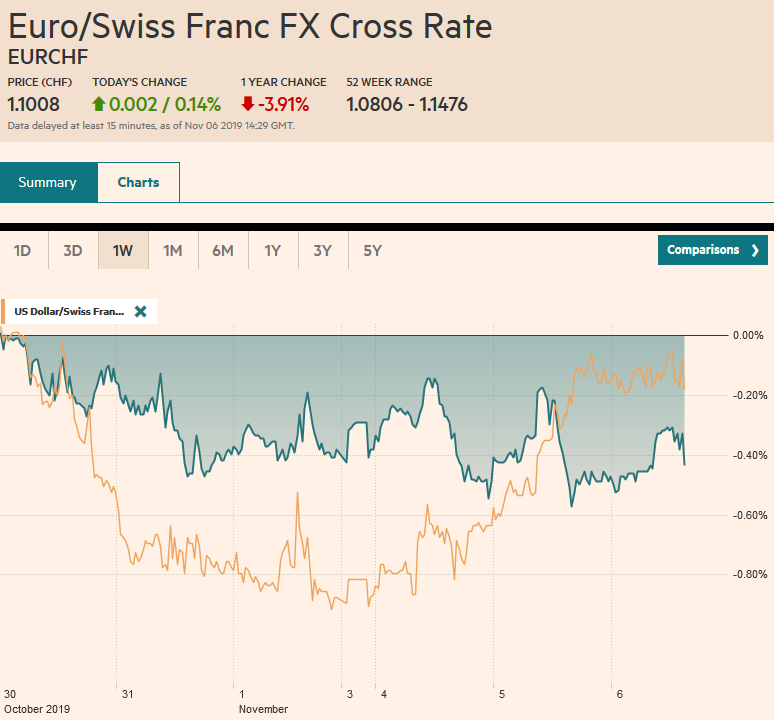

Swiss Franc The Euro has risen by 0.14% to 1.1008 EUR/CHF and USD/CHF, November 6(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Investors seem to be catching their collective breath today, and the global capital markets are consolidating recent moves. A notable exception is the Chinese yuan, which has continued to strengthen, and the dollar has slipped back below CNY7.0. Asia Pacific equities were mixed, and the four-day advance in the regional benchmark stalled today. That said, India has rallied to new highs. In Europe’s Dow Jones Stoxx 600 is firm but struggling to maintain the upside momentum that has lifted it for the past three sessions. US shares are little changed. Benchmark 10-year yields played

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, 4.) Marc to Market, Brazil, Currency Movement, EUR/CHF, Europe, Eurozone Markit Composite PMI, Eurozone Retail Sales, Eurozone Services PMI, Featured, FX Daily, Huawei, newsletter, USD, USD/CHF

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Swiss FrancThe Euro has risen by 0.14% to 1.1008 |

EUR/CHF and USD/CHF, November 6(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

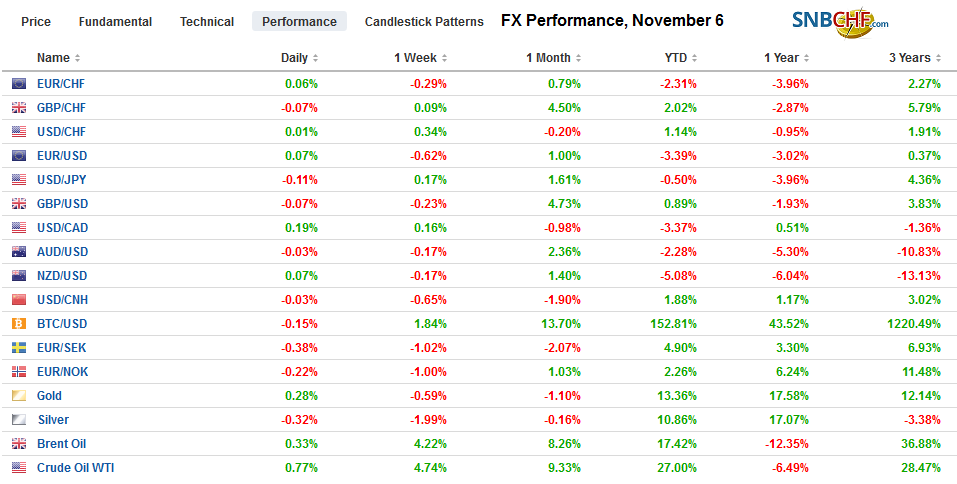

FX RatesOverview: Investors seem to be catching their collective breath today, and the global capital markets are consolidating recent moves. A notable exception is the Chinese yuan, which has continued to strengthen, and the dollar has slipped back below CNY7.0. Asia Pacific equities were mixed, and the four-day advance in the regional benchmark stalled today. That said, India has rallied to new highs. In Europe’s Dow Jones Stoxx 600 is firm but struggling to maintain the upside momentum that has lifted it for the past three sessions. US shares are little changed. Benchmark 10-year yields played catch-up in Asia after the US surge yesterday. European yields are narrowly mixed, and the US 10-year yield is hovering around 1.85%. The dollar is consolidating yesterday’s gains against the major currencies. Outside of the yuan, which is the strongest of the emerging market complex, most of the liquid and accessible emerging market currencies are nursing small losses, though eastern and central European currencies are resisting the pull. Oil prices are a little heavier after reaching six-week highs yesterday, and gold has steadied after posting its biggest loss in over a month yesterday. |

FX Performance, November 6 - Click to enlarge |

Asia Pacific

It is becoming clearer that mission accomplished claims about what has been dubbed phase one of the US-China trade agreement is anything but. Indeed, the whole focus on where the pact should be signed given Santiago canceled the APEC meeting due to social unrest is a distraction. China appears to have gotten the upper hand. It is not accepting the suspension of the threatened mid-December tariff. This was a chit Trump created in a pique that would hurt US consumers. It is insisting on rolling back some earlier tariffs. So far, the US has not formally responded.

China issued sold its first euro-denominated bond since 2004. It sold 4 bln euros of 7, 12, and 20- year debentures. In all, the offering was over-subscribed five-fold, and the pricing (e.g., the 7-year bond was 30 bp above mid-swaps) was tighter than expected.

There is much discussion about the possible coordination of monetary and fiscal policy. A push back has been a defense of central bank independence. However, in Japan, where the central bank often is perceived to be among the least independent of major central banks, enhanced coordination is possible. This was precisely BOJ Governor Kuroda’s point that seems to have somewhat wide application. Kuroda argued that the ultra-low rates that have been engineered by the BOJ make government spending even more powerful.

The dollar closed above its 200-day moving average against the yen yesterday (~JPY109.05), for the first time in six months. It was unable to take out the recent high (~JPY109.30) and has backed off a little today. Initial support is pegged in the JPY108.50-JPY108.70 area. There are two expiring option strikes to note: $485 mln at JPY109.20 and $780 mln at JPY108.75. The Australian dollar is trading quietly well within yesterday’s ranges. The 200-day moving average, which has capped rallies this year, is found near $0.6950. Support is seen near $0.6875. For the second consecutive session, the PBOC set the dollar’s reference rate a little weaker than expected, and this emboldened the market to take the greenback through CNY7.0, which surprises many observers. The offshore market recognizes the risk of a trap and was reluctant to extend yesterday’s dollar losses much through CNH6.99. The dollar edged higher against the Thai baht after the central bank delivered the as expected 25 bp rate cut (benchmark is now 1.25%). It is the second cut here in H2.

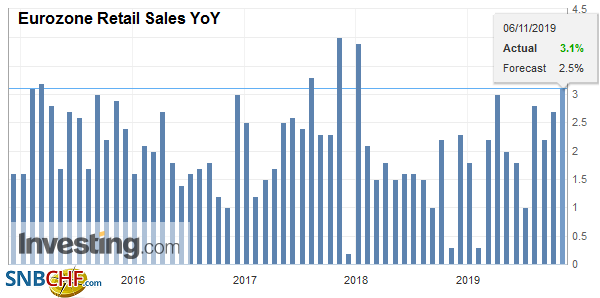

EuropeThe emerging meme that Europe may be past the worst of its slowdown was supported by today’s data. Specifically, Germany’s final PMI reading showed improvement from the flash estimates for services and the composite. Separately, Germany reported that factory orders surged in September. The 1.3% increase contrasts with the median forecast in the Bloomberg survey of 0.1%, and to August series was revised to -0.4% from -0.6%. |

Eurozone Retail Sales YoY, September 2019(see more posts on Eurozone Retail Sales, ) Source: investing.com - Click to enlarge |

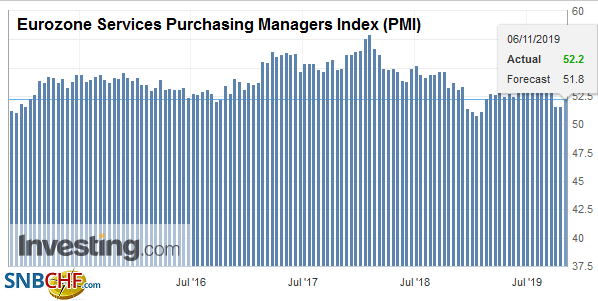

| The final French services and composite PMI was in line with the flash estimates and showed sequential improvement. Italian services rebounded to 52.2 from 51.4 in September, but the poor manufacturing news (47.7 from 47.8, reported last week) limited the composite gain to 50.8 (from 50.6). Spain, which has been one of the bright spots, disappointed with (services PMI 52.7 from 54.3, and the composite fell to 51.2 from 51.7). Note that Spain goes back to the polls, unable to form a government with the existing configuration of parliament. It is not clear that the election this weekend will produce significant changes. The concern that the manufacturing weakness in the eurozone was spilling over to drag down services seems a bit exaggerated. The EMU services PMI rose to 52.2 from the 51.8 flash reading and 51.6 in September. |

Eurozone Services Purchasing Managers Index (PMI), October 2019(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

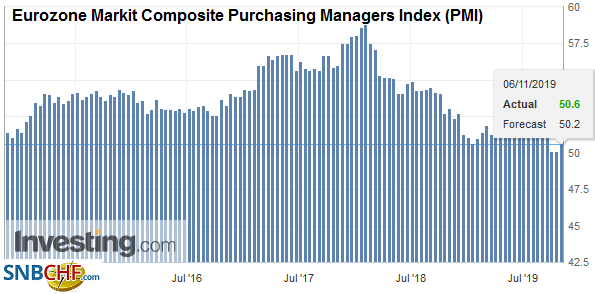

| The composite rose to 50.6 from 50.2 flash estimate and 50.1 in September. |

Eurozone Markit Composite Purchasing Managers Index (PMI), October 2019(see more posts on Eurozone Markit Composite PMI, ) Source: investing.com - Click to enlarge |

Germany’s Finance Minister Scholz signaled a new initiative by Germany to renew efforts to move forward on the banking union. It would include some deposit reinsurance program that would enhance national efforts. It would require uniform taxation of banks in the EU and common insolvency and resolution procedures, which have gradually been adopted. It is still early days, but the shift in the German stance is potentially a game-changer.

The euro’s pullback is a bit more than we expected, but it is holding the (38.2%) retracement of the rally that began early last month from below $1.09. A break of the $1.1065 area could also confirm the potential double top in place near $1.1175. The importance of the pattern is the measuring objective, and it would project toward $1.0950. A close above $1.11 would help heal the technical damage inflicted yesterday. Sterling is in about a quarter-cent range below $1.29.

America

China’s needs can outstrip its political posturing. This has seen true of its agriculture purchases from the US, which have not waited for a phase 1 agreement. The same is true now for Canada. It what appeared to be a “punishment” for holding Huawei’s Meng at the request of the US. China had stopped shipments of meat from Canada several months ago. That ban appears to have been lifted. In 2018, China bought about C$600 mln of Canada-sourced meat. China was Canada’s third-largest pork market. Although driven by China’s needs, it represents a slight de-escalation. Meng’s extradition case is expected to return to the courtroom early next year.

Brazil holds an auction today for four deep-water fields that may hold massive oil deposits that potentially are bigger than Norway and Mexico’s oil reserves. It could raise $25 bln. Separately, WTI for December reached six-week highs yesterday near $57.50 a barrel and poking through the 200-day moving average on an intraday basis (~$57.40) for the second consecutive session. The API estimated that US oil inventories rose by more than four million barrels last week. The more robust EIA estimate is expected to be a built of less than a million barrels. The four-week average is a little more than four million barrels.

In addition to the EIA energy report, the US provides estimates for Q3 productivity and unit labor costs. These are derived from the first estimate of Q3 GDP reported last week. Productivity is likely to have slowed to around 1%. The rise in unit labor costs (compensation and productivity) is projected to have slowed from the 2.6% pace in Q2. These are not the kind of economic reports that move the market. The Fed’s Williams, Evans, and Harker take to the microphones today. However, there is a broad understanding that the Federal Reserve has moved to the sidelines, and a cut next month is highly unlikely. The bar is set at a material change in the economic outlook. Canada reports its IVEY survey results and Mexico reports on its vehicle production and export figures.

The US dollar is trading in the upper end of yesterday’s range against the Canadian dollar. The greenback is trading roughly CAD1.3145-CAD1.3170 through the European morning. We still see the greenback correcting higher after sliding in the second half of October. Barring a break of CAD1.3100, we see the risk favoring a move toward CAD1.3230. The US dollar appears to be carving out a round bottom against the Mexican peso but is running into resistance in the MXN19.25-MXN19.26 area that also houses the 200-day moving average. A move above there would target the MXN19.34-MXN19.44 band. A bill allowing Mexico’s president to be recalled after three years (2022 for AMLO) passed the lower chamber of Congress yesterday. It now needs to be ratified by the state legislatures, which is thought likely. It could inject a little more political uncertainty going forward. The Dollar Index stalled near 98.00 yesterday and within a couple thousandths of an index point of the high from late October. A break of 97.45-97.55 would suggest the upper end of its range has been found.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$CNY,Brazil,Currency Movement,EUR/CHF,Europe,Eurozone Markit Composite PMI,Eurozone Retail Sales,Eurozone Services PMI,Featured,FX Daily,Huawei,newsletter,USD/CHF