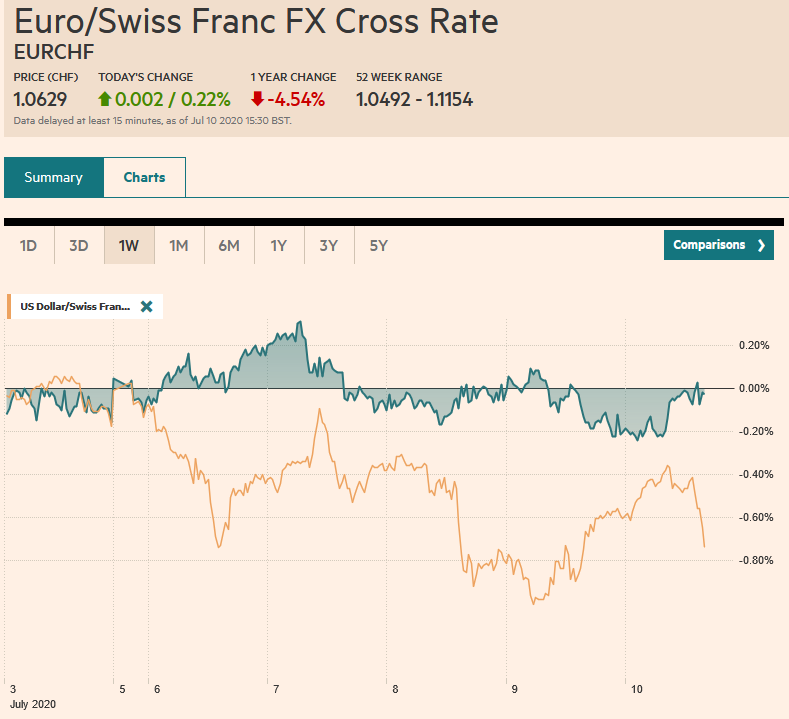

Swiss Franc The Euro has risen by 0.22% to 1.0629 EUR/CHF and USD/CHF, July 10(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Record fatalities in a few US states, coupled with new travel restrictions in Italy and Australia, have given markets a pause ahead of the weekend. News that two state-backed funds in China took profits snapped the eight-day advance in Shanghai at the same time as there is an attempt to rein in the use of margin. Many of the largest markets in the Asia Pacific region fell by 1-2%, This pared the weekly gains in most markets, but sent the Nikkei and Kospi lower for the week. European shares are trying to snap a three-day fall. Several sectors are higher through the morning session,

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, Canada, China, Currency Movement, EUR/CHF and USD/CHF, Featured, Federal Reserve, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.22% to 1.0629 |

EUR/CHF and USD/CHF, July 10(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Record fatalities in a few US states, coupled with new travel restrictions in Italy and Australia, have given markets a pause ahead of the weekend. News that two state-backed funds in China took profits snapped the eight-day advance in Shanghai at the same time as there is an attempt to rein in the use of margin. Many of the largest markets in the Asia Pacific region fell by 1-2%, This pared the weekly gains in most markets, but sent the Nikkei and Kospi lower for the week. European shares are trying to snap a three-day fall. Several sectors are higher through the morning session, but the drag is coming from consumer discretionary, energy, and financials. US shares are trading lower, and the S&P 500 advance for the week of about 0.7% could be halved in the early going. Bonds are drawing the safe-haven bid. The US 10-year is slipping below 60 bp, and core European bond yields are mostly a couple of basis points lower. The US and UK five-year yields are at new record lows (~ 26 bp and -9 bp, respectively). The dollar enjoys a firmer bias, though the yen and Swedish krona (maybe related to bond purchases), are posting modest gains, and the euro and sterling have recovered from earlier losses and are little changed. Of note, the dollar has pushed through JPY107 to visit levels not seen for a couple of weeks. The losses in emerging market currencies between yesterday and today has left the JP Morgan Emerging Market Currency Index practically flat on the week. Gold is trading near $1807 an ounce, but the upside momentum seen earlier this week has stalled. The International Energy Agency warned that the new flare-up of cases can weaken the demand for oil. After falling 3% yesterday, August WTI is being drilled another 2% today. It is below $39 a barrel for the first time this month. |

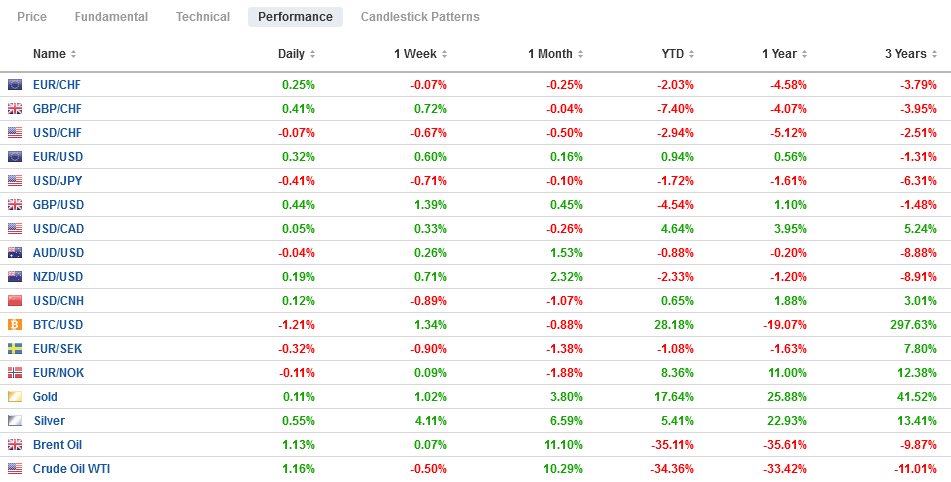

FX Performance, July 10 - Click to enlarge |

Asia Pacific

News on the ground was thin. The surge in virus cases and the decline in US equities took a toll on regional markets. After initially seemingly encouraging equity buying, Chinese state organizations seemed to have drawn more cautious yesterday before a couple of state-run funds were quite public about their plans to take profits. Reports indicate that foreign-based funds also were sellers and for the first time this month today. Chinese data show that foreign funds were net buyers of CNY63 bln of equities this month through the linked connections. They reported slow CNY4.4 bln today, the most in almost four months. Separately, China said bank lending in June was in line with expectations (~CNY1.8 trillion), but the shadow banking surged more than expected.

The risk-off moment has seen the US dollar slump to about JPY106.70, its lowest level since June 24. Little support is seen ahead of JPY106.00. On the top side, the JPY107.00-JPY107.15 may offer nearby resistance. The Australian dollar has held above this week’s lows (~$0.6920) in the local time zone before recovering toward $0.6960 in the European morning. The intraday technicals are getting stretched. Look for resistance near $0.6970 to off the nearby cap. The broad US dollar strength proved enough to resurface above CNY7.0 after falling through yesterday.

Europe

European finance ministers picked Ireland’s Donohoe to be the Eurogroup President despite a consensus among the large countries to support Spain’s Calvino to replace Portugal’s Centeno, who is leaving the finance minister to govern the central bank. Donohoe will assume the office until mid-September. Still, a fair question is whether his selection sheds any light on the likelihood of a compromise at the July 17-18 summit about the EU Recovery Plan and budget. Did resisting Germany and France here, for example, serve as a catharsis so they will support the EC compromise? Was it a shot across the bow of the European leadership warning that it is not just the “Frugal Four” that is pushing back.

Italy and France reported large jumps in May industrial output. Italy’s industrial production surged a whopping 42.1% in May, almost twice what economists anticipated, and signals a strong recovery from the revised 20.5% drop in April (initially reported as -19.1%). The French bear was not as much, but still solid. French industrial output rose by 19.6%. Economists had hoped for around a 15.5% increase after a 20.6% slide in April (initially reported as -20.1%). Manufacturing jumped back by 22% (-22.3% in April).

The euro was sold to about $1.1255 before finding a good bid. The low for the week was set on Monday, near $1.1240. It has recovered to almost $1.13 in the European morning. It may find additional gains more difficult. There is an option for about 530 mln euros at $1.13 that expires today. The intraday technicals are stretched. The US is threatening to announce new levies on French goods in retaliation for the digital tax. Similarly, sterling has recovered from the initial selling that took it to almost $1.2565 in late Asia. It traded back to nearly $1.2620 in by midday in Europe. The intraday technicals are stretched, suggesting North American deals will be reluctant to chase it. Immediate resistance is seen near $1.2630.

America

The Fed’s balance sheet fell by $88 bln last week, the fourth weekly decline. Over this stretch, the balance sheet has shrunk by nearly $250 bln to around $6.92 trillion. It sounds kind of simple, but the reason the balance sheet is shrinking is that some things (swaps for foreign central banks and lending to primary dealers) are falling faster than the Fed is buying new assets. It purchased less than a billion dollars of corporate bonds in the past week, and the Main Street facility has yet to make a loan.

Central banks sold Treasuries from their custody account at the Federal Reserve for the second consecutive week. The $11 bln divestiture followed almost a $9 bln liquidation of the previous week. One would suspect an emerging market, but over the past two weeks, emerging market currencies have not been particularly volatile, and in this context, weak currencies are potential candidates. The weakest was the Russian rouble (~-2.6%). It has no Treasury holdings to speak of (~$7 bln as of April, according to US figures) and is most unlikely to use the Fed’s custody services. The next weakest was the Indonesian rupiah, a 1.5% decline. Maturing issues that are not recycled could also appear as a drawn down in holdings.

The US June reading of producer price may not attract much attention today. Headline PPI is likely to have remained in slight deflationary territory (below zero) but less than in May -0.8%). Excluding food and energy, producer prices have fared better. But at 0.3%-0.4% year-over-year, the lack of so-called pipeline pressure is clear. Canada’s jobs report is released at the same time. It is expected to report a strong recovery in jobs. The median forecast in the Bloomberg survey is for a 700k increase after an almost 290k rise in May. The unemployment rate may fall back to 12.1% from 13.7%. Mexico reports May industrial production figures. A small recovery is expected after falling by a quarter in April.

The US dollar made a marginal new high for the week against the Canadian dollar, just above CAD1.3620 in late Asia Pacific turnover. The greenback was consolidating near CAD1.3600 in the European morning, and initial support is seen near CAD1.3575. The week’s low was set yesterday around CAD1.3490. The US dollar is firm against the Mexican peso. It appears poised to test the high for the week near MXN22.90. The greenback finished last week a little below MXN22.40 and four-day decline in tow. With the dollar near MXN22.76, roughly had of last week’s 2.9% decline has been retraced this week.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, July 6: New Record Number of Covid Cases Doesn’t Curtail Appetite for Risk

FX Daily, July 6: New Record Number of Covid Cases Doesn’t Curtail Appetite for Risk

Overview: A new daily high number of contagions globally has been reported, but the risk-appetites have been stoked. Chinese stocks have been on a tear. The Shanghai Composite rallied 5.7% today to bring the five-day advance to 13.6%. Most other regional markets, including Hong Kong, rallied as well (3.8%). Australia was the main exception, and it pulled back by 0.7%. It is still up a solid 3.4% over the past five sessions.

FX Daily, February 12: The Greenback Slips in Subdued Activity

FX Daily, February 12: The Greenback Slips in Subdued Activity

Investors appear to be increasingly looking past the latest coronavirus from China as new afflictions slow. Despite the soggy close of US equities yesterday, Asia Pacific bourses are nearly all higher, led by more than 1% gains in Singapore and Thailand. The Dow Jones Stoxx 600 is at new record highs, led by consumer discretionary and materials sectors.

FX Daily, February 14: Investors Continue to Look Past the Coronavirus

FX Daily, February 14: Investors Continue to Look Past the Coronavirus

Overview: The capital markets are heading into the weekend, still trying to look past the coronavirus despite the new cases in Hubei. Tokyo was a notable exception in the Asia Pacific region, as the other major equity markets, like in Hong Kong, China, Taiwan, South Korea, and Australia, advanced. The MSCI Asia Pacific Index rose for the second week.

FX Daily, February 19: Investors’ Confidence Snaps Back

FX Daily, February 19: Investors’ Confidence Snaps Back

Overview: After shunning risk yesterday, investors re-entered the fray today, and the animal spirits returned. The MSCI Asia Pacific Index snapped a four-day slide, and China’s markets were among the few losers in the region today. Europe’s Dow Jones Stoxx 600 recovered yesterday’s losses in full and is again at record highs. US shares are also trading firmer and are poised to recoup yesterday’s decline.

FX Daily, April 03: Oil Firm, Greenback Extends Gains

FX Daily, April 03: Oil Firm, Greenback Extends Gains

Overview: Global equities are finishing the week on a soggy tone despite the 2%+ gains seen in the US yesterday. The extension of shutdowns, rising contagion and fatality rate, and imploding economies weigh on prices. In Asia, Korea and Indonesia bucked the trend to most minor gains. Europe is giving back yesterday’s gains, and the Dow Jones Stoxx 600 is nearly flat on the week.

FX Daily, May 8: Jobs and Negative Fed Funds Futures

FX Daily, May 8: Jobs and Negative Fed Funds Futures

Overview: The S&P 500 closed near its session lows for the third day running yesterday but failed to deter the bulls in Asia-Pacific, where most markets rose by more than 1%. Taiwan, Korea, and Australia lagged a bit though closed higher. Europe’s Dow Jones Stoxx 600 is firm, and the modest gains (~0.5%) would be enough to ensure a higher weekly close if it can be maintained.

FX Daily, June 8: Monday Blues: Consolidation Threatened

FX Daily, June 8: Monday Blues: Consolidation Threatened

Overview: The MSCI Asia Pacific Index rose for a sixth consecutive session. Japan, Taiwan, Singapore, and Indonesian markets advanced more than 1%. European bourses are mixed, with the peripheral shares doing better than the core, leaving the Dow Jones Stoxx 600 about 0.5% lower near midday after surging 2.5% ahead the weekend. US shares are firm, as is the 10-year yields, hovering near 92 bp.

FX Daily, July 1: Second Verse Can’t be Worse than the First, Can it?

FX Daily, July 1: Second Verse Can’t be Worse than the First, Can it?

The resurgence of the contagion in the US has stopped or reversed an estimated 40% of the re-openings, but the appetite for risk has begun the second half on a firm note, helped by manufacturing PMIs that were above preliminary estimates or better than expected. Except for Tokyo and Seoul, equities in the Asia Pacific region rose. The MSCI Asia Pacific Index rose almost 15.5% in Q2.

Tags: #USD,$CNY,Canada,China,Currency Movement,EUR/CHF and USD/CHF,Featured,federal-reserve,newsletter