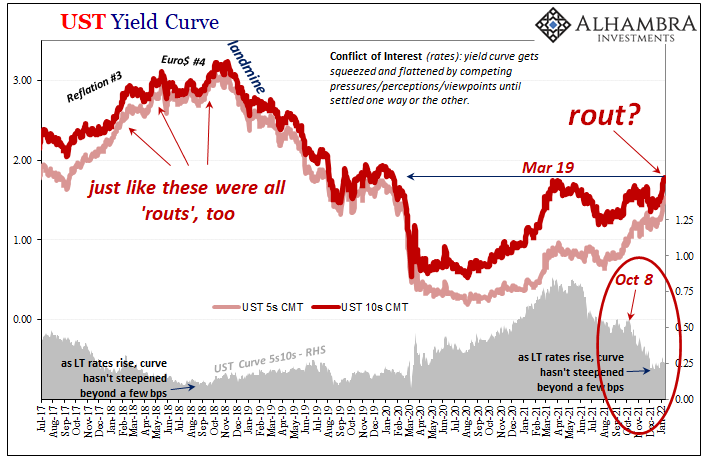

How is that US Treasury rates out in the independent longer end of the yield curve have now “suffered” a seven percent CPI to go along with double taper and triple maybe quadruple (if the whispers are to be believed) rate hikes this year, yet have weathered all of that allegedly bond-busting brutality with barely a market fluctuation? The short end of the curve, as noted here, is being pressured by only the last of those things, rate hikes, and from them creating the malodorous Conundrum No5. Part of the explanation for this can still be found in the word “transitory.” The flattening curve here and elsewhere acknowledges this, how despite the US CPI achieving its lofty status it still is not inflation (OK, Emil, it’s not monetary inflation). . This last point

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, China, Consumer Prices, Core CPI, CPI, currencies, Deflation, disinflation, economy, Featured, Federal Reserve/Monetary Policy, inflation, Markets, newsletter, PPI, producer prices

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| How is that US Treasury rates out in the independent longer end of the yield curve have now “suffered” a seven percent CPI to go along with double taper and triple maybe quadruple (if the whispers are to be believed) rate hikes this year, yet have weathered all of that allegedly bond-busting brutality with barely a market fluctuation? The short end of the curve, as noted here, is being pressured by only the last of those things, rate hikes, and from them creating the malodorous Conundrum No5.

Part of the explanation for this can still be found in the word “transitory.” The flattening curve here and elsewhere acknowledges this, how despite the US CPI achieving its lofty status it still is not inflation (OK, Emil, it’s not monetary inflation). |

. |

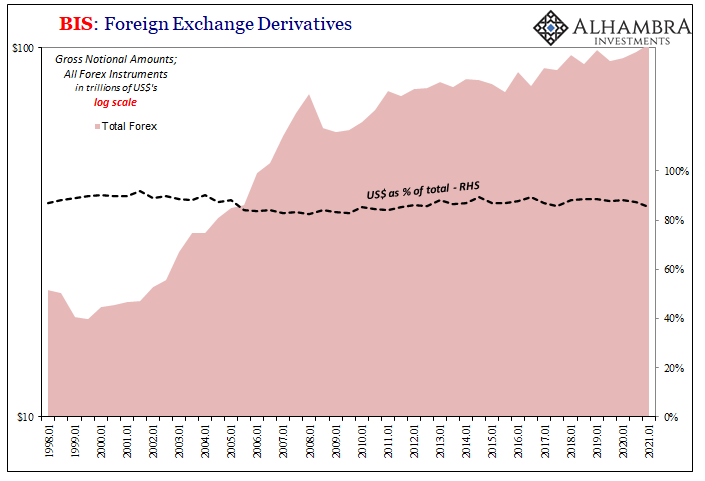

| This last point the purpose behind my recent as well as incoming review of the BIS derivatives data – the real money should there have been any chance.

There wasn’t. |

. |

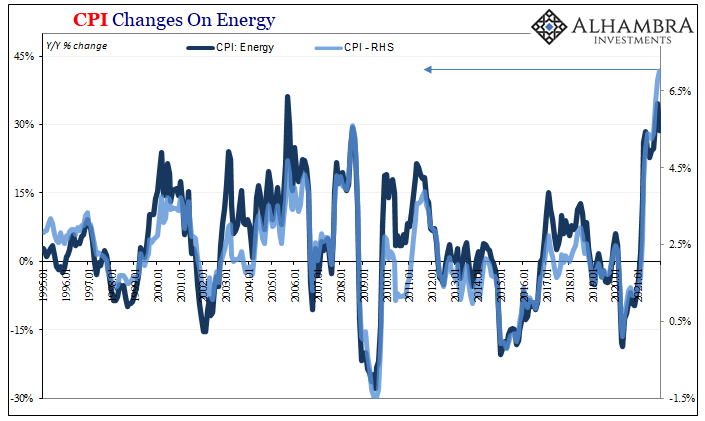

| So, what is going on with prices, and what does “everyone” seem to be missing about them?If your survey doesn’t go past the US headline CPI, then you’re left with a conundrum (especially since Jay Powell’s FOMC isn’t really hawkish about them, either, but rather the prospect Americans will normalize to them along with an historically faulty unemployment rate doing what it has done again). The rate is undoubtedly huge, the highest in forty years.

On top of that, in December while reaching a 7.04% year-over-year rate, it also decoupled from gasoline. |

. |

. |

|

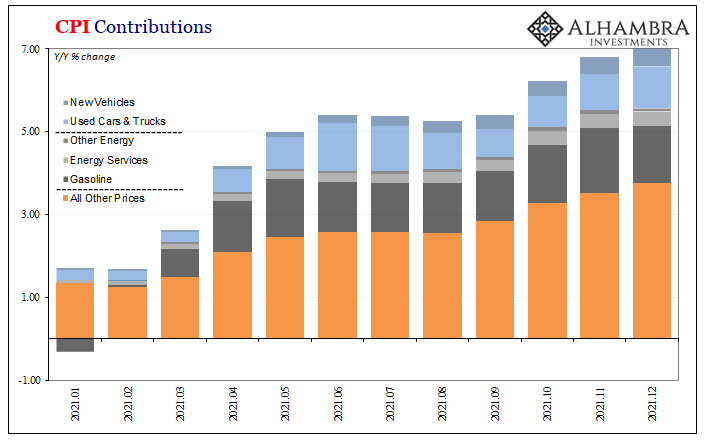

| Though, as noted previously, the CPI has been boosted and amplified by used car prices along with those for gasoline, that wasn’t as much the case in December. For the first time in a very, very long time, too, the headline CPI (y/y) accelerated during the same month when the index for energy prices decelerated (month-over-month they were down).

Even though car prices made up much of the difference in the index, as you can see above the prices of other things beside gasoline and vehicles have gone up, too. The core CPI rate – which removes energy and food, though not automobiles – registered an enormous (and painful) 5.45% year-over-year gain for December 2021. |

. |

| Clearly, it’s not just the energy sector (nor Big Food gouging consumers on beef and vegetable prices, as some politicians have recently alleged).

Even so, already in the core CPI you can see how it has changed speed. It had first slowed way down around July before reaccelerating in October if at a lesser rate than the earlier bulge – or Emil’s camel hump – around Uncle Sam’s Helicopter #3. Thus, a smaller yet still noticeable third hump to round out Q4 2021. But when we move away from prices of goods and into services, Hump #3 (since I’m numbering pretty much everything these days, why not?) appears entirely a one-off itself. The CPI data for services less rent depicts a very different end of year result. In fact, outside of October, consumer prices that aren’t for goods have slowed way down again to among the lower rates of increase. |

. |

| The third hump here is smaller, more importantly much skinnier.

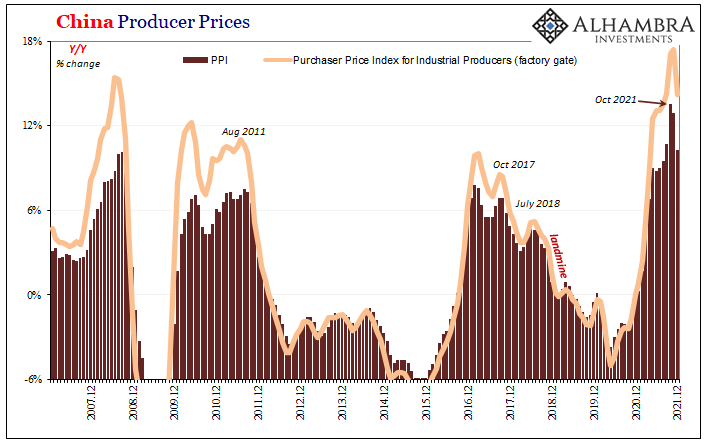

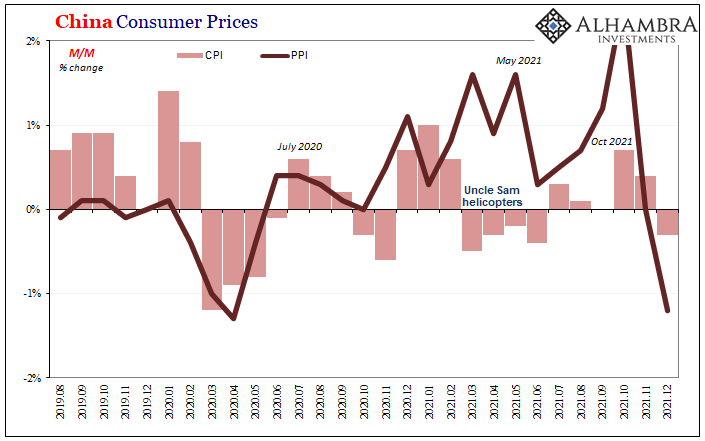

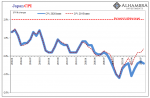

What this suggests is exactly that; transitory outside of some goods. But what about outside of the US? Remember, too, how inflation is both a monetary phenomenon as well as a global one united by a global monetary system. Again, this the purpose of reviewing all manner of global money proxies like TIC, Z1, and the BIS collection of global derivatives. The yield curve even for US Treasuries is a sorting mechanism that takes account of so many other factors beyond domestic goods prices. Since the Chinese also released their consumer price data today, along with their producer price estimates, those figures are both handy and topical. |

. |

| Like other producer prices from around the world, China’s had surged but only up to October – yes, there’s that month again. And while factory gate prices held up in November, neither would in December.

Though the year-over-year rates remain unusually high, they’ve dropped considerably from their top in a very short time; which, as you can see above, typically has meant a “cycle” peak. Not only that, if you compare China’s producer prices to the US services (less rent) CPI, what emerges is a common outline; all three camel humps. |

. |

. |

|

| Like US services, Chinese producer and factory prices came down dramatically first in November and then even more during December; here the third hump was higher in China but equally skinny. The outlier is US goods.

Moving over to China’s consumer prices, what’s missing – or mistimed – is that second hump which otherwise had matched up nicely with US Helicopter #2 in other subsets. In China, there was no impact from it because, why would there be? Since it did have at least a solid correlation with China’s producer prices, we’re really beginning to zero in on what this likely means insofar as “transitory” might be concerned. |

. |

| In other words, the earlier frenzy of American consumer buying unleashed by Helicopter #2 had pushed up producer prices globally to go along with consumer prices domestically, goods as well as services, but those effects really do seem to be waning the further away you go in time, in geography, and travel beyond US consumer goods prices.

Waning but not yet extinguished: there was a temporary restart around October perhaps related to the pre-Christmas rush for goods, the panic over better-order-early-or-Christmas-is-canceled when spooked shoppers further confounded the still-tangle of supply issues. After that early holiday spending, however, prices around the world apart from US goods have decelerated and in China they’ve outright declined. |

. |

| As I began, if your view of “inflation” is only US goods focused exclusively on the multi-decade high seven, Taper Rejection’s growing Conundrum No5 just might seem irrational. Looking beyond US goods to the entire vast majority of what’s left of global “inflation”, believing specifically US goods prices are representative of inflation or even “inflation”, that is what’s irrational. |

. |

There’s quite a lot of disinflation indicated in these other parts already, with November and then December quieting way down across a the global economy.

Furthermore, this downshift predates omicron by at least a month. In fact, remember how yield curves had shifted to even flatter during October almost certainly anticipating these global outcomes – prices along with what they might signal for economic activity.

Transitory isn’t just some buzzword Jay Powell will maybe soon regret abandoning, it is becoming more and more evident in the data even if that data doesn’t yet include prices for US goods. It’s already in services, however, and then corroborated by quite a lot more evidence globally.

And since there was never any indication of money for it to have been inflation, how else could it really have turned out? Uncle Sam tried his best, but atop the monetary throne still sits the eurodollar.

You Might Also Like

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

2021-12-25

If there is a better, more fitting way to head into the Christmas holiday in the United States than by digging into the finances and monetary flows of the People’s Bank of China, then I just don’t want to know what it is. Contrary to maybe anyone’s rational first impression that this is somehow insane, there’s much we can tell about the state of the world, the whole world and its “dollars”, right from this one key data source.

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century

2021-12-22

Have oil producers shot themselves in the foot, while at the same time stabbing the global economy in the back? It’d be quite a feat if it turns out to be the case, one of those historical oddities that when anyone might honestly look back on it from the future still hung in disbelief. Let’s start by reviewing just the facts.

Testing The Supply Chain Inflation Hypothesis The Real Money Way

Testing The Supply Chain Inflation Hypothesis The Real Money Way

2021-12-18

Basic intuition says this is a no-brainer. Producer prices rise, businesses then pass along these higher input costs to their customers in the form of consumer price “inflation” so as to preserve profits. This is the supply chain hypothesis. Statistically, we’d therefore expect the PPI to lead the CPI.And this was expected for much of Economics’ history, taken for granted as one of those self-evident truths (kind of like the Inflation Fairy). After the dreadful experience of the Great Inflation, and the dreadful performance of Economics during it, a few scholars went back to take a second look.One of the most cited contrary studies was published in 1995 by Todd Clark of the Federal Reserve’s branch in Kansas City (Economic Review; vol. 80, issue Q III, 25-39). Using econometric evidence,

Short Run TIPS, LT Flat, Basically Awful Real(ity)

Short Run TIPS, LT Flat, Basically Awful Real(ity)

2021-10-28

Over the past week and a half, Treasury has rolled out the CMB’s (cash management bills; like Treasury bills, special issues not otherwise part of the regular debt rotation) one after another: $60 billion 40-day on the 19th; $60 billion 27-day on the 20th; and $40 billion 48-day just yesterday.

Perfect Time To Review What Is, And What Is Not, Inflation (and why it matters so much)

Perfect Time To Review What Is, And What Is Not, Inflation (and why it matters so much)

2021-10-13

It is costing more to live and be, so naturally people are looking for who it is they need to blame. Maybe figure out some way to stop it. You know and feel for the basics since everyone’s perceptions begin with costs of just living. This is what makes the subject of inflation so difficult, even more so in the era of QE.

August Avoids Zero In JGB’s

August Avoids Zero In JGB’s

2021-09-28

Central banks and their staffs have long been accused of trying to hide inflation. This allegation had been a staple of their critics, those charging reckless monetary policies for creating “too much” money that had allegedly been causing price imbalances all over the financial map.

What’s Real Behind Commodities

What’s Real Behind Commodities

2021-09-08

Inflation is sustained monetary debasement – money printing, if you prefer – that wrecks consumer prices. It is the other of the evil monetary diseases, the one which is far more visible therefore visceral to the consumers pounded by spiraling costs of bare living. Yet, it is the lesser evil by comparison to deflation which insidiously destroys the labor market from the inside out.

Weekly Market Pulse: As Clear As Mud

Weekly Market Pulse: As Clear As Mud

2021-07-19

Is there anyone left out there who doesn’t know the rate of economic growth is slowing? The 10 year Treasury yield has fallen 45 basis points since peaking in mid-March. 10 year TIPS yields have fallen by the same amount and now reside below -1% again. Copper prices peaked a little later (early May), fell 16% at the recent low and are still down nearly 12% from the highs.

Tags: Bonds,China,Consumer Prices,Core CPI,CPI,currencies,Deflation,disinflation,economy,Featured,Federal Reserve/Monetary Policy,inflation,Markets,newsletter,PPI,producer prices