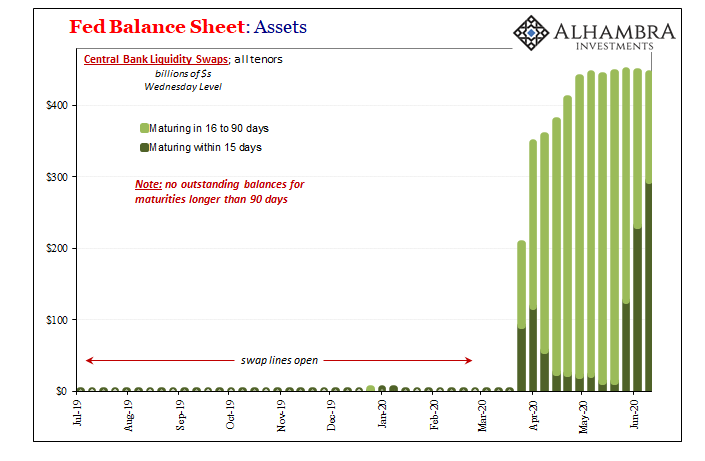

Just a quick update to add a little more data and color to my last Friday’s swap line criticism so hopefully you can better see how there is intentional activity behind them. Since a few people have asked, I’ll break them out with a little more detail. While the volume of swaps outstanding at the Fed has, in total, remained relatively constant (suspiciously, if you ask me), the underlying tenor of them has not. Meaning, there is purpose. It’s not like everyone panicked in March, signed up for longer swap trades, and are now letting them just roll off as everything has gone back to normal (as is alleged). Fed Balance Sheet: Assets, 2007-2020 - Click to enlarge Foreign central banks (remember, the overseas institution initiates the transaction likely on

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, central bank liquidity swaps, currencies, dollar flood, economy, eurodollar system, Featured, Federal Reserve/Monetary Policy, jay powell, Liquidity, Markets, newsletter, overseas dollar swaps

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

Just a quick update to add a little more data and color to my last Friday’s swap line criticism so hopefully you can better see how there is intentional activity behind them. Since a few people have asked, I’ll break them out with a little more detail. While the volume of swaps outstanding at the Fed has, in total, remained relatively constant (suspiciously, if you ask me), the underlying tenor of them has not. Meaning, there is purpose. It’s not like everyone panicked in March, signed up for longer swap trades, and are now letting them just roll off as everything has gone back to normal (as is alleged). |

Fed Balance Sheet: Assets, 2007-2020 - Click to enlarge |

| Foreign central banks (remember, the overseas institution initiates the transaction likely on behalf of perceived or real demand of banks operating within its jurisdiction – including, as I pointed out, foreign subsidiaries of US banks) have instead kept up the volume, but as longer-dated arrangements have been expiring these have been actively renewed and shifted to shorter duration transactions. |

Fed Balance Sheet: Assets, 2019-2020 - Click to enlarge |

The question is, why haven’t they disappeared altogether? If March had been a one-off, June is a long way off to show so much volume still taking this circuitous route.

|

. |

| Has the Fed morphed back into a quasi-real bills state, or is the “temporary” market disruption of March and April maybe not nearly so temporary? And, thinking along these lines, that “flood” maybe didn’t work at least so far as getting things back closer to normal.

If QE really had unleashed a flood, these things should’ve zeroed out by now. As the longer duration trades come up for maturity, those made under panic of March and early April, the initiating agent (central bank) would’ve just let them expire with local banks flush with Jay Powell’s “money printing.” Instead, they are clearly, purposefully, and actively being replaced week by week for practically the same net volume just lesser maturities. Again, why? If only someone would have the guts to ask Jay Powell directly. But that might spoil some or all of his 60 minutes. Which is it: |

|

You Might Also Like

COT Black: No Love For Super-Secret Models

COT Black: No Love For Super-Secret Models

As I’ve said, it is a threefold failure of statistical models. The first being those which showed the economy was in good to great shape at the start of this thing. Widely used and even more widely cited, thanks to Jay Powell and his 2019 rate cuts plus “repo” operations the calculations suggested the system was robust.

So Much Bond Bull

So Much Bond Bull

Count me among the bond vigilantes. On the issue of supply I yield (pun intended) to no one. The US government is the brokest entity humanity has ever conceived – and that was before March 2020. There will be a time, if nothing is done, where this will matter a great deal.That time isn’t today nor is it tomorrow or anytime soon because it’s the demand side which is so confusing and misdirected.

So Much Dollar Bull

So Much Dollar Bull

According to the Federal Reserve’s calculations, the US dollar in Q1 pulled off its best quarter in more than twenty years – though it really didn’t need the full quarter to do it. The last time the Fed’s trade-weighed dollar index managed to appreciate farther than the 7.1% it had in the first three months of 2020, the year was 1997 during its final quarter when almost the whole of Asia was just about to get clobbered.In second place (now third) for the dollar’s best, Q4 2008.

Don’t Forget (Business) Credit

Don’t Forget (Business) Credit

Rolling over in credit stats, particularly business debt, is never a good thing for an economy. As noted yesterday, in Europe it’s not definite yet but sure is pronounced. The pattern is pretty clear even if we don’t ultimately know how it will play out from here. The process of reversing is at least already happening and so we are left to hope that there is some powerful enough positive force (a real force rather than imaginary, therefore disqualifying the ECB) to counteract the negative tendencies in order to set them straight before it becomes too late.

A Day For Rate Cuts

A Day For Rate Cuts

Well, that wasn’t he had in mind. The whole point of a rate cut, any rate cut let alone an emergency fifty, is to signal especially the stock market that the Fed is in the business of…something. The public has been led, by and large, to assume that something good happens when the Fed Chair shows up on TV.

The Global Engine Is Still Leaking

The Global Engine Is Still Leaking

An internal combustion engine that is leaking oil presents a difficult dilemma. In most cases, the leak itself is obscured if not completely hidden. You can only tell that there’s a problem because of secondary signs and observations.If you find dark stains underneath your car, for example, or if your engine smells of thick, bitter unpleasantness, you’d be wise to consider the possibility.

Why The FOMC Just Embraced The Stock Bubble (and anything else remotely sounding inflationary)

Why The FOMC Just Embraced The Stock Bubble (and anything else remotely sounding inflationary)

The job, as Jay Powell currently sees it, means building up the S&P 500 as sky high as it can go. The FOMC used to pay lip service to valuations, but now everything is different. He’ll signal to all those fund managers by QE raising bank reserves, leading them on in what they all want to believe is “money printing” (that isn’t).

This Thing Is Only Getting Started; Or, *All* The V’s Are Light On The Right

This Thing Is Only Getting Started; Or, *All* The V’s Are Light On The Right

The Federal Reserve’s models really are the most optimistic of the bunch. With the policy meeting conducted today, no surprises as far as policies go, we now know what ferbus has to say about everything that’s happened this year. Skipping the usual March projections, what with the FOMC totally occupied at the time by a complete global monetary meltdown Jay Powell now says “we saw it coming”, the central bank staff released the calculations performed by its DSGE prodigy concurrent with today’s policy meeting.

Tags: central bank liquidity swaps,currencies,dollar flood,economy,eurodollar system,Featured,Federal Reserve/Monetary Policy,jay powell,Liquidity,Markets,newsletter,overseas dollar swaps