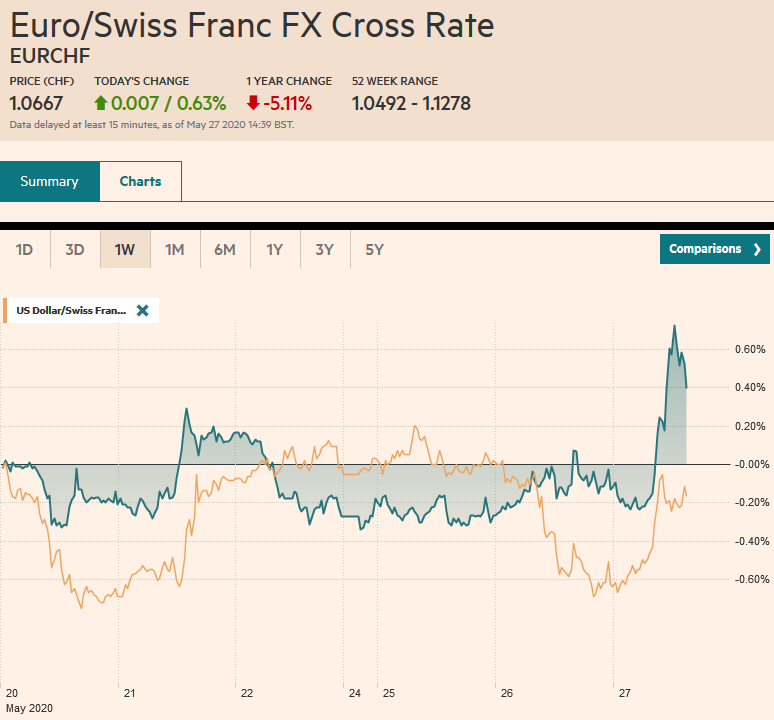

Swiss Franc The Euro has risen by 0.63% to 1.0667 EUR/CHF and USD/CHF, May 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The S&P 500 gapped higher yesterday, above the recent ceiling and above the 200-day moving average for the first time since early March. The momentum faltered, and it finished below the opening level and near session lows. The spill-over into today’s activity has been minor. The heightened tensions weighed on China and Hong Kong markets, but Japan, South Korea, Taiwan, and Indian equity markets rose. Europe’s Dow Jones Stoxx 600 is higher for the third consecutive session, the longest streak this month. US shares are also trading higher, and the S&P 500 looks poised to rechallenge

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, China, ECB, EU, Featured, Federal Reserve, Hong Kong, Japan, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.63% to 1.0667 |

EUR/CHF and USD/CHF, May 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The S&P 500 gapped higher yesterday, above the recent ceiling and above the 200-day moving average for the first time since early March. The momentum faltered, and it finished below the opening level and near session lows. The spill-over into today’s activity has been minor. The heightened tensions weighed on China and Hong Kong markets, but Japan, South Korea, Taiwan, and Indian equity markets rose. Europe’s Dow Jones Stoxx 600 is higher for the third consecutive session, the longest streak this month. US shares are also trading higher, and the S&P 500 looks poised to rechallenge yesterday’s high, leaving yesterday’s opening gap unfilled. Benchmark bond yields are a little lower, and the US 10-year is hovering around 68 bp. The greenback is bid against most of the major and emerging market currencies. Among the majors, the yen, the Canadian dollar, and New Zealand dollar are steady to higher, while the European complex, led by the Swiss franc, is nursing small losses. Turkey, Hungary, and South Africa led the losers among emerging market currencies. The Chinese yuan (onshore and offshore) fell to its lowest level of the year. Gold drifted to two-week lows a little above $1700, while July WTI is consolidating in $33.50-$34.30 range as Russia seems to be balking at extending the maximum output cuts beyond next month. |

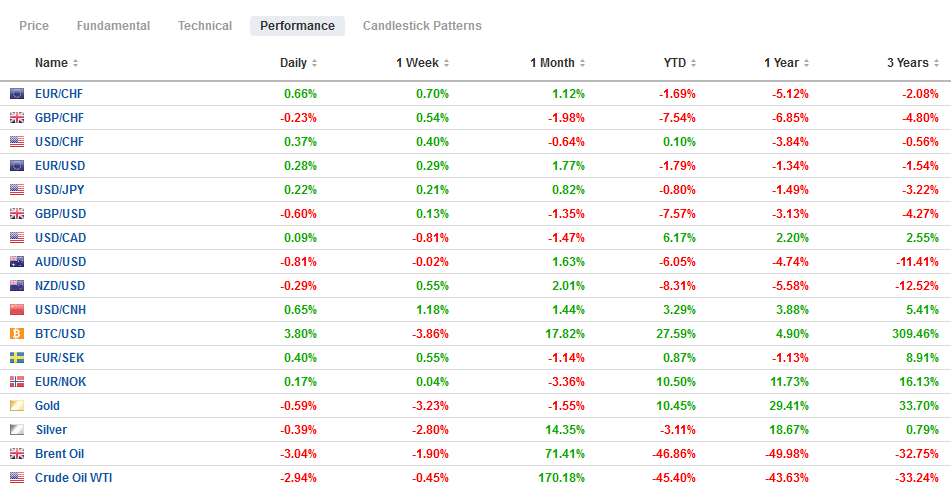

FX Performance, May 27 - Click to enlarge |

Asia Pacific

President Trump is threatening “very interesting” action against China by the end of the week. Apparently, under consideration are a new set of sanctions against officials, businesses, and financial firms over the effort to crack down on dissent in Hong Kong. There are actions the US could take, including limiting transactions and freezing assets. The US could suspend Hong Kong’s special trade privileges, but this seems potentially too disruptive for US companies and would punish Hong Kong more than China. Meanwhile, demonstrations and conflict with police have escalated in Hong Kong.

Pressure on the Hong Kong dollar is evident in the forward market. The 12-month forward points increased by almost 60 to 670. A week ago, they stood at 256. The 3-month forward points increased by almost 20 today to about 167. A week ago, they stood at 75. Separately, the PBOC set the dollar’s reference rate at CNY7.1092, while the bank models implied CNY7.1144. However, the dollar rose to almost CNY7.1630 to approach the CNY7.1850 peak last September. The dollar rose to almost CNH7.1770 against the offshore yuan. It peaked last September near CNH7.1965. Chinese officials do not appear to cause the yuan’s weakness but are not resisting it forcefully.

Separately, China reported a 4.3% decline in April industrial profits, almost a third of the decline that the median forecasts in the Bloomberg survey anticipated and what seems like an improvement after the nearly 35% decline in Q1. However, the performance of the state-owned enterprises suggests a more complicated picture. Profits in this sector fell 46% in the January to April period, a little worse than the 45.5% decline reported in Q1.

Nevertheless, with the latest reserve requirement cuts for large banks, and additional efforts for small and medium businesses, and signs of more fiscal support coming from the National People’s Congress, China is stepping up economic and financial efforts. At the same time, Japan’s cabinet has approved a JPY117 trillion supplemental budget with JPY72.7 trillion of fiscal outlays. South Korea is expected to deliver another 25 bp rate cut tomorrow (bringing the seven-day repo rate to 50 bp).

For the sixth consecutive session, the dollar stuck on the JPY107-handle. It has not traded below JPY107.30 since May 18. It neared JPY108 yesterday but backed off. Today there are $1.7 bln in options in the JPY107.80-JPY107.90 area that expire. If that is not a sufficient cap, there is another billion-dollar option at JPY108.15 that will also be cut. The Australian dollar is in a narrow range below yesterday’s high near $0.6675. There is an option for nearly A$635 mln at $0.6650 that expires today.

Europe

The European Commission appears to be combining the German-French proposal with the other proposal by Austria, Sweden, Denmark, and the Netherlands to advance a 750 bln euro fiscal support effort. It would include 500 bln euro in grants and 250 bln euros in loans. It seems a popular meme to see an EU bond as a step toward the mutualization of debt and a fiscal union. This seems exaggerated. There are already common obligations, such as bonds issued by the European Stabilization Mechanism and the European Investment Bank. The EU itself has issued bonds in the past.

ECB President Lagarde is laying the foundation for an increase in the central bank’s Pandemic Emergency Purchase Program next week. She cautioned today that the more mild scenario that had been considered was out of date and that the more likely scenario is the one that anticipates an 8-12% contraction this year. The internal debate seems to be over relaxing more of the self-imposed limits. The capital key has already been diluted for PEPP, and the issue limit of 1/3 has also been waved. There does not seem to be much interest in taking rates deeper into negative territory.

There has been much discussion of the Bank of England adopting negative rates. We have understood officials to be keeping that option on the table, which may help lower UK rates, such as last week’s 3-year Gilt auction that resulted in a negative yield. However, it does not seem to be imminent. More likely, the Bank of England will increase its bond purchases when it meets on June 18. The BOE’s chief economist, Haldane’s comments, were consistent with the idea that other policy options will be explored before negative rates.

The euro initially slipped to almost $1.0930 after stalling in front of $1.10 yesterday. However, with a running start in the European morning, the euro punched above $1.10 and above last week’s high to poke above the 200-day moving average (~$1.1015) for the first time since the end of March. The $1.1050 area may hold some offers, but there is little chart-based resistance ahead of $1.1160-$1.1200. Sterling, on the other hand, is firm but through late in the London morning, has been unable to surpass yesterday’s high near $1.2365. The next target above there is around $1.2425.

America

The US reports the May Richmond Fed survey and the Fed’s Beige Book for ahead of next month’s FOMC meeting. Nearly every survey (diffusion indices and sentiment surveys) have shown some moderation in the weakness since in April. The improvement has also mostly been better than expected. And yesterday’s it was reported that April new home sales, which were forecast to have imploded by nearly a quarter, eked out a small (0.6%) gain. Yes, there is little doubt that the world’s biggest economy has suffered a large hit in this quarter, but the data suggests ideas of a Q3 recovered may not be misplaced. Other data, including traffic patterns, are also pointing to a slight pick up in activity as the lockdowns ease. Canada and Mexico’s calendars are light today. Banxico issues its inflation report today, and coupled with the strength of the peso may spur speculation of another 50 bp rate cut at its next meeting.

Although Fed officials have played down the likelihood of negative rate policy in the US and the fed funds futures curve is not implying negative rates, the central bank may not be done. There is more virtual ink being devoted to the possibility of yield curve control, where the Fed would not target a certain amount of Treasuries to be bought, as it is now ($5 bln a day down from $75 bln a day at the peak) but to target another rate. The Bank of Japan targets the 10-year yield, and the Reserve Bank of Australia targets the three-year yield. If the Fed adopts such a tool, it would more likely target a short or intermediate coupon such as something between a two- and five-year maturity. It would help steepen the curve and send a signal that rates will remain low for some time.

The Canadian dollar joined the Australian dollar in breaking out of its recent range. The US dollar fell below the lower end of its two-month range against the Canadian dollar near CAD1.3850 yesterday. The losses are being extended today. The break of CAD1.38 is important from a technical perspective as it coincided with the halfway mark of this year’s range. The next retracement objective is near CAD1.3600. More immediately, a bid in the European morning was found near CAD1.3730. The old support near CAD1.38 now offers resistance. The greenback is also pushing below the halfway mark of this year’s range against the Mexican peso (~MXN22.15). A break of MXN22 would set the sights on the MXN21.00-MXN21.10 area. Mexico is reporting a record increase in virus cases and related fatalities. The peso’s strength largely reflects the broader risk-on mood.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, May 20: Fed Funds Futures No Longer Imply Negative Rates

FX Daily, May 20: Fed Funds Futures No Longer Imply Negative Rates

Overview: Another late sell-off of US equities, ostensibly on questions over Moderna’s progress on a vaccine, failed to deter equity gains in the Asia Pacific region. China was a notable exception, but the MSCI Asia Pacific Index rose for the fourth consecutive session. European shares are little changed, but reflects a split.

FX Daily, May 26: Fear is Still on Holiday

FX Daily, May 26: Fear is Still on Holiday

Overview: The heightened tensions between the US and China sapped risk-appetites before the weekend, but appear to be missing in action today. Equity markets have rebounded strongly. Nearly all the equity markets in the Asia Pacific region rose (India was a laggard) led by an almost 3% rally in Australia, which was seen as particularly vulnerable to the Sino-American fissure.

FX Weekly Preview: An Eventful Week Ahead

FX Weekly Preview: An Eventful Week Ahead

The US employment report on the first Friday of December usually marks the unofficial end of the year. The desks are often lighter and dealers are loath to jeopardize the year’s bonuses in thin and often erratic markets. This year is an exception. Next week features the first ECB meeting with Lagarde at the helm and the final FOMC meeting of the year.

FX Daily, January 23: ECB’s Strategic Review and the Coronavirus Command Investors’ Attention

FX Daily, January 23: ECB’s Strategic Review and the Coronavirus Command Investors’ Attention

The spread of the coronavirus and the lockdown in the epicenter in China has again sapped the risk-taking appetite in the capital markets. Asia is bearing the brunt of the adjustment. Tomorrow starts China’s week-long Lunar New Year celebration when markets will be closed, which may have also spurred today’s drama that aw the Shanghai Composite tumbled 2.75%, bringing the week’s loss to 3.2%, the most in five months.

FX Daily, April 30: ECB Takes Center Stage

FX Daily, April 30: ECB Takes Center Stage

Overview: Equities continue to recover even as deep economic contractions are reported. Yesterday, the US said Q1 GDP contracted at an annualized pace of 4.8%, while the eurozone reported today that output fell 3.8% quarter-over-quarter in Q1. Hong Kong and South Korea were closed, but the rest of the Asia Pacific bourses rallied strongly with several, including Australia and India, rising more than 2%.

FX Daily, May 19: Optimism Burns Eternal

FX Daily, May 19: Optimism Burns Eternal

Overview: Hopes for a vaccine and a German-French proposal to break the logjam at the EU for a joint recovery effort helped propel equities higher yesterday. There was strong follow-through in the Asia Pacific region, where most markets advanced by more than 1% today. However, the bloom came off the rose, so to speak, in Europe. After a higher opening, markets reversed lower, and the Dow Jones Stoxx 600 is off about 0.75% in late morning turnover.

FX Daily, May 21: Markets Pull Back after Flirting with Breakouts

FX Daily, May 21: Markets Pull Back after Flirting with Breakouts

Overview: New two and a half month highs in the S&P 500 yesterday failed to have much sway in the Asia Pacific region and Europe today as US-China tensions escalate and profit-taking set in. Perhaps it is a bit of "buy the rumor sell the fact" type of activity on the back of upticks in the preliminary PMI reading and hesitancy about pushing for what appeared to be breakouts.

FX Daily, May 22: US-China Escalation Sinks Hong Kong and Hits Risk Appetites

FX Daily, May 22: US-China Escalation Sinks Hong Kong and Hits Risk Appetites

Overview: The US has ratcheted up pressure on China on several fronts and has sapped risk appetites ahead of the weekend. Equity markets are lower across the world. Even in India, where the central bank unexpectedly cut the repo rate 40 bp, shares fell 0.7%. It was Hong Kong’s 5.5% that led the region lower. Europe’s Dow Jones Stoxx 600 is off around 1% in late morning turnover to pare this week’s gain to about 2.5%.

Tags: #USD,$CNY,China,ECB,EU,Featured,federal-reserve,Hong Kong,Japan,newsletter