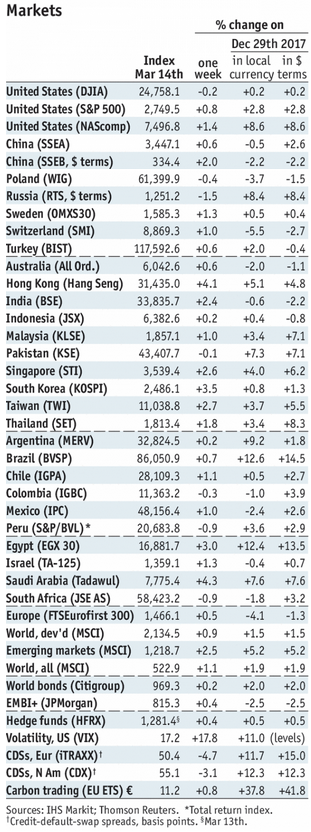

Stock Markets EM ended Friday under renewed selling pressures, and capped off a mostly softer week. COP, THB, and TWD were the best performers last week, while TRY, RUB, and ZAR were the worst. Despite a widely expected 25 bp hike, this week’s FOMC meeting still has potential to weigh on EM. Stock Markets Emerging Markets, March 14 Source: economist.com - Click to enlarge Poland Poland reports February industrial and construction output and PPI Monday. Data are expected to slow from January. Real retail sales will be reported Tuesday, which are expected to remain steady at 7.7% y/y. Yet inflation continues to fall. CPI rose only 1.4% y/y in February, the lowest since December 2016 and below the 1.5-3.5%

Topics:

Win Thin considers the following as important: Brazil, Chile, Colombia, emerging markets, Featured, Indonesia, Malaysia, Mexico, newslettersent, Philippines, Poland, Russia, Singapore, South Africa, Taiwan, win-thin

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Stock MarketsEM ended Friday under renewed selling pressures, and capped off a mostly softer week. COP, THB, and TWD were the best performers last week, while TRY, RUB, and ZAR were the worst. Despite a widely expected 25 bp hike, this week’s FOMC meeting still has potential to weigh on EM. |

Stock Markets Emerging Markets, March 14 Source: economist.com - Click to enlarge |

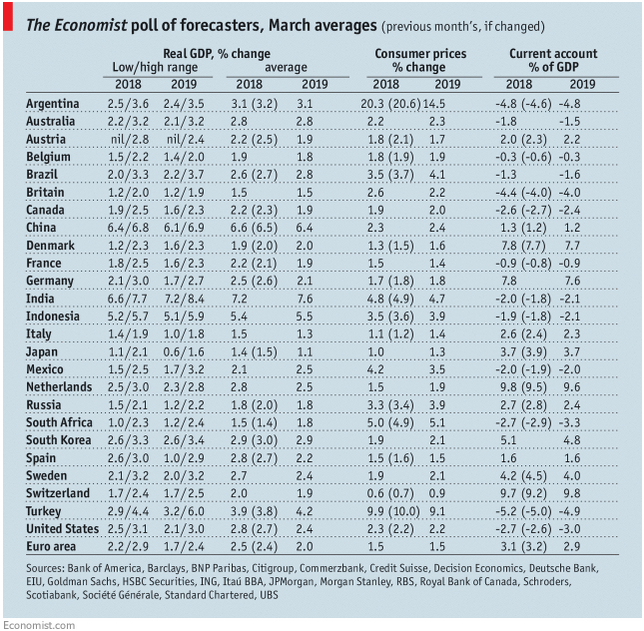

PolandPoland reports February industrial and construction output and PPI Monday. Data are expected to slow from January. Real retail sales will be reported Tuesday, which are expected to remain steady at 7.7% y/y. Yet inflation continues to fall. CPI rose only 1.4% y/y in February, the lowest since December 2016 and below the 1.5-3.5% target range. Next policy meeting is April 11, no change expected as the bank now sees steady rates until at least H2 2019 or even 2020. ChileChile reports Q4 GDP Monday, which is expected to grow 2.9% y/y vs. 2.2% in Q3. The central bank meets Tuesday and is expected to keep rates steady at 2.5%. CPI rose 2.0% y/y in February, right at the bottom of the 2-4% target range. If the economy turns down, low inflation will give the central bank room to resume the easing cycle. TaiwanTaiwan reports February export orders Tuesday, which are expected to rise 2.8% y/y vs. 19.7% in January. The central bank meets Thursday and is expected to keep rates steady at 1.375%. February IP will be reported Friday, which is expected to rise 2.5% y/y vs. 10.9% in January. South AfricaSouth Africa reports February CPI and Q4 current account data Tuesday. Headline CPI is expected to rise 4.1% y/y vs. 4.4% in January, while the current account deficit is expected at -2.0% of GDP vs. -2.3% in Q3. If inflation comes in at consensus, it would be the lowest since March 2015 and in the bottom half of the 3-6% target range. SARB is likely to resume the easing cycle at the March 28 policy meeting. January retail sales will be reported Thursday, which are expected to rise 5.9% y/y vs. 5.3% in December. Moody’s is scheduled to issue its rating update Friday. ColombiaColombia central bank meets Tuesday and is expected to keep rates steady at 4.5%. However, the market is split. Of the 14 analysts polled by Bloomberg, 9 see steady rates, 4 see a 25 bp cut, and 1 sees a 50 bp cut. CPI rose 3.4% y/y in February, the lowest since October 2014 and within the 2-4% target range. The bank just cut 25 bp at the last meeting in January, and so it might pause for a month. MalaysiaMalaysia reports February CPI Wednesday, which is expected to rise 2.0% y/y vs. 2.7% in January. Bank Negara does not have an explicit inflation target. However, low inflation should allow it to remain on hold at the next policy meeting May 10. BrazilCOPOM meets Wednesday and is expected to cut rates 25 bp to 6.5%. Mid-March IPCA inflation and February current account data will be reported Friday. Inflation is expected to rise 2.87%y/y vs. 2.86% in mid-February. If so, this would still close to the bottom of the 2.5-6.5% target range. IndonesiaBank Indonesia meets Thursday and is expected to keep rates steady at 4.25%. CPI rose 3.2% y/y in February, the lowest since December 2016 and near the bottom of the 3-5% target range. While the bank has expressed concern about rising inflation, data should allow it to remain on hold in H1. PhilippinesBangko Sentral ng Pilipinas meets Thursday and is expected to keep rates steady at 3.0%. However, the market is split. Of the 11 analysts polled by Bloomberg, 7 see steady rates and 4 see a 25 bp hike. CPI rose 4.5% y/y in February, the highest since August 2014 and above the 2-4% target range. After switching to a 2012 base year, CPI rose 3.9% y/y in February vs. 3.4% in January, which muddies the picture. We see risk of a hawkish surprise. MexicoMexico reports mid-March CPI Thursday, which is expected to rise 5.06% y/y vs. 5.45% in mid-February. If so, inflation would move closer to the 2-4% target range. Yet the bank may be under pressure to deliver another hike at the next policy meeting April 12. It will be a tough call, and may depend in large part on how the peso is trading then. SingaporeSingapore reports February CPI Friday, which is expected to rise 0.4%y/y vs. 0.0% in January. The MAS does not have an explicit inflation target. However, low inflation should allow it to remain on hold at next month’s semi-annual policy meeting. RussiaCentral Bank of Russia meets Friday and is expected to cut rates 25 bp to 7.25%. CPI rose 2.2% y/y in February, a record low and well below the 4% target. As such, we believe the easing cycle can continue through mid-year. Putin’s reelection over the weekend should have no policy implications. |

GDP, Consumer Inflation and Current Accounts Source: economist.com - Click to enlarge |

Tags: Brazil,Chile,Colombia,Emerging Markets,Featured,Indonesia,Malaysia,Mexico,newslettersent,Philippines,Poland,Russia,Singapore,South Africa,Taiwan,win-thin