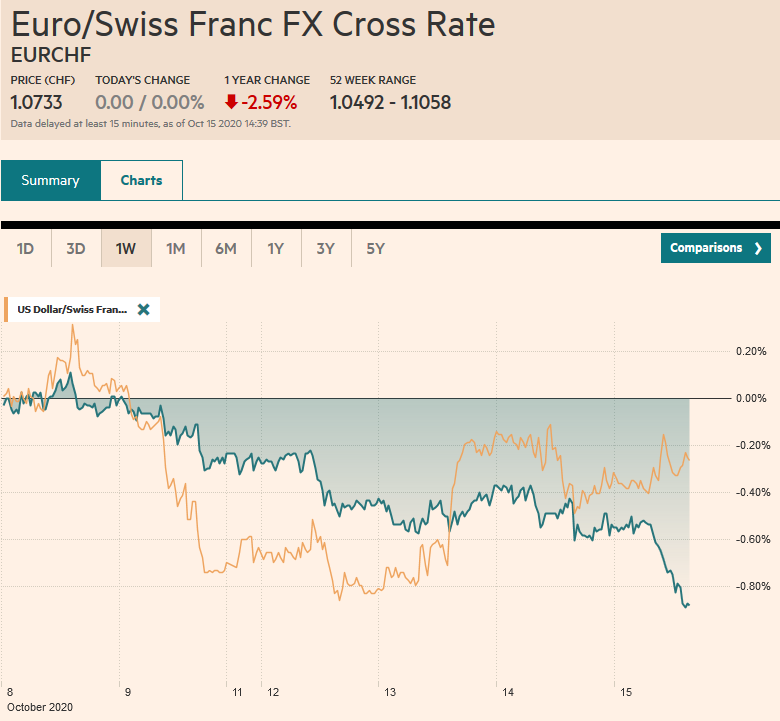

Swiss Franc The Euro has stable by 0.00% to 1.0733 EUR/CHF and USD/CHF, October 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: A combination of the surging virus, threatening the slow recovery that was already losing momentum, the lack of new stimulus in the US, and market positioning is seeing risk unwind in a big way today. Equities are selling off. Led by a 2% drop in Hong Kong, Asia Pacific equities tumbled, with the exception of Australia, where signals from the central bank suggested more easing may be around the corner. The Dow Jones Stoxx 600 is off for a third day, but the nearly 2.2% decline is the largest drop since September 21. US shares are also lower. The S&P 500 closed the gap from

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, Australia, Brexit, China, Currency Movement, Featured, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has stable by 0.00% to 1.0733 |

EUR/CHF and USD/CHF, October 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A combination of the surging virus, threatening the slow recovery that was already losing momentum, the lack of new stimulus in the US, and market positioning is seeing risk unwind in a big way today. Equities are selling off. Led by a 2% drop in Hong Kong, Asia Pacific equities tumbled, with the exception of Australia, where signals from the central bank suggested more easing may be around the corner. The Dow Jones Stoxx 600 is off for a third day, but the nearly 2.2% decline is the largest drop since September 21. US shares are also lower. The S&P 500 closed the gap from Monday’s higher open yesterday, and next is the gap from last Friday (~3447.3-3458.0). Benchmark 10-year yields are lower, led by Australia’s seven basis point decline. Core bonds in Europe are outperforming the periphery with a 3-4 bp decline yields. The US 10-year Treasury yield is slipping below 0.70% to reach its lowest level since October 2. The dollar is gaining across the board. The Antipodeans and Scandis are the weakest (off ~0.4-1.2%). Even the yen is softer. The liquid accessible emerging market currencies lead the retreat, and the JP Morgan Emerging Market Currency Index is off (~0.3%) for a fourth consecutive session. Gold is heavy and unable to sustain gains above $1900, and November crude oil is pulling back from its push above $41. |

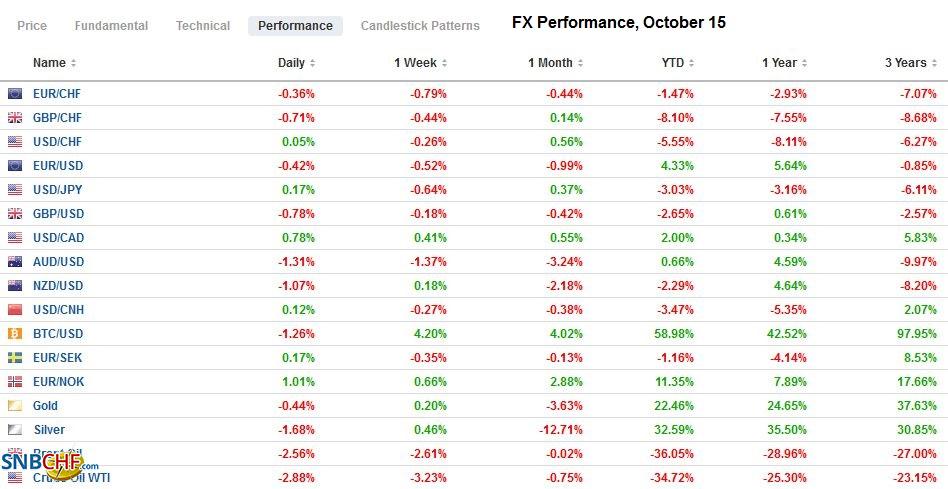

FX Performance, October 15 - Click to enlarge |

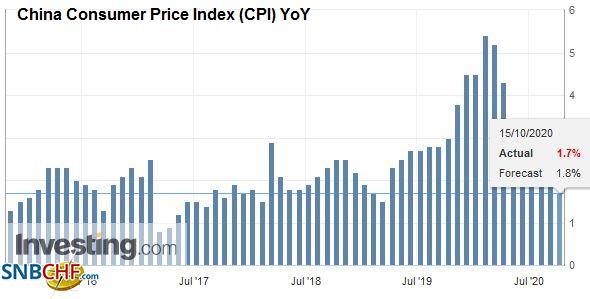

Asia PacificChina’s price pressures are more subdued than economists expected. September CPI slowed to 1.7% from 2.4% in August. It is the lowest since February 2019 and was helped by a further relaxation of food prices. The upward pressure on pork prices subsided to 25.5% from 52.6%. Core prices were unchanged at 0.5%. |

China Consumer Price Index (CPI) YoY, September 2020(see more posts on China Consumer Price Index, ) Source: investing.com - Click to enlarge |

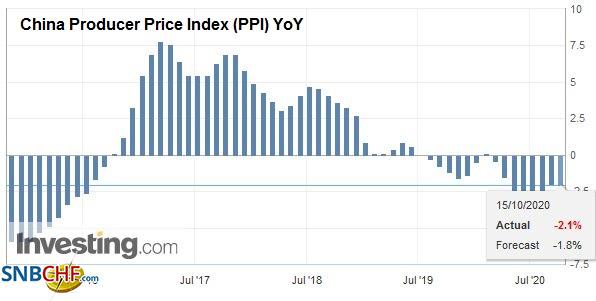

| Producer prices were also weaker than expected. The 2.1% decline from a year ago was even more than in August (-2.0%) and snaps a three-month increasing trend. The base effect contributes to the lower inflation as the year-ago swine flu impact is dropping from the year-over-year comparisons. Officials continue to emphasize supply-side efforts, but the disinflation risks are rising. |

China Producer Price Index (PPI) YoY, September 2020(see more posts on China Producer Price Index, ) Source: investing.com - Click to enlarge |

There were two developments in Australia to note. First, the employment data was soft. Jobs were lost for the first time in three months, even though the loss of jobs (29.5k) was less than economists projected. Two-thirds of the job loss were full-time positions. The unemployment rate ticked up to 6.9% from 6.8%, and the participation rate slipped as the impact of the Victoria shutdown was evident. Second, the RBA Governor Lowe suggested that the central bank is considering lower rates and buying longer-term bonds, which, even with today’s decline, are the highest among the high-income countries.

The dollar held JPY105 yesterday, and there is a $1.1 bln option expiring there today. It has recovered to JPY105.35. The week’s high is near JPY105.85. Initial resistance is seen in the JPY105.45-JPY105.60 band. The Australian dollar is off about 1.25% (~$0.7070), its biggest loss in three weeks. The loss of $0.7100 undermines the outlook, and a break of $0.7060 sets the stage for a test on more significant support near $0.7000. The PBOC set the dollar’s reference rate at CNY6.7374, which in line with bank projections. The broader dollar gains help the PBOC if it wanted to slow the yuan’s ascent. The PBOC injected liquidity into the banking system, more than is rolling off tomorrow. The 10-year bond yield edged to a new high of 3.22%.

Europe

The UK’s chief negotiator will inform Prime Minister Johnson that a trade deal with the EU is still possible. This will allow Johnson to step away from the ultimatum. It now looks as if negotiations will continue for the next couple of weeks and possibly into early November. The November EU summit was to discuss relations with China, against whom the EU has levied punitive tariffs in recent weeks on some steel and aluminum products and is squeezing Huawei. The IMF revised down its forecast for next year’s growth to 5.9% from 6.3% in June. This is the highest in the G7 and incidentally is in line with the median forecast in the Bloomberg survey (6.0%). However, a hard exit, which means a reversion to the WTO standards, could shave growth by 1.0%-1.5%.

The euro was pushing above $1.18 at the start of the week and now is threatening to fall below $1.17 for the first time since October 2. There is an option for nearly 650 mln euros at $1.1695 that expires today, which is also the (61.8%) retracement of the bounce since the September 25 low near $1.1610. While the intraday technical readings are stretched, the euro needs to reclaim $1.1720 to steady the tone, and ideally, $1.1740. It has not been below $1.16 since late July. The surging virus, new restrictions are weighing on sentiment. Sterling is trading within yesterday’s wide range and is almost a cent range today (~$1.2935-$1.3030). It too looks to have found a bid in early European turnover, and the option for roughly GBP615 mln at $1.2980 that expires today may still be in play. The euro had approached GBP0.9300 in mid-September approached GBP0.9000 yesterday, the low since, and is consolidating today.

America

It seems that the market has reacted several times to fading hopes of a stimulus effort ahead of the election. Yet more stimulus after the election still appears to be a safe bet. The election, as we have been saying, will likely determine the size and scope of the effort. The US is likely to have the largest deficit among the high-income countries next year as it did this year.

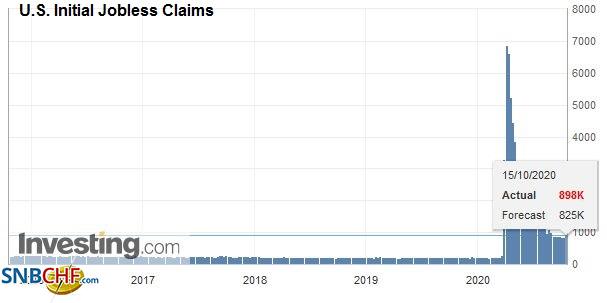

| On tap today are the weekly jobless claims. A decline to 825k (from 840k) is expected. Still, the data remains marred by California’s continued problems, where its numbers will remain frozen at mid-September levels for possibly a couple of more weeks as it works through backlog and identity verification issues. Estimates suggest that there are as many as 600k backlog initial claims and a million continuing claims. The point is that the labor market remains stressed, and improvement is slow. The NY and Philadelphia Fed manufacturing surveys for October will be reported, and both are expected to have softened slightly. It would be the fourth consecutive month that the Philly Fed’s survey has softened. The Fed’s speaking calendar remains busy with six officials speaking today, including Barkin at the Economic Club of New York. |

U.S. Initial Jobless Claims, October 15, 2020(see more posts on U.S. Initial Jobless Claims, ) Source: investing.com - Click to enlarge |

ADP reports Canada’s payroll data, and the government reports September’s existing-home sales. However, the driving force of the Canadian dollar today is the broader risk appetites, and the lack thereof is helped the US dollar recover to CAD1.32 in the European morning after testing CAD1.31 earlier this week. The near-term potential extends into the CAD1.3220-CAD1.3260 area. The greenback is also recovering against the Mexican peso. The move above MXN21.45 warns of the risk toward MXN21.65 and possibly the MXN21.80 area.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

The capital markets are relatively quiet so far today as the FOMC meeting gets underway. Equity markets in the Asia Pacific region, but Japan and Australia advanced, and the regional benchmark rose for the fourth consecutive session. European stocks are a little firmer.

FX Daily, September 16: Dollar Eases Ahead of the FOMC

FX Daily, September 16: Dollar Eases Ahead of the FOMC

Overview: The dollar has been sold against nearly all the world’s currencies ahead of what is expected to be a dovish Federal Reserve, even if no fresh action is taken. The Scandis and Antipodean currencies are leading the majors.

FX Daily, October 14: UK Blinks on Threat to Walk Away on Eve of EU Summit

FX Daily, October 14: UK Blinks on Threat to Walk Away on Eve of EU Summit

Overview: Turn around Tuesday saw the dollar bounce, particularly against the Australian dollar and European currencies, among the majors. Sterling pared earlier losses on reports that the UK would not walk away from the talks just yet, while the euro remains on its back foot.

FX Daily, July 10: Surge in Coronavirus Spooks Investors as China Takes Profits

FX Daily, July 10: Surge in Coronavirus Spooks Investors as China Takes Profits

Record fatalities in a few US states, coupled with new travel restrictions in Italy and Australia, have given markets a pause ahead of the weekend. News that two state-backed funds in China took profits snapped the eight-day advance in Shanghai at the same time as there is an attempt to rein in the use of margin.

FX Daily, July 13: Risk Appetites Firm, but the Greenback is Mixed

FX Daily, July 13: Risk Appetites Firm, but the Greenback is Mixed

Equities began the week on a firm note in the Asia Pacific region. The Nikkei gained more than 2%, and the profit-taking seen in China ahead of the weekend was a one-day phenomenon. The Shanghai Composite rose 1.8%, and the Shenzhen Composite surged 3.5%. Taiwan and South Korea markets also rallied more than 1%.

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

The optimism among investors appears to have evaporated in the face of new US-Chinese tensions, possible delays in the next US fiscal stimulus, and new record virus infections in Australia and Hong Kong. US stocks had pared early gains yesterday, and the high-flying NASDAQ finished lower after setting new record highs.

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

The NASDAQ rallied 1% yesterday to record highs as the Dow Industrials struggled, and the S&P 500 was able to eke out a small gain. The coattails were short, and the strength of the yen may have contributed to a 0.2% loss of the Nikkei. Still, its 6.2% advance this month is the best among the G10.

FX Daily, August 24: Markets Prove Resilient to Start New Week

FX Daily, August 24: Markets Prove Resilient to Start New Week

New virus outbreaks in Europe and Asia are not adversely impacting the capital markets today. Global equities are firmer. Some reports suggesting the US ban on WeChat may not be as broad as initially signaled helped lift Hong Kong shares, but nearly all the markets in the region traded higher.

Tags: #USD,$CNY,Australia,Brexit,China,Currency Movement,Featured,newsletter