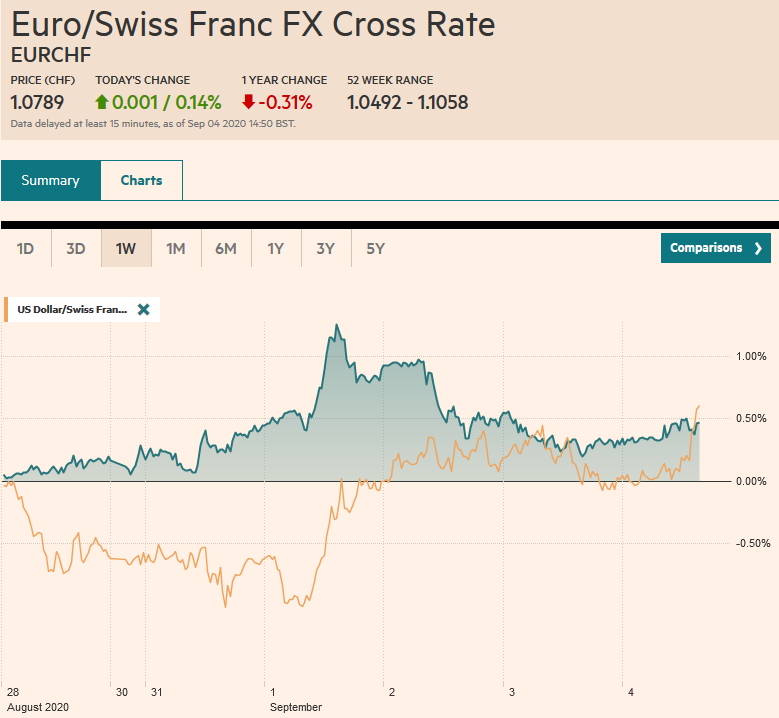

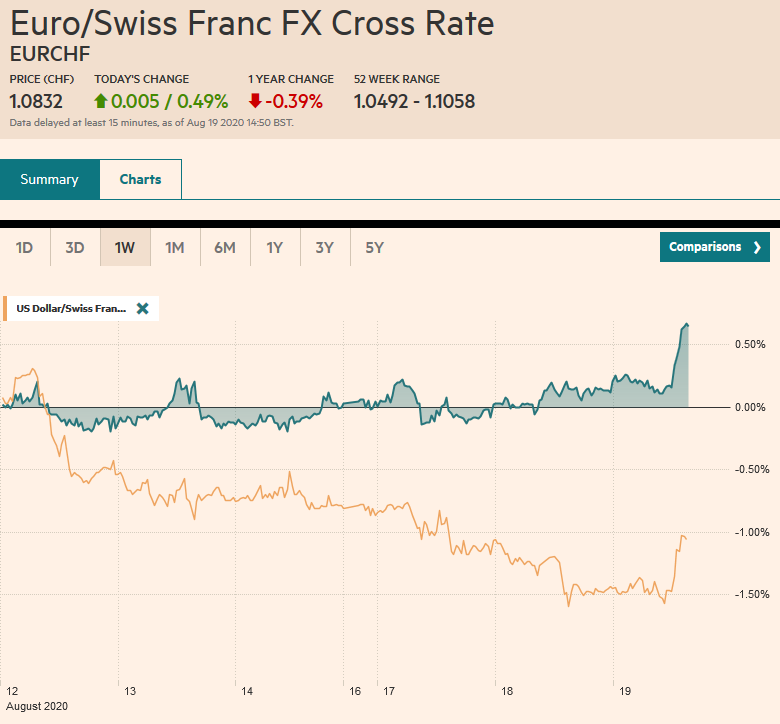

Swiss Franc The Euro has risen by 0.14% to 1.0789 EUR/CHF and USD/CHF, September 4(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The dramatic sell-off of US shares yesterday is the main focus, capturing the limelight from other forces, including today’s US employment report. It was the third-worst session for the S&P 500 since the March 23 bottom, and the other two did not see follow-through selling. Asia Pacific shares tumbled, led by Australia’s 3% plunge, while the Nikkei, Hang Seng, and Kospi fell over 1%. European bourses are firmed, recovering about a third of yesterday’s 1.4% decline. Materials, industrials, and financials are leading today’s efforts. US shares are steady to slightly firmer.

Topics:

Marc Chandler considers the following as important: 4) FX Trends, 4.) Marc to Market, China, Currency Movement, Featured, Japan, jobs, NATO, newsletter, treasuries, USD

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Swiss FrancThe Euro has risen by 0.14% to 1.0789 |

EUR/CHF and USD/CHF, September 4(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

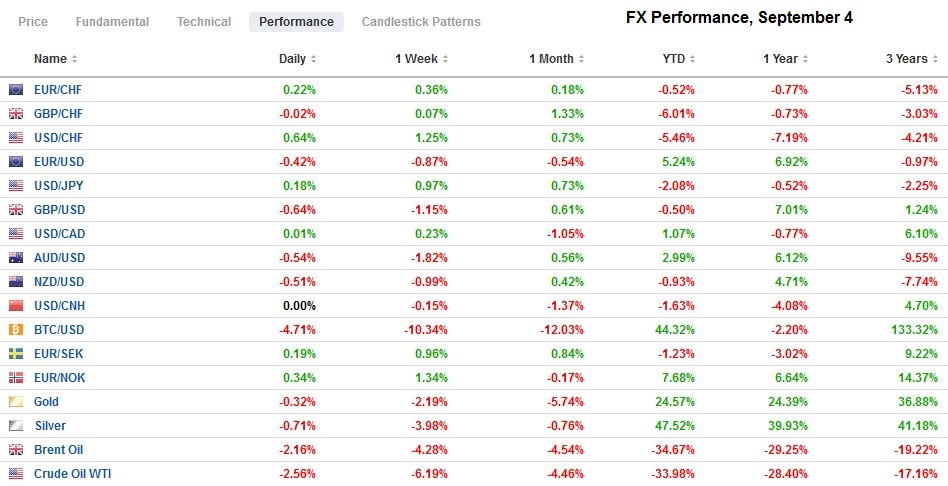

FX RatesOverview: The dramatic sell-off of US shares yesterday is the main focus, capturing the limelight from other forces, including today’s US employment report. It was the third-worst session for the S&P 500 since the March 23 bottom, and the other two did not see follow-through selling. Asia Pacific shares tumbled, led by Australia’s 3% plunge, while the Nikkei, Hang Seng, and Kospi fell over 1%. European bourses are firmed, recovering about a third of yesterday’s 1.4% decline. Materials, industrials, and financials are leading today’s efforts. US shares are steady to slightly firmer. The bond market lost a safe-haven bid, and yields are a little higher. The US benchmark is around 65 bp, down five basis points on the week. The dollar is narrowly mixed. The majors are +/- 0.25%, with the Canadian dollar and Norwegian krone on the strong side, and the Swiss franc and Swedish krona on the weak side. Emerging market currencies are also mixed, but the JP Morgan Emerging Market Currency Index is up about 0.2% to offset most of the week’s loss. Gold tumbled alongside equities yesterday and is mostly in a $1930-$1940 range today. Oil has steadied, but the October WTI contract is nursing a slightly larger than a 3% loss for the week, the most since June. |

FX Performance, September 4 - Click to enlarge |

Asia Pacific

A Chinese paper (Global Times) reports that China may reduce their Treasury holdings in response to the weaponization of the dollar market, confrontation with Trump, and fear of failure given the jump in the US debt levels. The paper suggested the Treasury holdings can fall from around $1 trillion to $800 bln. They might fall, especially if the Federal Reserve ups its bond-buying program. China may have good reasons to diversify away from US Treasuries, but its holdings during the Trump presidency have been remarkably steady. In November 2016, they stood at $1.049 trillion according to US Treasury figures. The latest estimate for July was at $1.074 trillion. Moreover, even if China were do launch a divestment campaign, why would it be telegraphed. What is done is more important than what is said.

Australian retail sales continue to fare well. They rose 3.2% in July after a 2.7% gain in June. Through the first seven months, they have averaged 2.0% gain a month. In the comparable period last year, the average was 0.2%. August will be more challenging. The 3.1% decline in Australian shares today is the largest since May. Like in the US, tech stocks lead the rout. Separately, Australia committed to re-opening the economy before the end of the year.

Polls suggest Japanese Cabinet Secretary Suga is the leading candidate to replace Abe as Prime Minister. This underscores our sense of continuity of Abenomics. Suga has indicated he will press for more BOJ liquidity provisions, which given the risk of deflation as shown in the August CPI for Toyko, maybe the direction that Governor Kuroda was moving in too.

The dollar is in less than a quarter of a yen range today above JPY106.00. Recall that last week it settled near JPY105.40 following Abe’s resignation. There is a $1.8 bln option at JPY106 that will be cut today. On the top side, there are another $2 bln in expiring options struck between JPY106.50 and JPY106.65. Below, there is a $365 mln option at JPY105.75 and another for about $480 mln at JPY105.55. After pulling back to around $0.7230 in the local session, the Australian dollar has rebounded to almost $0.7300, where it appeared to be losing some momentum. That said, above there resistance is seen in the $0.7320-$0.7340 area. Reflecting the dollar’s recovery yesterday, the PBOC set the dollar’s reference rate at CNY6.8359, a little stronger than the bank models suggested. The yuan’s advancing streak against the dollar is now six-weeks long, and it has declined in only one week here in Q3.

Europe

German factory orders in July rose 2.8% after the June series was revised to show a 28.8% jump rather than 27.9%. Still, the July increase was a little more than half of what economists projected. The source of disappointment was from domestic parties, where orders fell 10.2% after the 35.3% jump in June. Despite the consternation this week about the euro’s strength, in July, as the euro was appreciated by the most in a month for a decade, foreign orders jumped. Foreign orders rose 14.4%, following a 23.6% rise. Yet the real strength of the foreign demand was from outside the eurozone. Those orders rose an impressive 19.2% after increasing 23.8% in June.

NATO meets today, and two European issues are center stage. The first is the dispute between Greece and Turkey over what appears to be large gas finds in waters that Ankara claims. The two NATO members remain at loggerheads. Greece is a member of the EU and is supported by Brussels. The second issue is the Navalny poisoning. Some formal response is necessary, though unlike the past victims of Moscow’s actions, this one apparently took place on Russian territory, a technical distinction of diplomatic importance. The critics of the Nord Stream II gas pipeline that is to bypass Ukraine and go directly to Germany is pushing Berlin to cancel it. The US has been pressing for this for some time and has threatened sanctions on those that persist. Although some German MPS form across the political spectrum are ready to abandon the commercial project, it is not clear that there is a consensus to do so in the grand coalition. Some note that the US imports Russian oil while being critical of Europe’s gas imports, which strikes some as a commercial position for the US, not one of principle. Europe could pass its own version of the Magnitsky Act that would allow sanctions for human rights violations.

The euro recovered smartly yesterday, making new highs late in the North American session, even as equities were hammered. The euro edged above yesterdays highs to about $1.1865 by early in the European session. The market seems reluctant to do much until at least after the US jobs data. Two option strikes are relevant: The first is for about 650 mln euros at $1.1850, and the other is for about 965 mln euros at $1.1875. Note that there are nearly $3 bln in options that will be cut today struck between $1.1900 and $1.1905. There are also roughly $3 bln in options in the $1.1780-$1.1800 range. Given that long holiday weekend in the US, it would not be surprising if the market faded the initial reaction to the employment data. Sterling is trading at the lower end of yesterday’s range. It is in a little more than half a cent range above $1.3255. It met a wall of selling in near $1.3320. Sterling closed near $1.3350 last week, and there is a GBP270 mln option struck there that expires today. Its three-week advance, which matches the longest since January it at risk.

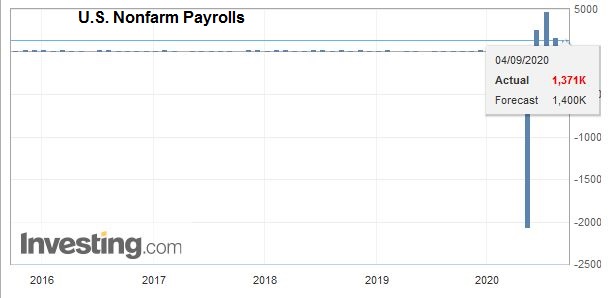

AmericaThe US employment report is front and center. The weekly jobless claims are increasingly difficult to read. In part, a new seasonal adjustment is being used, but more importantly, going forward, the benefits are increasingly going to be exhausted. This will produce lower numbers of continuing claims but will not represent an improvement in the labor market. |

U.S. Nonfarm Payrolls, August 2020(see more posts on U.S. Nonfarm Payrolls, ) Source: investing.com - Click to enlarge |

| Note that the Pandemic Unemployment Assistance Program, which extends benefits to the self-employed and gig workers, increased its rolls by 152k to 759k last week. The median forecast in the Bloomberg survey stands at 1.35 mln for today’s non-farm payrolls, down from 1.76 mln in July. |

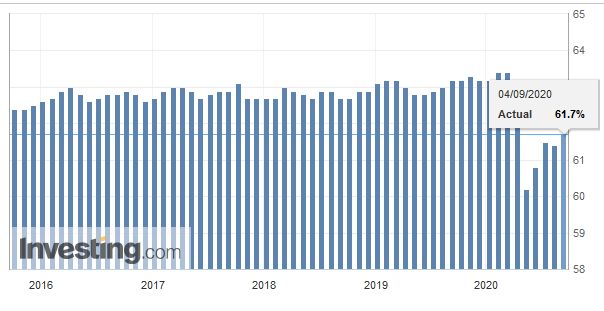

U.S. Participation Rate, August 2020(see more posts on U.S. Participation Rate, ) Source: investing.com - Click to enlarge |

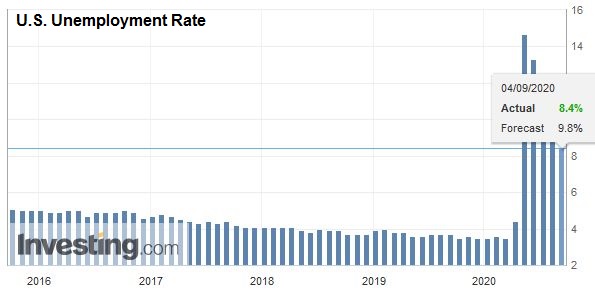

| The unemployment rate is expected to slip to 9.8%. Note that the seasonal adjustment factor was a net additive in recent months and, with today’s report, become a net drag. |

U.S. Unemployment Rate, August 2020(see more posts on U.S. Unemployment Rate, ) Source: investing.com - Click to enlarge |

| Separately, we note that Fed officials, who now have entered the quiet period ahead of the September 15-16 FOMC meeting, appeared to have increased their calls for more fiscal support. However, talks between the White House and the House of Representatives seem to have gone nowhere. That said, an agreement between Mnuchin and Pelosi seeks to avoid a government shutdown in early October. |

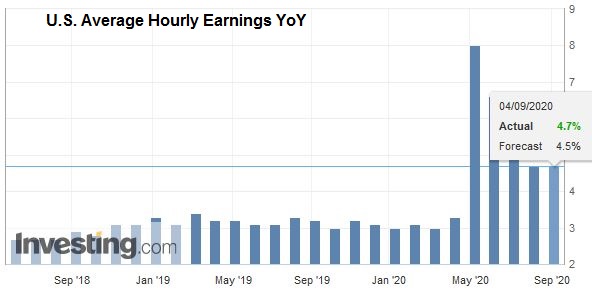

U.S. Average Hourly Earnings YoY, August 2020(see more posts on U.S. Average Hourly Earnings YoY, ) Source: investing.com - Click to enlarge |

Canada also reports August employment data. The median forecast in the Bloomberg survey calls for a 250k increase after a 418k rise in July. The unemployment rate was at 10.9% in July and may have fallen to 10.2% in August. The mix between full and part-time jobs may be important, but the market’s response is often more about the reaction to the US data. Separately, note that today begins Mexico’s pre-approval procedures for steel exports to the US. These were announced to avoid the lower quotas that the US has imposed some types of Brazilian steel and Canadian aluminum.

The US dollar recovered to about CAD1.3160 in yesterday’s surge. Recall that the greenback has traded briefly below CAD1.30 earlier this week for the first time since January. Yesterday’s move stalled in front of the 20-day moving average (~CAD1.3175). The US dollar has not closed above since July 14. Initial support is seen near CAD1.3080, but yesterday’s low was around CAD1.3040 is likely to be stronger. The sell-off in equities yesterday failed to deter the peso buying. The dollar fell for the third consecutive session against the peso and is heavier today. It is approaching the 200-day moving average (~MXN21.5180), which it has not traded below since March. The June low is in the MXN21.46-MXN21.47 area.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, July 16: Equities Slide and the Greenback Bounces After China’s GDP and Before the ECB

FX Daily, July 16: Equities Slide and the Greenback Bounces After China’s GDP and Before the ECB

Overview: Profit-taking, perhaps spurred by disappointing retail sales figures, sent Chinese equity markets down by 4.5%-5.2% today, the most since early February. It appears to be triggering a broader setback in equities today. The Hang Seng fell 2%, and most other markets in the region were off less than 1%.

FX Daily, August 07: Position Adjustment Dominates ahead of US/Canada Employment Reports

FX Daily, August 07: Position Adjustment Dominates ahead of US/Canada Employment Reports

Escalating dramas may be behind the position adjustment today ahead of the US jobs data. The US and China feud expanded beyond Tiktok to WeChat, and efforts to tighten disclosure rules for Chinese companies listed in the US are nearing. The negotiations between the White House and the Democrats broke down, preventing or at least delaying additional stimulus.

FX Daily, August 17: The Dollar Softens to Start the New Week

FX Daily, August 17: The Dollar Softens to Start the New Week

The capital markets are looking for direction. Asia Pacific equity markets were mixed, with gains in China, Hong Kong, and Taiwan countering losses in Japan, South Korea, and Australia. European and US shares are trading slightly firmer.

FX Daily, August 19: US Equities Outperform but Does Little for the Heavy Greenback

FX Daily, August 19: US Equities Outperform but Does Little for the Heavy Greenback

Overview: The S&P 500 and NASDAQ set new all-time highs yesterday, but the continued outperformance of US equities have failed to lend the dollar much support. It was sold to new lows for the year yesterday against the euro, sterling, the Swedish krona, and the Australian dollar.

FX Daily, August 24: Markets Prove Resilient to Start New Week

FX Daily, August 24: Markets Prove Resilient to Start New Week

New virus outbreaks in Europe and Asia are not adversely impacting the capital markets today. Global equities are firmer. Some reports suggesting the US ban on WeChat may not be as broad as initially signaled helped lift Hong Kong shares, but nearly all the markets in the region traded higher.

FX Daily, August 26: Hurricane Laura Lifts Oil Prices

FX Daily, August 26: Hurricane Laura Lifts Oil Prices

A consolidative tone has emerged after US equity benchmarks reached new highs yesterday. The MSCI Asia Pacific Index had reached seven-month highs on Tuesday, but Japan, China, and Australian stocks saw modest profit-taking today. European shares are recouping yesterday’s minor loss, and US shares are flat.

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 1: Dollar Lurches Lower

FX Daily, September 1: Dollar Lurches Lower

The US dollar has been sold-off across the board. The euro approached $1.20, and sterling neared $1.3450. The greenback traded below CAD1.30 for the first time since January. Most emerging market currencies but the Turkish lira, are also advancing today.

Tags: #USD,China,Currency Movement,Featured,Japan,jobs,NATO,newsletter,treasuries