[This article is part of the Understanding Money Mechanics series, by Robert P. Murphy. The series will be published as a book in late 2020.] In chapter 8 we presented Ludwig von Mises’s explanation of how bank credit expansion causes the boom-bust cycle, what is now known as Austrian business cycle theory. However, the reigning view today in both academia and the popular media is the Keynesian explanation, derived from John Maynard Keynes’s famous 1936 book The General Theory. In contrast to the Austrians, Keynes viewed depressions as something that could naturally plague market economies when total spending (“aggregate demand”) was insufficient to support full employment. Keynes argued that markets didn’t possess a self-correcting mechanism and that left to

Topics:

Robert P. Murphy considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

[This article is part of the Understanding Money Mechanics series, by Robert P. Murphy. The series will be published as a book in late 2020.]

In chapter 8 we presented Ludwig von Mises’s explanation of how bank credit expansion causes the boom-bust cycle, what is now known as Austrian business cycle theory. However, the reigning view today in both academia and the popular media is the Keynesian explanation, derived from John Maynard Keynes’s famous 1936 book The General Theory.

In contrast to the Austrians, Keynes viewed depressions as something that could naturally plague market economies when total spending (“aggregate demand”) was insufficient to support full employment. Keynes argued that markets didn’t possess a self-correcting mechanism and that left to their own devices, markets could be mired in depression for years on end. Only with wise oversight by central banks and government officials could we hope to achieve steady economic growth.

This chapter will summarize the Keynesian view and then challenge it from an Austrian perspective.

The Rhetorical Framing of The General Theory

It would be difficult to overstate the extent to which the Keynesian approach has permeated modern society. Although Keynes wasn’t the first to blame business downturns on a lack of spending, his 1936 book—released in the midst of an unending global depression—appeared to offer a sophisticated diagnosis of the problem, and furthermore seemed to explain why the traditional economic remedies had failed.

The very title of the book reflects Keynes’s clever rhetorical framing and helps us nowadays to understand why this book captivated so many of its readers. Keynes himself explains it well in the (very brief) first chapter of the book:

I have called this book the General Theory of Employment, Interest and Money, placing the emphasis on the prefix general. The object of such a title is to contrast the character of my arguments and conclusions with those of the classical theory of the subject, upon which I was brought up and which dominates the economic thought, both practical and theoretical, of the governing and academic classes of this generation, as it has for a hundred years past. I shall argue that the postulates of the classical theory are applicable to a special case only and not to the general case, the situation which it assumes being a limiting point of the possible positions of equilibrium. Moreover, the characteristics of the special case assumed by the classical theory happen not to be those of the economic society in which we actually live, with the result that its teaching is misleading and disastrous if we attempt to apply it to the facts of experience. (Keynes 1936,1 p. 11, bold added)

It would have been presumptuous and provoked defensiveness for Keynes to argue that his predecessors were complete buffoons and totally wrong. Instead, as the introductory chapter explains, Keynes argued that their “classical” approach was correct under certain conditions (namely, when the economy is at full employment) but that in general those conditions might not be fulfilled. In that case—such as the world faced in 1936—Keynes proposed a more general theory that could handle all possible scenarios.

Thus, Keynes was proposing to do for economics what Albert Einstein had done for physics: Einstein’s theory of relativity didn’t say that the classical mechanics of Isaac Newton were totally wrong. Instead, Einstein proposed equations that described the behavior of matter and energy under more general circumstances. Then, in the special case when the objects moved at only a small fraction of the speed of light, Einstein’s system “reduced to” the more familiar Newtonian system. This explained to physicists why Newton’s model had initially seemed so successful but also demonstrated the superiority of Einstein’s approach.

To be sure, there are serious problems with Keynes’s rhetorical framing. For one thing, it was a misnomer to use the term “classical,” when that phrase already had a well-established meaning among economists, to refer to the doctrines based on the labor theory of value that were dominant before the so-called Marginal Revolution of the 1870s. Even more serious, Keynes was wrong to claim that his predecessors “assumed” full employment. As an obvious example, which we discussed in chapter 8, Mises developed his own theory of the business cycle in 1912—two decades before Keynes!

Despite these problems, Keynes’s rhetorical framing surely helps to explain the impact of his book. Another common explanation is that the Keynesian framework provided a seemingly scientific justification for increased government spending and intervention in markets, which was music to the ears of many academics and political officials. Ironically, Keynes himself acknowledged this affinity in the 1936 preface to the German edition when he wrote:

The theory of output as a whole, which is what the following book purports to provide, is much more easily adapted to the conditions of a totalitarian state, than is the theory of the production and distribution of a given output produced under conditions of free competition and a large measure of laissez-faire. (Keynes 1936, p. 6)

The Paradox of Thrift

Perhaps the quickest way to illustrate the divide between Keynesian and “orthodox” economics is the so-called paradox of thrift. According to conventional wisdom as well as a straightforward application of economic principles, when the community saves more, this allows for more investment spending, and is thereby the path to growing productivity and rising living standards. Yet as Keynes explained in the 1939 preface to the French edition of his book:

Quite legitimately we regard an individual’s income as independent of what he himself consumes and invests. But this, I have to point out, should not have led us to overlook the fact that the demand arising out of the consumption and investment of one individual is the source of the incomes of other individuals, so that incomes in general are not independent, quite the contrary, of the disposition of individuals to spend and invest….It is shown that, generally speaking, the actual level of output and employment depends, not on the capacity to produce or on the pre-existing level of incomes, but on the current decisions to produce which depend in turn on current decisions to invest and on present expectations of current and prospective consumption. Moreover, as soon as we know the propensity to consume and to save…we can calculate what level of incomes, and therefore what level of output and employment, is in profit-equilibrium with a given level of new investment; out of which develops the doctrine of the Multiplier. Or again, it becomes evident that an increased propensity to save will ceteris paribus contract incomes and output; whilst an increased inducement to invest will expand them. (Keynes 1936, p. 9, bold added)

The above excerpt is a good distillation of the entire enterprise of The General Theory. Rather than viewing the economy from the perspective of an individual household or firm—where we start each time period with a particular level of income out of which consumption and investment are financed—Keynes reversed causality. Individual and business decisions to consume or invest, driven by psychological considerations, determine the level of income in the community.

Under the “paradox of thrift,” when hard times hit, the seemingly rational thing for households and businesses is to tighten their belts and eliminate superfluous spending. But from a Keynesian perspective, this leads to disaster, as the drop in spending only further reduces the income in the economy. This is why government budget deficits—a form of negative saving—are called for, as they can more than pay for themselves through the “multiplier.”

Even though the economic models and arguments have been refined over the decades, this basic Keynesian attitude survives to this day. The hostility to saving is apparent in the writings of economists like Paul Krugman, but also among central bankers such as Ben Bernanke, who justified his unprecedented actions as Fed chair by reference to the dread of “deflation” (by which he meant falling prices). And the popular press toes the Keynesian line as well: amid the COVID-19 crisis, a CNN headline declared, “New threat to the economy: Americans are saving like it’s the 1980s.”2

The Keynesian Understanding of the Great Depression

According to Keynes, the persistence of the Great Depression showed the failure of “classical” economic doctrines and policies. If the market economy had a self-corrective mechanism, why had the world been mired in high unemployment for years on end?

According to Keynes, his orthodox colleagues were unable to explain persistent unemployment. As he argues in chapter 2, the orthodox school had to believe that if unemployment were excessively high, then market forces would eventually bring down the wage rate, at least as measured in “real” terms (i.e., adjusted for price inflation). The falling (real) wage rate would reduce the number of people looking for work, and it would increase the amount of workers that employers wanted to hire. Thus, any “glut” in the labor market should be quickly eliminated according to the orthodox economists.

Keynes pointed out two flaws with this argument. First, it simply didn’t fit the facts: workers strongly resisted cuts in the actual money wages they received, but they didn’t respond the same way if their “real” wages fell because of a general increase in prices. Therefore, Keynes argued, the orthodox explanation—in which workers rationally supplied labor hours according to the height of the real wage—was simply not true. (This real-world behavior on the part of workers is sometimes explained as “money illusion.”)

Second, Keynes argued that even if the workers collectively wanted to reduce their (real) wage demands, they might be powerless to do so, for if workers agreed to even a significant pay cut—measured in nominal, actual money terms—the lowered costs of production would then lead firms to reduce the prices they charged for their products, meaning that in real terms the wage rate wouldn’t have fallen so much after all.

Thus Keynes thought it was obvious that something external to the labor market caused the massive increase in unemployment during the Great Depression years. Any attempt to fit the facts of the 1930s into the orthodox framework would seem contrived. As he wryly observed, “Labour is not more truculent in the depression than in the boom—far from it. Nor is its physical productivity less. These facts from experience are a prima facie ground for questioning the adequacy of the classical analysis” (Keynes 1936, p. 14).

Photo from the Franklin D. Roosevelt Presidential Library and Museum

In this context, Keynes argued that government budget deficits could provide relief. (We are here omitting his more complex discussion on interest rates.) To drive home his shocking perspective, Keynes actually argued:

If the Treasury were to fill old bottles with banknotes, bury them at suitable depths in disused coalmines which are then filled up to the surface with town rubbish, and leave it to private enterprise on well-tried principles of laissez-faire to dig the notes up again…there need be no more unemployment and, with the help of the repercussions, the real income of the community, and its capital wealth also, would probably become a good deal greater than it actually is. It would, indeed, be more sensible to build houses and the like; but if there are political and practical difficulties in the way of this, the above would be better than nothing. (Keynes 1936, p. 68)

Needless to say, in the orthodox approach, diverting labor power into burying money and then digging it up again is hardly the way to help a distressed economy.

The Austrian Critique of Keynesianism

There are entire books (cited in the endnotes3) devoted to the refutation of Keynesian theory and its treatment of the Great Depression, so our discussion here will be brief.

On theoretical grounds, the Austrians provide a much more satisfactory explanation of the business cycle, as laid out in chapter 8. Contrary to Keynes, workers aren’t as productive when the boom collapses into a bust, at least not when we take into account the overall structure of production.

To use an exaggerated illustration: if during the boom period the economy produced nothing but hammers and no new nails, eventually a crisis would emerge. Even though carpenters would possess the same skills, their physical productivity would clearly plummet once the last nail in inventory had been used. A massive drop in “real output” would be necessary at that point, while the economy retooled (literally). No amount of deficit spending or money printing could paper over such basic material facts. The fact that the Austrian approach accords with common sense is evidence in its favor, and the amusing reductio ad absurdum that Keynes himself invented for his own theory should be a strike against it.

Empirically, we note that during the 1930s, governments and central banks around the world engaged in the most Keynesian policies in history to that date. In the United States, for example, the Hoover administration—despite disinformation to the contrary—cajoled big business to prop up wage rates and ran unprecedented peacetime budget deficits.4 For its part, the Federal Reserve in the early 1930s expanded the monetary base and slashed interest rates to then record lows.

Now, to be sure, modern-day Keynesians acknowledge these awkward facts as “too little, too late.” But even so, their admission raises the obvious question: If the fundamental Keynesian explanation for the Great Depression is that governments were too timid when it came to deficit spending, then why didn’t the Great Depression happen earlier, when everybody admits that governments did even less during financial panics?

No, a much more sensible explanation of the historical record is staring us in the face: the depressions (or “panics”) of the nineteenth and early twentieth centuries played out according to the theory developed by Ludwig von Mises. Yet during those crises, governments largely remained aloof, and that’s why the economy recovered. In contrast, it wasn’t until government and central bank officials became serious about helping with “countercyclical” policies in the 1930s that an initial crash blossomed into a Depression that wouldn’t go away.

- 1. In this chapter, references to The General Theory use the pagination contained in this (free) online version of the book: John Maynard Keynes, The General Theory of Employment, Interest, and Money (1936; ETH Zurich International Relations and Security Network, n.d.), https://www.files.ethz.ch/isn/125515/1366_KeynesTheoryofEmployment.pdf.

- 2. See Matt Egan, “New Threat to the Economy: Americans Are Saving like It’s the 1930s,” CNN Business, May 12, 2020, https://www.cnn.com/2020/05/12/investing/jobs-coronavirus-consumer-spending-debt/index.html?fbclid=IwAR09Du7nf1OKE9-VpOgayFNTIDeKJisVivSlOR-rYtKoxQw9H8MwcIU49FM.

- 3. Murray N. Rothbard’s Man, Economy, and State (Princeton, NJ: D. Van Nostrand, 1962), https://mises.org/library/man-economy-and-state-power-and-market, contains a scathing critique of Keynesian thought as it stood in the early 1960s. Henry Hazlitt wrote a point-by-point critique of Keynes in his book The Failure of the “New Economics” (Princeton, NJ: D. Van Nostrand, 1959), https://mises.org/library/failure-new-economics-0. For an Austrian explanation of the Great Depression, see Murray N. Rothbard’s America’s Great Depression (Princeton, NJ: D. Van Nostrand, 1963), https://mises.org/library/americas-great-depression, and for a newer version that specifically critiques modern Keynesian arguments, see Robert P. Murphy, The Politically Incorrect Guide to the Great Depression and the New Deal (Washington, DC: Regnery Publishing, 2009).

- 4. To see the truth about the Hoover record, consult Rothbard’s America’s Great Depression, or start with the online article from Robert P. Murphy, “Did Hoover Really Slash Spending?,” Mises Daily, May 31, 2010, https://mises.org/library/did-hoover-really-slash-spending.

You Might Also Like

The Search for Yield

The Search for Yield

A no-holds-barred discussion of the economy after the coronavirus shutdown and George Floyd protests. Are we facing another Great Depression? Can there be a V-shaped recovery or is this wishful thinking? What will all the new money and credit created by Congress and the Fed mean for the dollar? What kind of economic mess will Trump or Biden inherit in 2021? How far will Fed chair Powell go to keep markets propped up?

Economic Collapse Has Turned Many Europeans against the EU

Economic Collapse Has Turned Many Europeans against the EU

Since the beginning of the year, the corona crisis has monopolized news coverage to the extent that a lot of very important stories and developments either went underreported or were ignored altogether. One such example was the very surprising ruling that came out of the German Constitutional Court in early May, which challenged the actions and remit of the European Central Bank (ECB).

Mark Packard’s Value Learning Process: The Two Kinds of Knowledge Entrepreneurs Must Have

Mark Packard’s Value Learning Process: The Two Kinds of Knowledge Entrepreneurs Must Have

Key Takeaways and Actionable Insights. Innovation is one of the keys to business success. The world is changing at such a pace, and your customers’ preferences are changing so fast, that your business has to change at the same speed, or even faster. How to keep up is a part of the entrepreneurial challenge.

The Great Society: A Lesson in American Central Planning

The Great Society: A Lesson in American Central Planning

Most people associate the Great Society initiative with Lyndon Baines Johnson. There is very good reason for that, to be sure. As president, Johnson, the “master of the Senate,” was the driving force behind the raft of legislation that passed during his administration, the 1964 and 1965 legislation that framed and filled in his vision for a “great society” in which the blessings of postwar America’s bonanza would be shared by all.

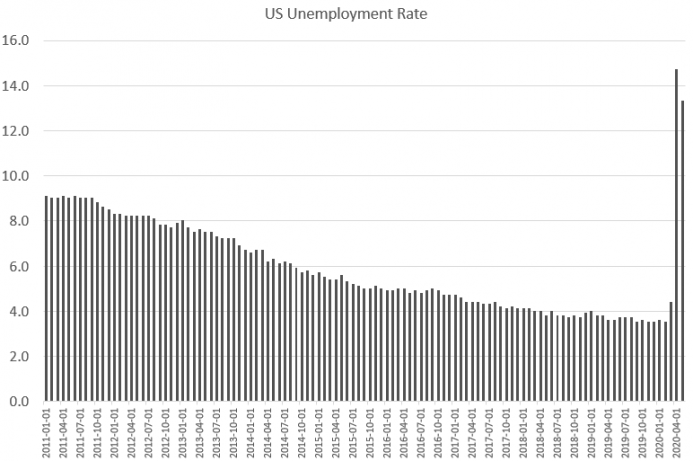

The Employment Situation Is Still a Disaster

The Employment Situation Is Still a Disaster

Last Friday, the US Bureau of Labor Statistics released new unemployment data. The report surprised many because it showed a decrease in the unemployment rate, while many observers had expected an increase.

The Scandinavian Model Won’t Work in Chile

The Scandinavian Model Won’t Work in Chile

Scandinavian welfare states continue to allure leftist onlookers across the world. The Nordic welfare model is marketed as a humane alternative to the cutthroat nature of Western capitalism. It received a massive boost when Vermont senator Bernie Sanders campaigned on emulating these countries in both of his presidential runs during 2016 and 2020.

Inequality is Overstated—and Overrated

Inequality is Overstated—and Overrated

Whining and complaining about inequality is a growth industry. Thomas Piketty’s book (or perhaps a large virtue-signaling paperweight), about how the rich are getting richer, achieved bestseller status and is now a movie. Understanding the flaws in the wealth inequality argument is increasingly important, because the communist wing of the Democratic Party is now openly advocating a wealth tax.

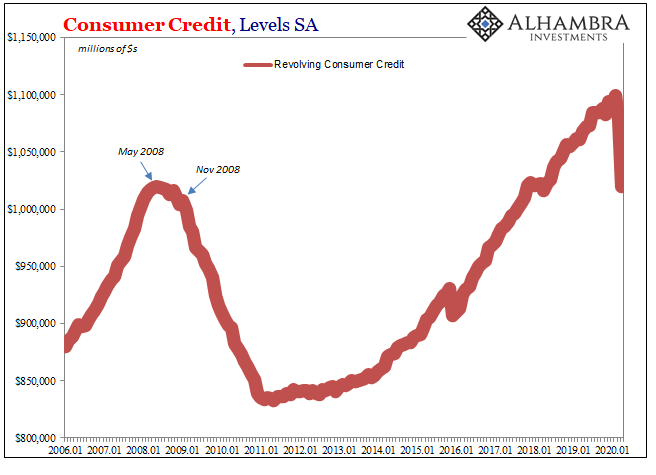

A Second Against Consumer Credit And Interest ‘Stimulus’

A Second Against Consumer Credit And Interest ‘Stimulus’

Credit card use entails a degree of risk appreciated at the most basic level. Americans had certainly become more comfortable with debt in all its forms over the many decades since the Great Depression, but the regular employment of revolving credit was perhaps the apex of this transformation. Does any commercial package on TV today not include one or more credit card offers? It certainly remains a staple of junk mail.

Tags: Featured,newsletter