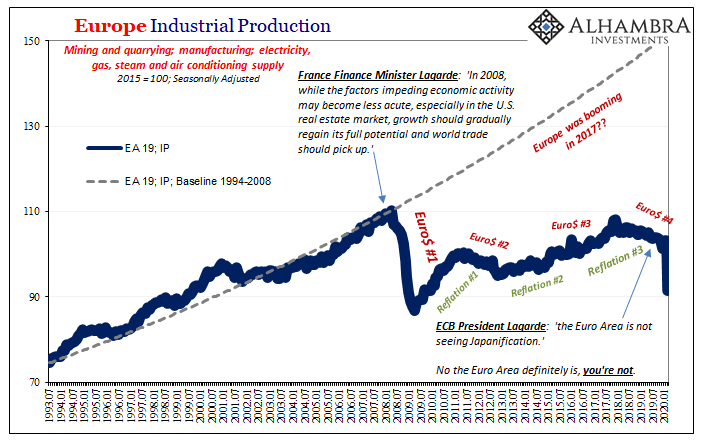

The monetary mouse. After years of Mario Draghi claiming everything under the sun available with the help of QE and the like, Christine Lagarde came in to the job talking a much different approach. Suddenly, chastened, Europe’s central bank needed assistance. So much for “do whatever it takes.” They did it – and it didn’t take. Lagarde’s outreach was simply an act of admitting reality. Having forecast an undercurrent of worldwide inflationary breakout (how “globally synchronized growth” does seem like ancient history), the two years leading up to 2020 weren’t supposed to have been this way. Draghi ended 2018 by ending his QE ignoring how growth had turned around, only to turnaround himself in 2019, like Jay Powell did on US policy rates, to restart it all over

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, Christine Lagarde, currencies, ECB, economy, Europe, Eurozone Industrial Production, Featured, Federal Reserve/Monetary Policy, France, Germany, industrial production, Italy, Mario Draghi, Markets, newsletter, NIRP, QE

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

The monetary mouse. After years of Mario Draghi claiming everything under the sun available with the help of QE and the like, Christine Lagarde came in to the job talking a much different approach. Suddenly, chastened, Europe’s central bank needed assistance. So much for “do whatever it takes.” They did it – and it didn’t take. Lagarde’s outreach was simply an act of admitting reality. Having forecast an undercurrent of worldwide inflationary breakout (how “globally synchronized growth” does seem like ancient history), the two years leading up to 2020 weren’t supposed to have been this way. Draghi ended 2018 by ending his QE ignoring how growth had turned around, only to turnaround himself in 2019, like Jay Powell did on US policy rates, to restart it all over again last fall. Europe merely out in front of the globally synchronized downturn parade, the American economy located near the rear of it. In her first major address as ECB President, last November Christine mouthed the words “much lower than previously forecast” with regard to Europe’s condition as well as its forward outlook. If only fiscal authorities would pitch in with reckless spending so as to reverse the direction, to “achieve this goal faster and with fewer side effects.” So QE wasn’t the panacea. Central bankers liked to voice such things as disclaimers before proceeding to describe all the ways QE would definitely guaranteed certainly create conditions attributable to one. Monetary policy, Draghi or Powell would say, wasn’t by itself an effective cure but it would absolutely be effective at curing. |

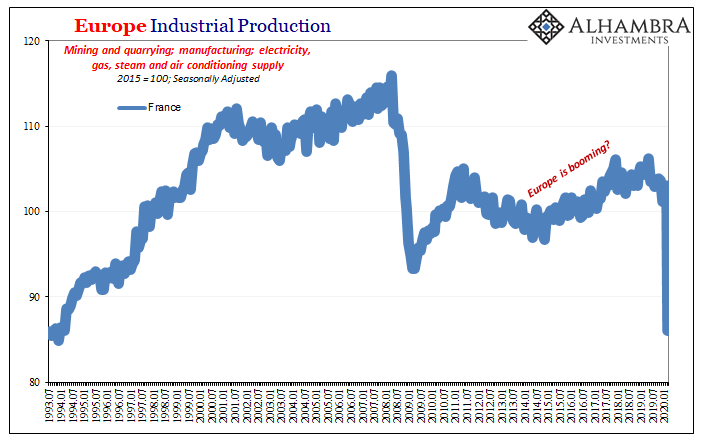

Europe Industrial Production, 1991-2020 - Click to enlarge |

| Nowadays, even the Germans are itching to be fiscally reckless.

It may be too late (as if fiscal “stimulus” is any different from the monetary puppet show). That’s the dirty little secret in all of this, especially 2017’s boom which bordered on criminal conspiracy and outright fraud. Here, see for yourself just what I mean:We’ll start with Italy because…there are hardly any words to describe this. When Italy like the rest of the world got caught up in the early 90’s recession, statistics say that Italian industry bottomed out at an equivalent index value of 104.6. At the lowest point way, way back a quarter-century ago. Taking near a decade and a half to hit 133 in the summer of 2007, following 2008’s “stimulus”-filled plunge Italian IP rebounded to a 2011 peak of just 112. By 2014, it was back down to the 2008 lows less than where output had been at the bottom of 1993. Then came Europe’s big “boom”, which got Italy (and the rest of Europe, and it doesn’t matter which stat you use, GDP works out generally the same way) back to all of 110; less than 2011, a lot less than 2007. |

Europe Industrial Production, 1993-2020 - Click to enlarge |

| After sliding for two years before COVID-19, the Italians got the worst of the shutdown in March. According to the latest Eurostat estimates, IP collapsed two months ago down by more than 28% year-over-year. That’s works out to an index value just less than 75, which just so happens to be 28% below the worst of the early nineties; a whole third less than the lowest point of the last three decades.

t’s probably been three generations since industrial output in Italy was this bad. Shutdown, sure, but that’s not the whole story. You can’t close off a wounded economy like this and expect it to immediately come right back. That’s the point here – Italy, like the rest of Europe save Germany still hasn’t come back from 2012 nor 2008! And now, this. |

Europe Industrial Production, 1993-2020 - Click to enlarge |

Lest anyone think this one problem child the lone exception to an otherwise really booming Europe before last year, Italy was merely the worst of the bunch all in the same rotten basket.

That’s why, long before COVID-19, Christine Lagarde was begging for a fiscal coordination. QE hadn’t made a dent in what had become a decade-long economic deficit, and then 2018 (Euro$ #4) turned 2017’s small upturn into yet another downturn despite Draghi’s ongoing “stimulus.” NIRP and all sorts of bond purchases, none of it relevant to the actual European economy. Keep that in mind right now and going forward.

The global economy doesn’t care about the ECB (nor any central bank).

We knew the data was going to be bad but it keeps surprising to the downside. This all matters because a weakened system before getting knocked out doesn’t just get right back up; it’s difficult enough for a healthy body to pick itself up off the mat after being KO’ed. Lagarde’s stimulus panic back in November a reality check for not just Europe and long before the world ever got this sick.

In other words, even the “V” everyone hopes shows up over the coming months probably doesn’t qualify under reasonable standards and definitions. Forget the more likely “L” for a minute, just getting back to 2018 it might take a miracle and another decade! Unfortunately, miracles aren’t exactly shovel-ready.

Sorry, Christine. Monetary policy doesn’t come with a money-back guarantee. It doesn’t have any money in it.

You Might Also Like

Lagarde Channels Past Self As To Japan Going Global

Lagarde Channels Past Self As To Japan Going Global

As France’s Finance Minister, Christine Lagarde objected strenuously to Ben Bernanke’s second act. Hinted at in August 2010, QE2 was finally unleashed in November to global condemnation. Where “trade wars” fill media pages today, “currency wars” did back then. The Americans were undertaking beggar-thy-neighbor policies to unfairly weaken the dollar.

European Data: Much More In Store For Number Four

European Data: Much More In Store For Number Four

It’s just Germany. It’s just industry. The excuses pile up as long as the downturn. Over across the Atlantic the situation has only now become truly serious. The European part of this globally synchronized downturn is already two years long and just recently is it becoming too much for the catcalls to ignore. Central bankers are trying their best to, obviously, but the numbers just aren’t stacking up their way.

Germany, Maybe Europe: No Signs Of The Bottom

Germany, Maybe Europe: No Signs Of The Bottom

For anyone thinking the global economy is turning around, it’s not the kind of thing you want to hear. Germany has been Ground Zero for this globally synchronized downturn. That’s where it began, meaning first showed up, all the way back at the start of 2018. Ever since, the German economy has been pulling Europe down into the economic abyss along with it, being ahead of the curve in signaling what was to come for the whole rest of the global economy.

Schaetze To That

Schaetze To That

When Mario Draghi sat down for his scheduled press conference on April 4, 2012, it was a key moment and he knew it. The ECB had finished up the second of its “massive” LTRO auctions only weeks before. Draghi was still relatively new to the job, having taken over for Jean-Claude Trichet the prior November amidst substantial turmoil.

As the Data Comes In, 2019 Really Did End Badly

As the Data Comes In, 2019 Really Did End Badly

The coronavirus began during December, but in its early stages no one knew a thing about it. It wasn’t until January 1 that health authorities in China closed the Huanan Seafood Wholesale Market after initially determining some wild animals sold there might have been the source of a pneumonia-like outbreak. On January 5, the Wuhan Municipal Health Commission issued a statement saying it wasn’t SARS or MERS, and that the spreading disease would be probed.

The Greenspan Bell

The Greenspan Bell

What set me off down the rabbit hole trying to chase modern money’s proliferation of products originally was the distinct lack of curiosity on the subject. This was the nineties, after all, where economic growth grew on trees. Reportedly. Why on Earth would anyone purposefully go looking for the tiniest cracks in the dam?

European Economy: A Time Recession

European Economy: A Time Recession

Eurostat confirmed earlier today that Europe has so far avoided recession. At least, it hasn’t experienced what Economists call a cyclical peak. During the third quarter of 2019, Real GDP expanded by a thoroughly unimpressive +0.235% (Q/Q). This was a slight acceleration from a revised +0.185% the quarter before.

You Will Never Bring It Back Up If You Have No Idea Why It Falls Down And Stays Down

You Will Never Bring It Back Up If You Have No Idea Why It Falls Down And Stays Down

It wasn’t actually Keynes who coined the term “pump priming”, though he became famous largely for advocating for it. Instead, it was Herbert Hoover, of all people, who began using it to describe (or try to) his Reconstruction Finance Corporation. Hardly the do-nothing Roosevelt accused Hoover of being, as President, FDR’s predecessor was the most aggressive in American history to that point, economically speaking.

Tags: Christine Lagarde,currencies,ECB,economy,Europe,Eurozone Industrial Production,Featured,Federal Reserve/Monetary Policy,France,Germany,industrial production,Italy,Mario Draghi,Markets,newsletter,nirp,QE