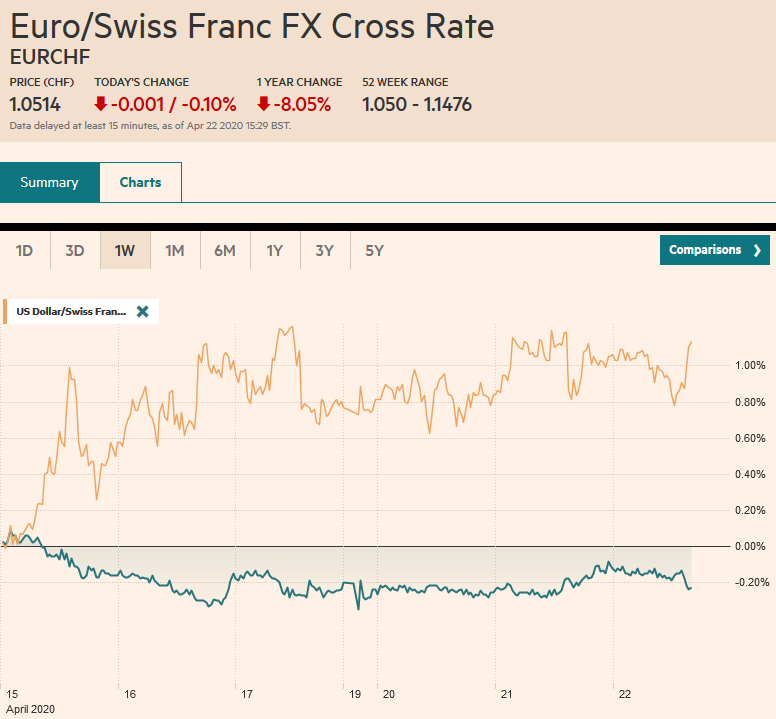

Swiss Franc The Euro has risen by 0.09% to 1.0562 EUR/CHF and USD/CHF, April 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Risk-appetites appear to have stabilized for the moment. Most equity markets are higher. Japan and Malaysia were exceptions, but the MSCI Asia Pacific Index rose for the first time this week. In Europe, the Dow Jones Stoxx 600 is recouping about a third of yesterday’s loss. The S&P 500 gapped lower yesterday, and although US shares are firmer, that gap (~2785.5=2820.4) is the key to the near-term outlook, Core yields are a little higher, and the US 10-year is around 58 bp. Italian bonds are little changed, but Spanish and Portuguese yields are more 7-8 bp higher. The US dollar is

Topics:

Marc Chandler considers the following as important: 4) FX Trends, 4.) Marc to Market, COVID-19, Currency Movement, EUR/CHF, Featured, Hong Kong, Italy, Mexico, newsletter, Oil, U.K. Consumer Price Index, U.K. Core Consumer Price Index, U.S. House Price Index, USD, USD/CHF

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Swiss FrancThe Euro has risen by 0.09% to 1.0562 |

EUR/CHF and USD/CHF, April 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Risk-appetites appear to have stabilized for the moment. Most equity markets are higher. Japan and Malaysia were exceptions, but the MSCI Asia Pacific Index rose for the first time this week. In Europe, the Dow Jones Stoxx 600 is recouping about a third of yesterday’s loss. The S&P 500 gapped lower yesterday, and although US shares are firmer, that gap (~2785.5=2820.4) is the key to the near-term outlook, Core yields are a little higher, and the US 10-year is around 58 bp. Italian bonds are little changed, but Spanish and Portuguese yields are more 7-8 bp higher. The US dollar is lower against the major currencies, with the dollar bloc outperforming and the euro complex is little changed. For the first time in three sessions, JP Morgan’s Emerging Market Currency Index is posting small gains. Gold, which had tested the $1660 area is back knocking on $1700. June WTI was sold when it poked above $14 and is now around $10. June Brent reached $16 a barrel, its lowest since the late 1990s, and is now a little below $19. |

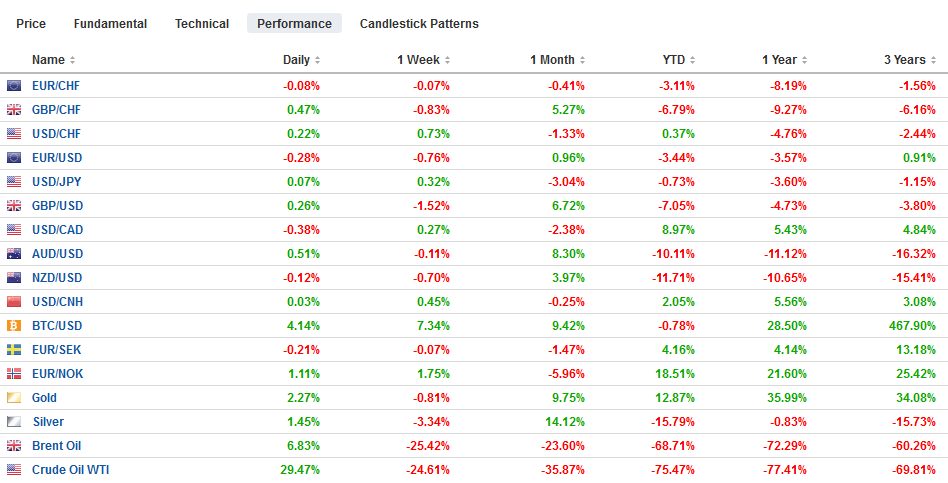

FX Performance, April 22 - Click to enlarge |

Asia Pacific

Singapore, which had done well in the early phases of the pandemic, has seen a reversal of fortunes. It now has the most case in Southeast Asia, according to reports. Foreign worker dormitories apparently have been a crucial center of the outbreaks.

Preliminary March retail sales data from Australia saw a surge in hygiene products and dried food as households prepared to be homebound. Sales appeared to peak in mid-March as the lockdown began. The strong rise in sales (estimated at about 8.2% on the month) should be recognized as a one-off event, and consumption will likely be a drag on Q2 GDP.

There are two developments in Hong Kong to note. First, interest rate differential has seen the Hong Kong dollar trade on the top side of the band, and like yesterday, the Hong Kong Monetary Authority intervened and bought around $360 mln US dollar (selling HKD2.79 bln). It represented a modest increase from Tuesday’s operation. Additional intervention is likely in the near-term. Second, HK’s Chief Executive Lam announced the most prominent cabinet reshuffle to date, involving five senior officials, including the minister that oversees the relationship with Beijing. The arrests of more than a dozen leaders of the recent protest movement over the past weekend will add to the social tensions.

For the third consecutive session, the dollar has held below JPY108.00. Support has been found in the JPY107.30-JPY107.50 area. The intraday technicals suggest the market is more likely to test the upside in North America. There is an option for $1.7 bln at JPY108.25 that should limit any breakout. The Australian dollar is has recouped yesterday’s roughly 0.9% fall to briefly poke above yesterday’s high just below $0.6350. The intraday technicals suggest the upside may be limited. Support is seen near $0.6300. The Chinese yuan edged slightly higher today after the dollar approached CNY7.10 yesterday.

Europe

Italy’s bonds sold off hard yesterday. The 10-year yield jumped nearly 22 bp to 2.15%. The 30-year soared 30 bp to 3.00%. One would have thought that the ECB’s flexible Pandemic Emergency Purchase Program would have been deployed to prevent precisely this. It is not as if there is a buyers’ strike. Consider that for the syndicated five-year bond that was sold yesterday, orders were for 110 bln euros for the 16-bln euro issue. S&P will announce the conclusion of its rating review of Italy at the end of the week. It is rated BBB. Moody’s will review its Baa3 (BBB-) rating next month.

Reports suggest the ECB will have a teleconference call today to discuss whether it should further liberalize its collateral rules to allow below investment grade securities. The problem is that it is possible that a sovereign (see Italy above) and some businesses may lose their investment-grade status during the crisis. The ECB has tried to gain some room to maneuver so as not to be beholden to the rating agencies. It tends to rely on the highest of the four major rating agencies, which includes DBRS.

Separately, the EU heads of state hold their teleconference tomorrow. There is a debate now over the form of assistance, grants, or loans. One is reminded of the incredible problems caused by inter-ally debts of World War I, and the innovation for World War II, of the Lend-Lease program, which minimized loans, and arguably helped facilitate a quicker recovery.

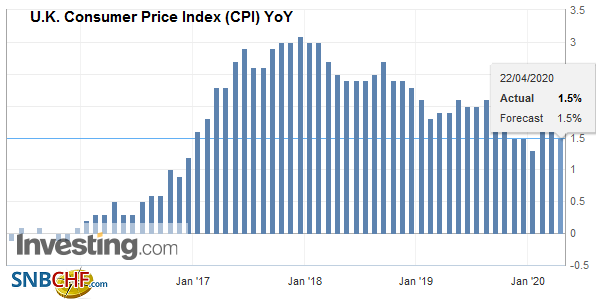

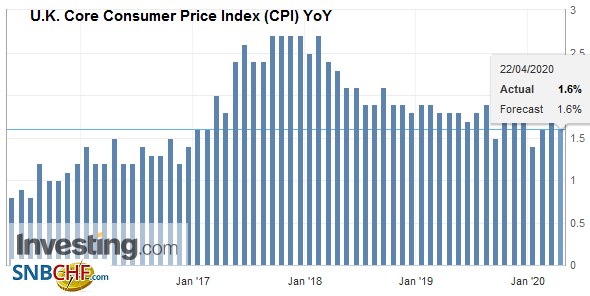

| The euro has been confined to a little more than a quarter-cent range today, mostly above $1.0850. Large expiring options today and tomorrow may serve to keep it on a $1.08-handle. Today there are options at $1.0825 (1 bln euros) and $1.0900 (1.5 bln euros) that expire. Tomorrow, there are options at $1.08 (1.6 bln euros) and $1.09 (1.4 bln euros) that expire. Disinflationary forces in the UK (slower increase in CPI and outright declines in PPI) failed to impact sterling. |

U.K. Consumer Price Index (CPI) YoY, March 2020(see more posts on U.K. Consumer Price Index, ) Source: investing.com - Click to enlarge |

| It is stabilizing after falling 1.2% yesterday, the most in a little more than a month. It pushed above $1.2350 in the European morning after testing the $1.2250 area yesterday. The intraday technicals are stretched ahead of the North American open, and the $1.2380 area may be sufficient to check stronger gains. Lastly, the central bank of Turkey is widely expected to announce a 50 bp rate cut shortly. However, the risk is of a larger rather than a smaller move. The dollar holding just below the TRY7.0 level ahead of the announcement. |

U.K. Core Consumer Price Index (CPI) YoY, March 2020(see more posts on U.K. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

AmericaThe Fed has bought nearly as many assets as it did under QE1 (2009, $300 bln) and QE2 (2010 $600bln) put together. This aggressiveness will weigh on the dollar down the road is increasingly cited as a bear case for the greenback. Yet there two good reasons not to over-emphasize this consideration. First, the relative size of central bank balance sheets was not particularly helpful in understanding or anticipating exchange rate changes in recent years. Second, the Fed’s balance sheet is now about 30% of GDP. The ECB’s are around 40% of its GDP, and the BOJ’s balance sheet is over 100% of Japan’s GDP. Even a balance sheet focus would not necessarily point to a weaker dollar. There are other factors. Emerging from the Great Financial Crisis, the dollar rallied on a divergence of policy thrusts and later on the policy mix. Interest rates were higher, as was the return on capital. The US Senate approved a roughly $485 bln package that includes about $320 bln for the Payroll Protection Plan that turns loans into grants for small and medium businesses that maintain or rehire employees. There are also funds for coronavirus testing and for hospitals. The House is expected to now vote on the bill tomorrow. Meanwhile, another aid package that includes assistance for state and local government is in the early stages of negotiations. |

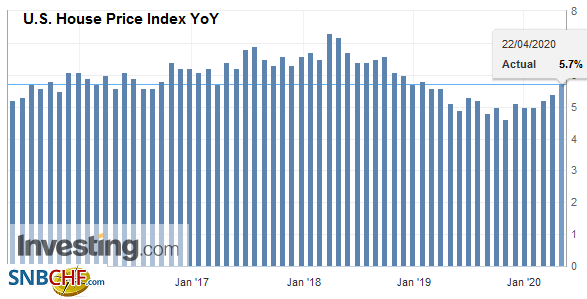

U.S. House Price Index YoY, February 2020(see more posts on U.S. House Price Index, ) Source: investing.com - Click to enlarge |

There are two other talking points today. The first is the US oil inventory report. Late yesterday, API estimated that US holdings rose by 13.2 mln barrels last week, and combined, the gasoline and distillate stocks from by a11.1 mln barrels. The EIA estimate is regarded as more robust and is expected to show a 14 mln barrel build. Cushing’s holdings will be watched closely as it is approaching capacity. The other talking point is about Missouri’s lawsuit against China over Covid-19. This is more about thunder than rain. US states suing foreign governments is a difficult legal course to tread, and the case will be most like dismissed, not on merit but on procedural grounds.

The Mexican peso was trading near two-week lows when the central bank surprised with a 50 bp rate that brought the target rate to 6.0%. It is the third cut in three months for a total of 125 bp. There is scope for more cuts as inflation was at 3.25% in March and falling. President AMLO is reluctant to deploy its fiscal powers, which so far has been mostly about speeding up payments of existing programs to low-income households and loans to small businesses. The IMF estimates its fiscal support to be less than 1% of GDP. Between the domestic economic hit, hard currency inflows from tourism, worker remittances, and oil are drying up. The IMF projects the Mexican economy to contract by 6.6% this year after failing to grow last year. The price of insuring against a sovereign default for five years (CDS) rose to nearly 300 bp yesterday, the highest since the Great Financial Crisis, when it was twice as high.

The US dollar reached CAD1.4265 yesterday, its best level since April 2, when it tested CAD1.43. It is on its session lows in late European morning turnover and a little above yesterday’s low near CAD1.4115. Although penetration is possible, a deeper pullback by the US dollar seems unlikely as the intraday technicals are already getting stretched. The Mexican peso is also consolidating yesterday’s loss. Support for the US dollar is seen near MXN24.20, and initial resistance is pegged around MXN24.40.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, October 23: Markets Lack Much Conviction, Await Fresh Developments

FX Daily, October 23: Markets Lack Much Conviction, Await Fresh Developments

Overview: UK Prime Minister Johnson is neither dead in a ditch as he said he would prefer to be than request an extension of Brexit, nor will the UK leave the EU at the end of the month. Yesterday’s vote rejected the attempt to fast-track the legislation needed to support the divorce agreement. It all but ensures that such a delay will be forthcoming.

FX Daily, February 26: Dramatic Investor Adjustment Continues

FX Daily, February 26: Dramatic Investor Adjustment Continues

Overview: The warning by the US Center for Disease Control and Prevention that Americans should prepare for an outbreak of Covid-19 sent the S&P 500 tumbling to an 11-week low and the 10-year Treasury yield to a record low near 1.30%. The volatility of the S&P (VIX) jumped to its highest level since 2018. The sell-off in global equities continues unabated.

FX Daily, November 11: Dollar Consolidates and Equities Follow Asia Lower

FX Daily, November 11: Dollar Consolidates and Equities Follow Asia Lower

Overview: Escalating violence in Hong Kong and the continued fall in Chinese producer prices weighed on equities in Asia Pacific trading. The MSCI Asia Pacific Index has risen nearly 7% during the five-week rally and is off to a weak start this week. Hong Kong’s Hang Seng fell around 2.6%, its biggest loss in three months, and China’s CSI 300 was off 1.75%. Nearly all the local markets fell but Australia.

FX Daily, November 19: Hong Kong Stocks Rally as Stand-Off Continues

FX Daily, November 19: Hong Kong Stocks Rally as Stand-Off Continues

Overview: The run-up in equities continues to be the dominant development in the capital markets. Although the Japanese and South Korean bourses fell, the rise in Australia, China, Hong Kong, and Taiwan underpin the MSCI Asia Pacific Index. The Hang Seng’s gains (1.5% on top of yesterday’s 1.3% rise) is notable as the situation on the ground remains intense and unresolved.

FX Daily, November 21: Markets Hear What it Wants from China’s Chief Negotiator, but HK maybe New Obstacle

FX Daily, November 21: Markets Hear What it Wants from China’s Chief Negotiator, but HK maybe New Obstacle

Overview: The strongest signs to date that even phase one of a US-China trade deal is proving elusive helped spur the risk-off mood that had already been emerging. The S&P 500 fell by the most in a month (~-0.40%) yesterday, closing the gap from last week we had noted was the risk, and follow-through selling was seen in Asia Pacific and Europe.

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

Overview: The ring of containment of Covid-19 has grown from China. The new frontline is Japan, South Korea, Italy, and Iran. A lockdown of around 50k people near Milan and Austria blocking trains from Italy is scaring investors. Asian markets fell, but South Korea bore the brunt with a nearly 4% decline. The national holiday in Japan spared local equities.

FX Daily, April 16: Markets Brace for another Jump in US Weekly Jobless Claims

FX Daily, April 16: Markets Brace for another Jump in US Weekly Jobless Claims

Overview: Equity losses in the US appeared to drag most Asia Pacific markets lower today, with China and India the notable exceptions. European bourses are higher, and the only energy sector is a drag on the Dow Jones Stoxx 600, which is around 1% higher in late morning turnover, while US shares are also trading firmer. Asia Pacific 10-year benchmark yields eased.

FX Daily, April 21: Oil Drilled Below Zero, Equity Rally Stalls, Greenback Advances

FX Daily, April 21: Oil Drilled Below Zero, Equity Rally Stalls, Greenback Advances

Overview: Oil’s wild ride has been joined by two other developments that are keeping investors off-balance. First, reports suggest that North Korea’s Kim Jong-Un maybe in critical condition after surgery. He apparently was absent from last week’s events celebrating his grandfather. The concern is about a potential power vacuum and the command and control of North Korea’s weapons. Second, in a tweet late yesterday, US President Trump said he would sign an executive order suspending immigration, ostensibly to fight the virus and protect jobs. No details were provided. Trump has also renewed his threat to stop imports of Saudi and Russian oil. These disruptions have seen global equities fall. Following yesterday’s 1.8% decline of the S&P 500, most of Asia Pacific’s major bourses

Tags: #USD,COVID-19,Currency Movement,EUR/CHF,Featured,Hong Kong,Italy,Mexico,newsletter,OIL,U.K. Consumer Price Index,U.K. Core Consumer Price Index,U.S. House Price Index,USD/CHF