Swiss Franc The Euro has risen by 0.52% to 1.0944 EUR/CHF and USD/CHF, September 09(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The improvement of investor sentiment seen last week is carrying over into the start of the new weeks. Global equities are firm as are benchmark yields. Asia Pacific equities advanced, except in Hong Kong, where Chief Executive Lam’s promise to formally withdraw the controversial extradition bill failed to deter protests. European markets extended their three-week advance at the open, but are struggling to sustain the upside momentum. US shares are trading with a firmer bias. Benchmark 10-year yields are rising three-four basis points in Europe, with US Treasury yield pushing up

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, China, Currency Movement, Featured, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.52% to 1.0944 |

EUR/CHF and USD/CHF, September 09(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The improvement of investor sentiment seen last week is carrying over into the start of the new weeks. Global equities are firm as are benchmark yields. Asia Pacific equities advanced, except in Hong Kong, where Chief Executive Lam’s promise to formally withdraw the controversial extradition bill failed to deter protests. European markets extended their three-week advance at the open, but are struggling to sustain the upside momentum. US shares are trading with a firmer bias. Benchmark 10-year yields are rising three-four basis points in Europe, with US Treasury yield pushing up toward 1.60%. Yields were softer in the Asia Pacific region. The dollar is in lower though narrow ranges against the major currencies, but the Japanese yen and Swiss franc. The euro and sterling are firmer but little changed. Among emerging market currencies, the Turkish lira, the Chinese yuan, and Mexican peso laggards, with most of the others gaining against the US dollar. Crude oil prices are firmer, but the market showed little reaction to news that Saudi Arabia replaced its long-time oil minister with a son of the King. With an OPEC+ meeting on the sidelines of the World Energy Congress later this week, investors will be particularly sensitive to any indication that the change in personnel reflects a change in policy. |

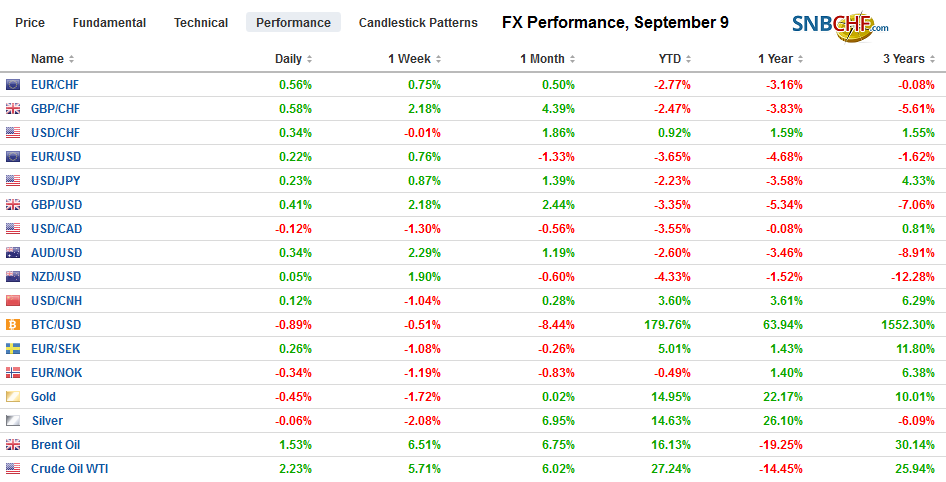

FX Performance, September 9 - Click to enlarge |

Asia Pacific

China’s trade surplus fell sharply in August as exports unexpectedly fell. The trade surplus of $34.8 bln compares with $44.6 bln in July. Overall exports fell 1% year-over-year after rising 3.3% in July. Exports have been in a sawtooth pattern since late last year, alternating monthly between gains and declines. Of note, exports to the US were off 16% year-over-year. Remember the US tariffs are applied to particular goods, say steel pipes, not to a dollar value as is often used in shorthand, like $250 bln of goods. China’s trade surplus with the US stood at $26.95 bln, according to the Chinese figures, meaning that it accounted for more than three-quarters of the PRC’s trade surplus. Imports fell by 5.6%, year-over-year. They have been declining on a year-over-year basis since last December, with the lone exception of April. Yet oil imports rose 3% in August and are up almost 10% year-over-year and nearly 10 mln barrels a day. China has been the third-largest buyer of US crude oil this year, and its new oil tariffs may reduce its demand from the US. Meanwhile, refinery margins are reportedly recovering, and this may lead to new marketing drives. Lastly, note that as a goodwill gesture ahead of the face-to-face sometime next month, apparently after the US 25% tariffs are lifted to 30% on October 1, China reportedly agreed to make some grain purchases. We suspect this points to where China has not been able to fully replace US inputs. China’s soy imports rose to the highest in three years, while iron ore imports were the most since January 2018.

| Japan revised Q2 GDP to 1.3% from the 1.8% initial estimate. The main culprit seems to be business investment. It rose only 0.2%, not 1.5% as had been previously estimated. It follows a 0.2% decline in Q1. Separately, Japan reported a JPY2 trillion July current account surplus. The current account surplus conceals the deterioration of Japan’s trade balance. On a balance of payments basis, Japan reported a trade deficit of JPY74.5 bln in July. To put this in perspective, consider that last year’s trade surplus averaged JPY254 bln a month in the first seven months. This year’s average is less than 1/10 at JPY21.4 bln. Separately, the balance of payments data showed Japanese investors bought JPY2.47 trillion (~$23 bln) of US Treasuries in July, the most in three years. |

Japan Gross Domestic Product (GDP) YoY, Q2 2019(see more posts on Japan Gross Domestic Product, ) Source: investing.com - Click to enlarge |

The dollar is trading in a narrow range (~JPY106.75-JPY107.05) against the yen, which is inside the pre-weekend range that itself was inside the previous day’s range. The consolidative pattern is often associated with continuation. There is a $565 mln option that expires today, which struck at JPY106.95, and there are another $960 mln in expiring options at JPY107.25-JPY107.30. Last week’s high was just below JPY107.25. The Australian dollar is firm and is edging closer to the $0.6880 area, which is an important retracement objective. Support is now pegged near $0.6830. The Chinese yuan is paring some of its pre-weekend gains, and the offshore yuan is snapping a four-day advance.

Europe

Beleaguered UK Prime Minister Johnson pushes for election again today, but the calculus has changed. He will be rebuffed, but he will not give up. There are still a number of moves he can make. At the same time, many EU leaders seem to accept the messy exit but also would be willing to give the UK one final chance for the thinnest of reasons. The weekend resignation of Amber Rudd from the cabinet and as a Tory does not appear to be a game-changer. Johnson met with Ireland’s Prime Minister (Taoiseach) Varadkar today but apparently came empty-handed. Varadkar said he heard no new workable proposals for the vexing Irish border issue. Weekend polls suggest the Tories will likely get more votes than Labour but fall well shy of a majority. In Britain, they like to call this a hung parliament, by which they mean a coalition is necessary.

Ironically, the economic news is better than the political news. The July data shows a stronger than expected recovery from the poor performance in June. The monthly GDP report rose 0.3% after a flat June as industrial production (0.1% vs. -0.3% June), construction output (0.5% vs. -0.7% June), and the services index (0.3% vs. unchanged June) were all better serially and than expected. Tomorrow the UK reports employment figures.

After reporting dismal factory orders and industrial output figures last week, Germany announced that exports unexpectedly rose in by 0.7% in July. Economists had expected a decline. Exports have fallen by an average of 0.1% a month through July, which is the same average as the first seven months of 2018. The trade surplus was also flattered by a 1.5% fall in imports. June imports were revised to a 0.7% gain from 0.5%. The surplus rose to 21.4 bln euros from 16.6 bln. It has averaged 18.7 bln euros this year and 19.8 bln euros in the comparable 2018 period. Unlike, the relationship we noted in Japan, Germany’s trade surplus drives the current account surplus (22.1 bln euros in July).

The euro is in about a 25-tick range above $1.1015. There is a 1.7 bln euro option that expires today at $1.10 and a nearly 630 mln euro option at $1.1025. The pre-weekend high was a little above $1.1055. There is a roughly 920 mln euro option at $1.1050 that will be cut today as well. Ahead of the ECB meeting later this week, it is difficult to envision the euro enjoying much upside momentum. Sterling is firm and appears to have been helped by the data. It is approaching last week’s high near $1.2355. Above there, resistance is around $1.24.

America

The US and Canada economic calendars are light to start the week. At the end of last week, the US reported somewhat disappointing jobs growth, while Canada’s report underscored the central bank’s neutral stance. The US economic highlights this week include PPI, CPI, and retail sales. When the Fed says it is data-dependent, it may mean something more subtle than what it appears. Regardless of this week’s reports, the market is unlikely to b swayed. With a high degree of confidence, it expects a 25 bp rate cut will be delivered next week (September 18).

Mexico reports August CPI today. It is expected to ease, with the median forecast in the Bloomberg survey seeing a 3.16% pace down from 3.78% in July. That would be a new three-year low. Banixco surprised many with a 25 bp rate cut last month. The market is divided about a follow-up cut at the September 26 meeting. However, a full 25 bp cut is discounted for the following meeting in mid-November. Separately, the government’s budget, which assumes 1.5%-2.5% growth next year is more optimistic than the market and the IMF (1.5%).

The Canadian dollar and Mexican peso’s ended seven-week declines last week with a 1% and 2.7% advances respectively. The Canadian dollar remains bid today and near the pre-weekend highs. A convincing break of CAD1.3150 will add to the technical evidence that a US dollar high is in place. However, some caution is advised as last week’s sharp move left the US dollar just below its lower Bollinger Band (~CAD1.3180), and it remains outside of it today. The dollar is pinned near its pre-weekend lows against the Mexican peso. Initial resistance is seen near MXN19.60, and the next technical objective is near MXN19.45. A cap in the Dollar Index is being carved near 98.50. If one is looking for a single level that can give a broad sense of the dollar’s performance, provided this level holds (98.50), the correction/consolidative phase is intact.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,China,Currency Movement,Featured,newsletter