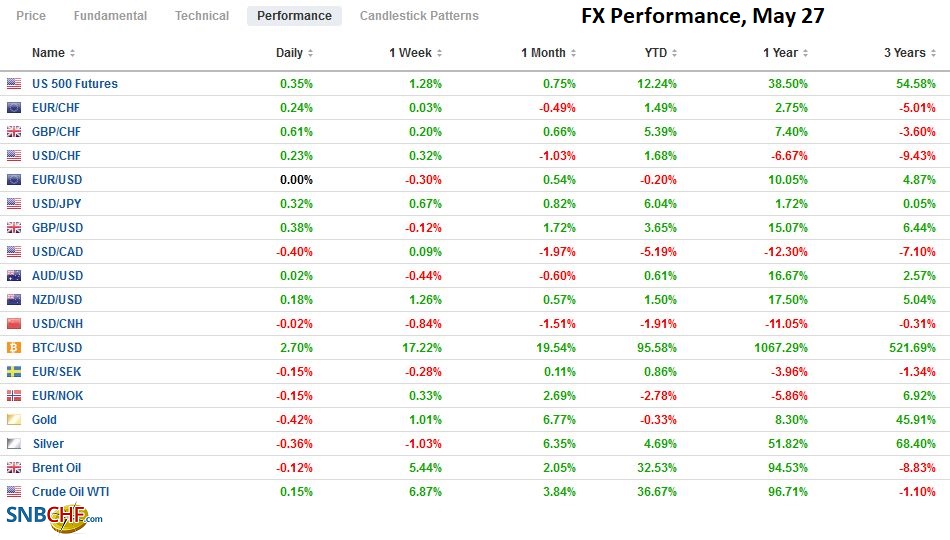

FX Performance, May 27 - Click to enlarge |

Asia Pacific

The media seemed to emphasize that the US Trade Representative Tai had a phone call with China’s Vice Premier Liu He yesterday. No meaningful details were reported, the information content nil. However, the real signal came from the administration’s head of the “Indo-Pacific” region, Campbell, who announced that the era of “engagement” was over and a new set of strategic priorities was emerging. The dominant paradigm, he declared, was one of competition. Meanwhile, the bill being debated in the US Senate that seeks to bolster and modernize US industry, wrapped in cold-war-like language that it is needed to answer China’s competitive threat, is running into Republican opposition. Several GOP Senators want to make amendments to the bill, which Majority Leader Schumer wants to complete before the weekend.

South Korea’s central bank left policy on hold but appears to have begun laying the groundwork for an adjustment of policy. It revised this year’s GDP to 4% from 3% and sees CPI at 1.8%. The market appears to be discounting a rate hike either late this year or early next year and nearly two hikes by mid-2022.

The dollar’s range against the yen this month has been among the smallest in years (~JPY108.35-JPY109.80). Today’s range is not even 20-pips. It has held above JPY109, and if sustained today, it would be the first session since May 17 it has not traded below. Of note, foreign purchases of Japanese bonds jumped to nearly JPY1.2 trillion last week, the second-highest week amount this year.

The Australian dollar failed to sustain the move to $0.7800 seen yesterday after the RBNZ’s hawkish message. It found support ahead of $0.7720 and is hovering around little changed levels in the European morning.

The firmer US dollar in North America yesterday failed to help steady the yuan. The greenback recorded near three-year lows near CNY6.3740. It is the sixth session, the dollar has been unable to sustain upticks. It is not just against the dollar the yuan is strengthening. Against the CFETS basket of 24 countries, it has risen for a fifth session and is at its highest level in five years. In the setting of the reference rate, there was little sign of protest from Chinese officials. The dollar’s fixing was at CNY6.4030, while the Bloomberg survey median projection was CNY6.4028.

Europe

The doves at the ECB have taken to the media to press against reducing the PEPP bond-buying next month. Previously, the hawks had suggested that rising inflation and an improving economic outlook could allow it to slow the purchases that had been increased since mid-March. Some tried to frame a narrative around it and contrasted it with the vague talk from several Fed officials that a discussion about tapering could be appropriate in the coming months. It was cited as the explanation for the euro’s decline yesterday of less than three-quarters of a cent. It seems a stretch and ignores that the increased bond-buying since mid-March has coincided with a stronger, not a weaker, euro. The euro held the week’s low near $1.2170 and last week’s low closer to $1.2125. Does there have to be a big fundamental story to account for the consolidation ahead of month-end and after a seven-day advance in the past ten days?

On Tuesday, Hungary’s central bank hinted it could adjust monetary policy as early as next month. Yesterday, Poland’s central bank bought less than half of the debt that the market anticipated it would. This spurred speculation that it was tapering, as Governor Glapinski suggested would be necessary before a rate hike in early 2022. The 10-year bond yield jumped six basis points yesterday and has pulled back a little today. The market appears to have a hike priced in before the end of the year. There are two hikes priced into Hungary and one for the Czech Republic.

The euro is straddling the $1.22-level and is in a 40-pip range so far today. An option for 550 mln euros at $1.22 expires today, and another one for almost 1.1 bln euros expires there tomorrow. In the last two sessions, the euro has been capped around $1.2260. Support is about a cent lower. The intraday momentum indicators favor the upside in the early going in the North American session. Initial resistance is seen in the $1.2220 area.

Sterling has stalled around $1.4200 last week and this week. It briefly slipped below $1.4100 in Asia for the first time since May 17 but recovered quickly. Resistance now is seen in the $1.4140-$1.4160 band.

America

The US reports April durable goods orders. Several important high-frequency economic data points have underwhelmed the market, and many models have reduced their earlier estimates for growth here in Q2. Nevertheless, a solid, even if not a spectacular, quarter is still expected. In April, we already know that Boeing had 25 new orders, but pared by the cancelation of 17 orders (all 737 Max). Still, it was the third month of net new orders. Excluding defense and aircraft, the median forecast in Bloomberg’s survey is for a solid 1.0% rise. To put that in perspective, consider that the 24-month average was steady at 0.1% in the last four months of 2019. The shipment of those goods used in models to estimate GDP is expected to have matched the Q1 average of 0.8%. The average was 1.9% in Q3 and 1.3% in Q4. The US reports a revised estimate for Q1 GDP, and it could be tweaked a little higher on the back of stronger consumption data. Yet both reports may be overshadowed by the weekly initial jobless claims, which have fallen for three consecutive weeks for the first time since last Oct-Nov. Next Friday, the May jobs report is released, and the early estimates are hovering a little above 600k.

This week’s two and five-year notes have generated higher bid cover ratios and produced lower yields than the last auctions. Today, Treasury is selling $62 bln seven-year notes. The yield is around seven basis points lower than last month’s auction. Meanwhile, the banks plopped down $450 bln in the Fed’s overnight reverse repo. It could surge into the month-end.

Mexico reports its April unemployment figures today. A small increase is expected from March’s 3.89% rate. Mexico’s unemployment averaged 3.49% in 2019 and 4.4% in 2020. The minutes from the recent central bank meeting are also released. The market anticipates a somewhat more hawkish stance and appears to be pricing in a rate hike by year-end. Mexico holds legislative and local elections on June 6. It has already been marred by the most violence in several years. The peso has appreciated by about 2.8% since the end of March. It is virtually flat on the year (~+0.2%).

The US dollar closed firmly against the Canadian dollar yesterday, and follow-through buying lifted it to almost last week’s high, around CAD1.2145. However, it has been coming off since early in the Asian sessions and reached almost CAD1.2100 in the European morning. There is an option for nearly $790 mln at CAD1.2100 that expires today and another for $1.2 bln there that expires tomorrow. Note that the US dollar has fallen against the Canadian dollar for the past seven weeks. That streak is at risk now. It finished last week near CAD1.2065.

The Mexican peso is moving sideways for the third session. The greenback is in a roughly MXN19.81-MXN19.93 trading range. The dollar has not traded above MXN20.00 this week, which, if sustained, would be the first week in five and only the second this year.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, May 25: Softer Yields Weigh on the Greenback

FX Daily, May 25: Softer Yields Weigh on the Greenback

2021-05-25

The decline in US 10-year rates to two-week lows below 1.59% is helping rebuild bullish enthusiasm for stocks and weighing on the US dollar. The NASDAQ reached two-week highs yesterday, and almost all the large markets in the Asia Pacific region rose, though India struggled.

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-05-25

Update May 24 2021: SNB intervening. Sight Deposits have risen by +1.9 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

FX Daily, May 24: China Action on Commodities and Crypto Featured

FX Daily, May 24: China Action on Commodities and Crypto Featured

2021-05-24

The US dollar is firmer in the European morning after starting out with a softer bias in Asia Pacific turnover. The dollar-bloc currencies, sterling, and the Swiss franc are heavy, but ranges are narrow, and consolidation seems to be the flavor of the day.

FX Daily, May 19: Now What Does Bitcoin say About the Dollar and the US?

FX Daily, May 19: Now What Does Bitcoin say About the Dollar and the US?

2021-05-19

A setback in commodities and technology are roiling equity markets today. The inability of US equities to sustain yesterday’s rally provided an initial headwind to trading in the Asia Pacific region today. Hong Kong and South Korea markets were closed for holidays, but most of the bourses fell, led by Australia, where the market tumbled nearly 2%, the most in almost three months as the drop in mining and energy took a toll.

FX Daily, May 10: The Dollar Remains on the Defensive

FX Daily, May 10: The Dollar Remains on the Defensive

2021-05-10

Last week’s cyberattack on the largest US gasoline pipeline continues to lift oil and gasoline prices. The June gasoline futures gapped higher to extend last week’s 2.4% gain but has subsequently moved lower to enter the gap.

FX Daily, January 20: The Dollar Slips to New Lows against Sterling and the Mexican Peso

FX Daily, January 20: The Dollar Slips to New Lows against Sterling and the Mexican Peso

2021-01-20

Global equities are moving higher today. Led by continued strong buying of Hong Kong shares, the MSCI Asia Pacific Index rose to new highs. The Hang Seng is up 6% this year and is approaching the 2019 record high. Australia’s shares set a new record today. Japan and Taiwan bucked the trend.

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

2021-01-19

Overview: The animal spirits are on the march today. Equities are mostly higher, peripheral European bonds are firm, and the dollar is mostly softer. After posting the first back-to-back decline this year, the MSCI Asia Pacific Index bounced back today, led by a 2.7% gain in Hong Kong (20-month high) and a 2.6% rise in South Korea’s Kospi.

FX Daily, January 11: Greenback Extends Recovery

FX Daily, January 11: Greenback Extends Recovery

2021-01-11

Julius Ceasar is said to have "crossed the Rubicon" on January 10, 49 BCE, taking the 13th Legion into Rome, defying orders from the Senate, and precipitating the Roman Civil Wat that marked the end of the republic and the birth of the empire.

Tags: #USD,China,Currency Movement,ECB,EUR/CHF,Featured,newsletter,Poland,South Korea,USD/CHF