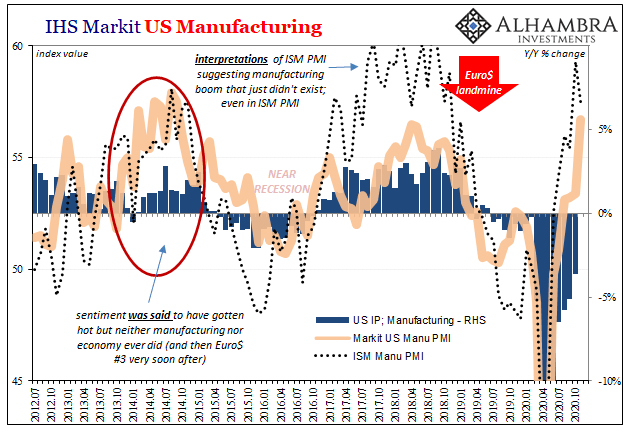

The ISM reported a small decline in its manufacturing PMI today. The index had moved up to 59.3 for the month of October 2020 in what had been its highest since September 2018. For November, the setback was nearly two points, bringing the headline down to an estimate of 57.5. At that level, it really wasn’t any different from where it had been at its multi-year high the month before. Neither are indicative of any sort of “V” shaped recovery, or any shaped recovery. Rebound, yes, but that’s very different. That point may have been best described by the key subcomponent most responsible for the index’s top-level decline. IHS Markit US Manufacturing, 2012-2020 - Click to enlarge The manufacturing employment estimate fell back below 50 yet again. In fact, it had

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, CARES Act, corporate profits, currencies, economy, employment, Featured, Federal Reserve/Monetary Policy, gdi, GDP, jobless claims, Labor market, Markets, newsletter, paycheck protection program, U.S. ISM Manufacturing PMI, Unemployment

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The ISM reported a small decline in its manufacturing PMI today. The index had moved up to 59.3 for the month of October 2020 in what had been its highest since September 2018. For November, the setback was nearly two points, bringing the headline down to an estimate of 57.5.

At that level, it really wasn’t any different from where it had been at its multi-year high the month before. Neither are indicative of any sort of “V” shaped recovery, or any shaped recovery. Rebound, yes, but that’s very different. That point may have been best described by the key subcomponent most responsible for the index’s top-level decline. |

IHS Markit US Manufacturing, 2012-2020 - Click to enlarge |

| The manufacturing employment estimate fell back below 50 yet again. In fact, it had been above that level only once (October) since July 2019. The manufacturing sector, seriously struggling long before COVID, appears to be caught up in the same imbalances unfavorable to getting workers back on their feet even during the reopening frenzy.

Not enough work because rebound doesn’t necessarily mean recovery. In many cases, as we’ve seen since 2008, it merely means lack of further contraction at this moment. |

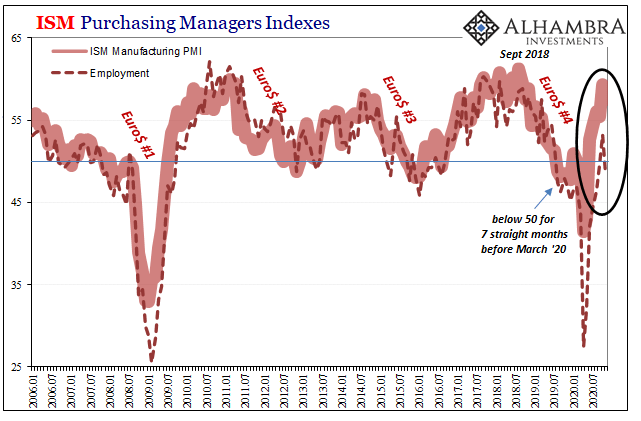

ISM Purchasing Managers Indexes, 2006-2020 - Click to enlarge |

| Not just manufacturers, it might at first seem to be a glaring disconnect between other measures of the economic rebound, including mainstream interpretations of this ISM headline. But a relatively slow increase off a very low trough, as in earlier this year, isn’t the sort of economic recovery trend which would produce a robust labor market comeback.

On the contrary, if businesses perceive a lackluster upturn, as these PMI numbers actually suggest, then they will continue to be cautious especially when it comes to their greatest cost component (and liquidity risk) – just as the slowdown in all the employment data demonstrates (save the unemployment rate which is once more caught up in the participation problem’s apparent second act). And it doesn’t really matter what “stimulus” has been unleashed along the way. |

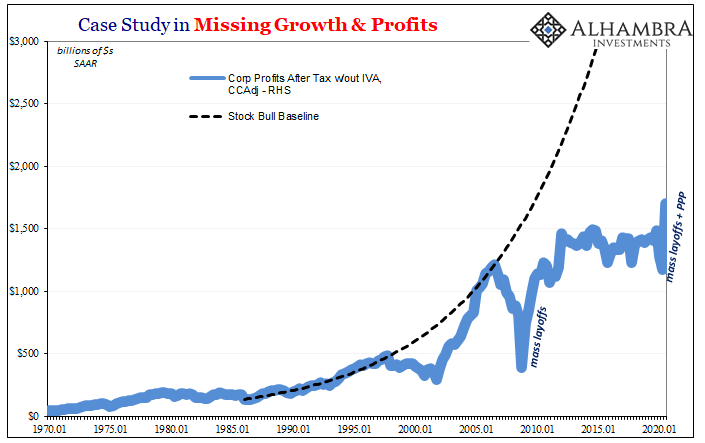

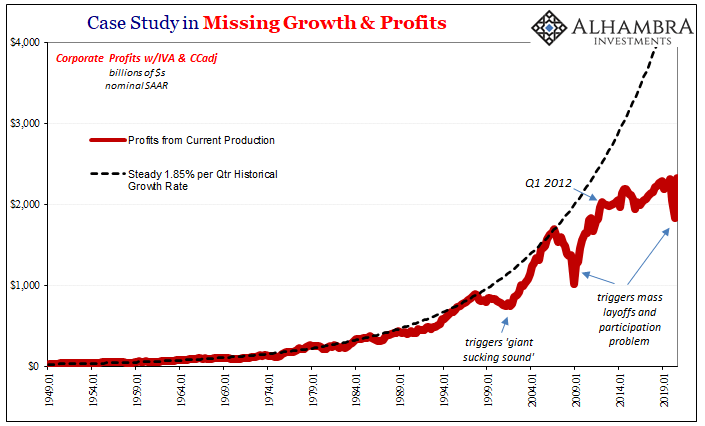

Case Study in Missing Growth & Profits, 1970-2020 - Click to enlarge |

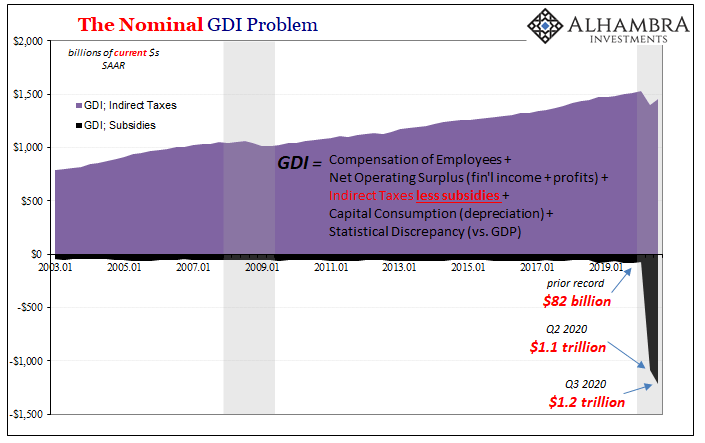

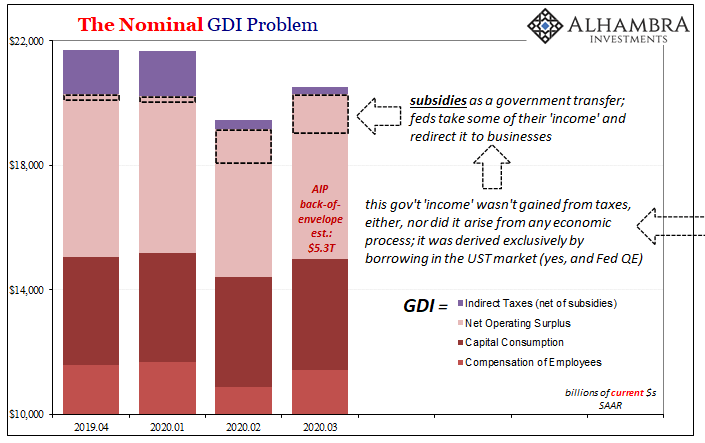

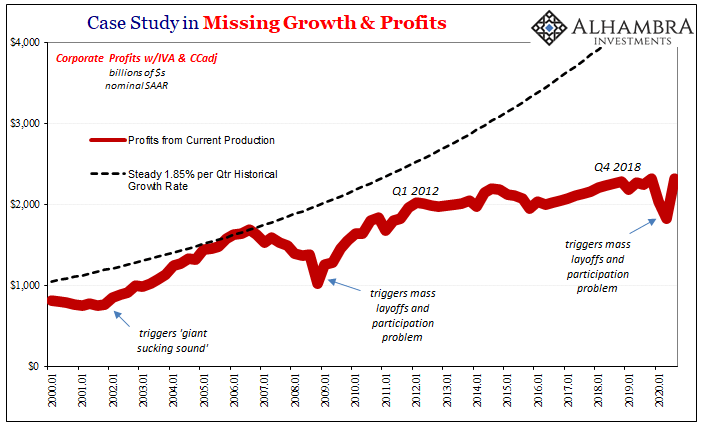

| Late last month, the Bureau of Economic Analysis (BEA) further proved the lack of stimulation in the massive government subsidies which have been paid out since the CARES Act was passed in late March. The effect in the economic accounting, as in reality, was to make things seem better than they really are.

In this case, literal jobs saved for once. Saved for what, though? This is not the same thing as recovery. In its second estimates for Q3 GDP, the BEA also provides the first set of estimates for corporate profits within the US economy. In some classifications, these absolutely surged, skyrocketed; and I don’t just mean from Q2 to Q3. In the case of after tax corporate profits (not including inventory valuations and deductions for amortized capital expenditures), the estimated level in Q3 2020 was a whopping 21% better than it had been in Q3 2019. |

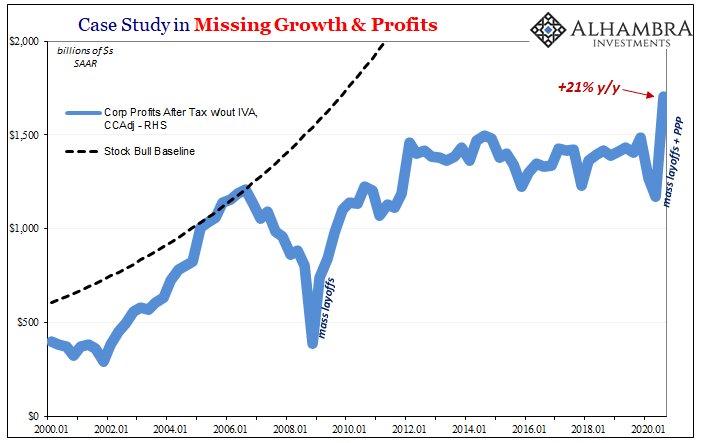

Case Study in Missing Growth & Profits, 2000-2020 - Click to enlarge |

| Not only is that the highest on record, it shatters the previous high from way back in 2014 (though still woefully short of the pre-crisis bull market trend).

So, why aren’t companies bringing back workers by the busload? As I had previously pointed out with the release of the preliminary Q3 GDP estimates, in a word, subsidies. |

The Nominal GDI Problem, 2003-2019 - Click to enlarge |

The Nominal GDI Problem - Click to enlarge |

|

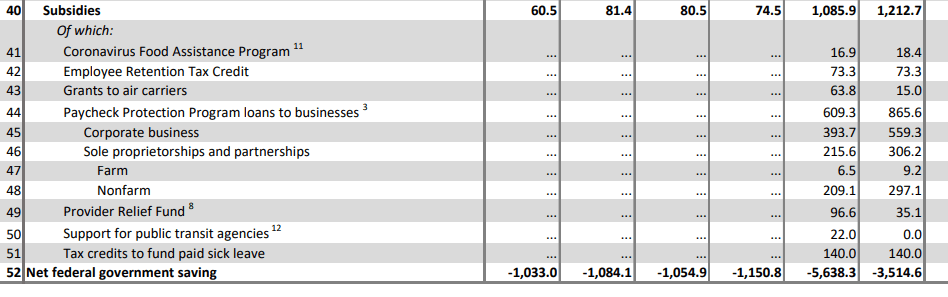

| The BEA’s updated data gives us a pretty good sense of how these have impacted specifically corporate business (and non-corporate proprietor’s firms, too, but our focus here is on corporates). The major component in the government subsidies, so far as corporate profits are concerned, has been the Paycheck Protection Program (PPP) in which the federal government initially lent hundreds of billions to companies of all sizes.

Those loans have been categorized instead as subsidies, because that’s really what they are. So long as any business uses the funds as the government intends, not reducing payrolls, as the name implies, these loans will convert into grants, meaning for GDI purposes they aren’t treated as corporate loans but, again, corporate subsidies. Very profitable ones. |

. |

| The numbers are, as expected, massive:

The figures shown above are seasonally-adjusted annual rates, but still the contributions so far as corporate profits (and proprietor’s profits) are concerned are unlike anything ever seen before. You can’t really subtract the amount of the PPP subsidy paid to corporate business shown above ($559.3 billion) from the GDP estimate of corporate profits, but if you did just to get another back-of-the-envelope sense of where things stand it would reduce economic profits down to somewhere probably less than what was figured for Q1 2020. Q1 had already put Corporate America in a huge hole. And it only gets worse from there; if you use profit estimates taken before taxes, cuts to which have also increased bottom lines, while also including IVA and CCadj, even with these massive subsidies the estimated aggregate for Q3 was barely equal to what it had been in Q4 last year. |

Case Study in Missing Growth & Profits, 1949-2019 - Click to enlarge |

Case Study in Missing Growth & Profits, 2000-2020 . |

|

Thus, no wonder businesses are in no mood to hire more…because there’s not any more work (revenue potential) that needs getting done. Instead, corporate profits, like the economic rebound represented by GDP and GDI, are hugely inflated and artificial. As I wrote at the end of October when first breaking down the impact of these subsidies:

|

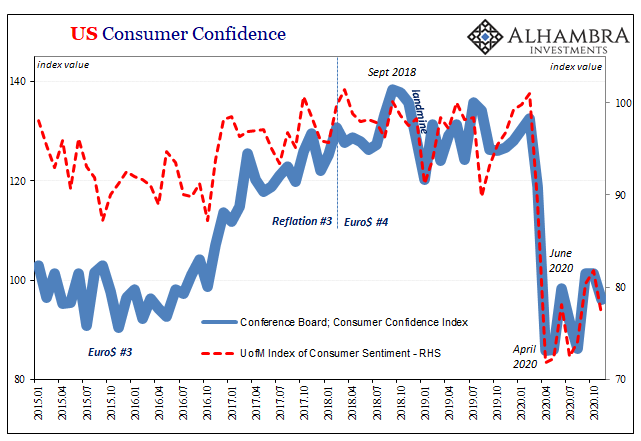

US Consumer Confidence, 2015-2020 - Click to enlarge |

| It’s instead the very obvious symptom of a deeply troubled underlying state.

And that’s why government “stimulus” doesn’t really stimulate. It has, however, in this specific case, actually saved jobs. But, and here’s the thing, many people are working at what they realize aren’t real jobs any longer so much as the creation of zombie labor beneficiaries of artificial and inflated PPP corporate windfalls. There isn’t more work, or even a return of work, for these workers to do, so, despite still being paid, they have to realize the company they work for (on average) continues to fundamentally struggle because the economic rebound doesn’t match the size of the GDP estimates. Even this significant slice of the workforce, therefore, must be cautious knowing just how precarious their own position must be – on top of the signals corporate (and proprietor’s) businesses are sending with their own quite rational caution about sustained reluctance to expand payroll levels and employment overall. These are all things connected to a lack of economic recovery. |

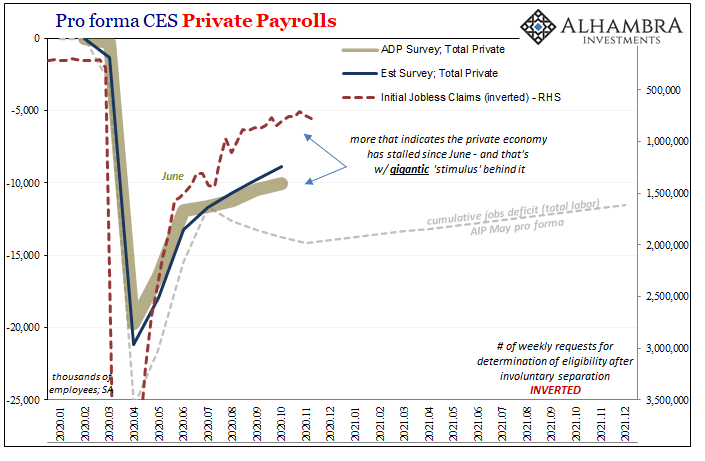

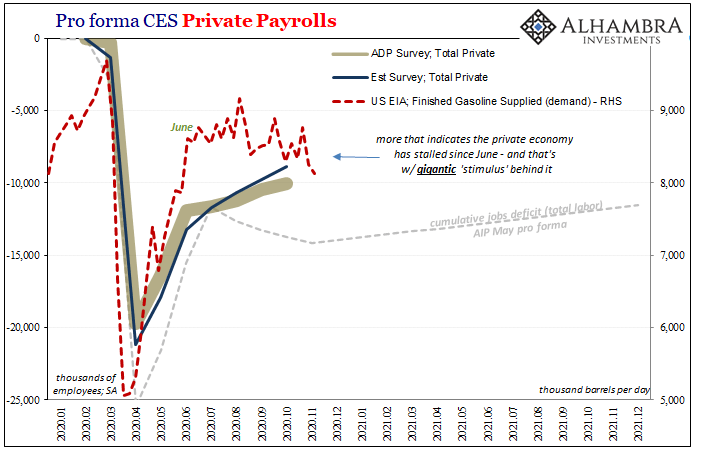

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

| And that’s why “stimulus” not only doesn’t stimulate, it’s once again “the only game in town.” If only actual, genuine, legitimate economic growth was. |

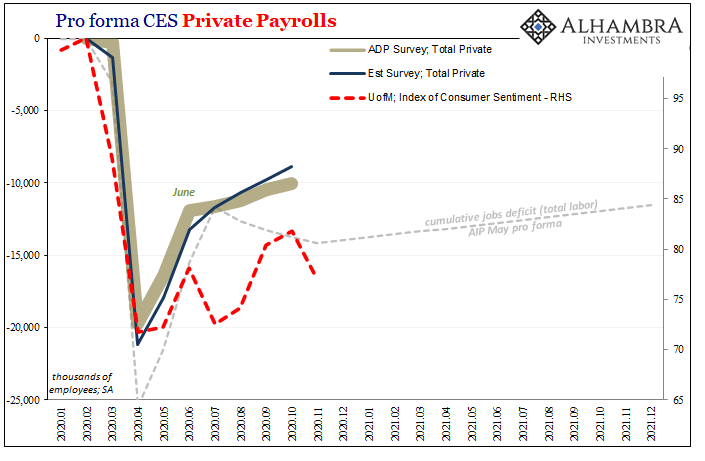

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

You Might Also Like

*These* Are The Real Huge Jobs Numbers, And They Will Make Your Blood Run Cold

*These* Are The Real Huge Jobs Numbers, And They Will Make Your Blood Run Cold

2020-08-24

There is simply no way to spin these figures as anything good. Not just the usual ones were talking about here, but more so some new data that you probably haven’t seen before. Beginning with the regular, it doesn’t matter that the level of initial jobless claims has declined substantially over the past few weeks

Reality Beckons: Even Bigger Payroll Gains, Much Less Fuss Over Them

Reality Beckons: Even Bigger Payroll Gains, Much Less Fuss Over Them

2020-07-05

What a difference a month makes. The euphoria clearly fading even as the positive numbers grow bigger still. The era of gigantic pluses is only reaching its prime, which might seem a touch pessimistic given the context. In terms of employment and the labor market, reaction to the Current Employment Situation (CES) report seems to indicate widespread recognition of this situation. And that means how there are actually two labor markets at the moment.

Purchasing Managers Indigestion

Purchasing Managers Indigestion

2020-08-06

There’s already doubt given how the two major series supposedly measuring the same thing seemingly can’t agree. If the rebound was truly robust, it would show up unambiguously everywhere. But IHS Markit’s purchasing managers indices struggled to get back above 50 in July, barely getting there, suggesting the economy might be slowing or even stalling way too close to the bottom.

Don’t Really Need ‘Em, Few More Nails Anyway

Don’t Really Need ‘Em, Few More Nails Anyway

2020-12-06

The ISM’s Non-manufacturing PMI continued to decelerate from its high registered all the way back in July 2020. In that month, the headline index reached 58.1, the best since early 2019, and for many signaling that everything was coming up “V.”

A Second Against Consumer Credit And Interest ‘Stimulus’

A Second Against Consumer Credit And Interest ‘Stimulus’

2020-06-10

Credit card use entails a degree of risk appreciated at the most basic level. Americans had certainly become more comfortable with debt in all its forms over the many decades since the Great Depression, but the regular employment of revolving credit was perhaps the apex of this transformation. Does any commercial package on TV today not include one or more credit card offers? It certainly remains a staple of junk mail.

The (Other) Shoe Of Unemployment

The (Other) Shoe Of Unemployment

2020-07-25

After raising the specter of a rebound stall, the idea before limited to Japan and Germany was abruptly given further weight today by US jobless claims numbers. For the first time since the peak at the end of March, the weekly tally of initial filings increased from the prior week.

It Just Isn’t Enough

It Just Isn’t Enough

2020-10-10

The Department of Labor attached a technical note to its weekly report on unemployment claims. The state of California has announced that it is suspending the processing of initial claims filed by (former) workers in that state.

Good Payrolls Still Say Slowdown

Good Payrolls Still Say Slowdown

2020-11-09

The payroll report for the month of October 2020 was a very good one. This shouldn’t be surprising, perfect BLS publications appear with regularity even during the most challenging of circumstances. Headlines and underneath, everything looked fine last month.

Tags: CARES Act,corporate profits,currencies,economy,employment,Featured,Federal Reserve/Monetary Policy,gdi,GDP,jobless claims,Labor Market,Markets,newsletter,paycheck protection program,U.S. ISM Manufacturing PMI,Unemployment