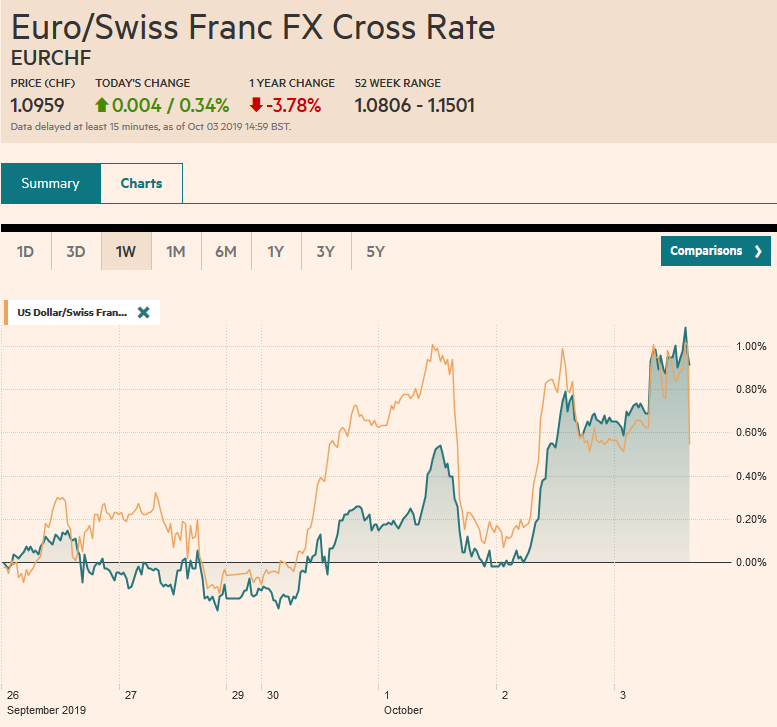

Swiss Franc The Euro has risen by 0.34% to 1.0959 EUR/CHF and USD/CHF, October 3(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Disappointing economic data again drove US equities lower, which in turn carried into Asia Pacific activity. Losses were recorded throughout the region, with the notable exception of Hong Kong. The Nikkei and Australia’s ASX were off by 2%. After its largest losing session of the year (-2.7%) yesterday, Europe’s Dow Jones Stoxx 600 continues to trade heavily. The composite PMI was revised lower (50.1 vs. 50.4 flash). Growth concerns weighed on the dollar yesterday through the interest rate channel. The January 2020 fed funds futures imply about a 75% chance of a cut later this month

Topics:

Marc Chandler considers the following as important: $TRY, 4.) Marc to Market, 4) FX Trends, Brexit, Currency Movement, Eurozone Markit Composite PMI, Eurozone Producer Price Index, Eurozone Retail Sales, Eurozone Services PMI, Featured, Hong Kong, newsletter, trade, U.K. Services PMI, U.S. Initial Jobless Claims, U.S. ISM Non-Manufacturing PMI, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.34% to 1.0959 |

EUR/CHF and USD/CHF, October 3(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Disappointing economic data again drove US equities lower, which in turn carried into Asia Pacific activity. Losses were recorded throughout the region, with the notable exception of Hong Kong. The Nikkei and Australia’s ASX were off by 2%. After its largest losing session of the year (-2.7%) yesterday, Europe’s Dow Jones Stoxx 600 continues to trade heavily. The composite PMI was revised lower (50.1 vs. 50.4 flash). Growth concerns weighed on the dollar yesterday through the interest rate channel. The January 2020 fed funds futures imply about a 75% chance of a cut later this month compared with a little more than a 50% chance a week ago. The greenback has stabilized against the major currencies, which are mostly little changed to lower in the European morning. Emerging market currencies are a little better. Benchmark 10-year bond yields are 2-4 bp lower, and the US yield is pushing under 1.60%. After larger moves yesterday, both gold and oil straddling closing levels. |

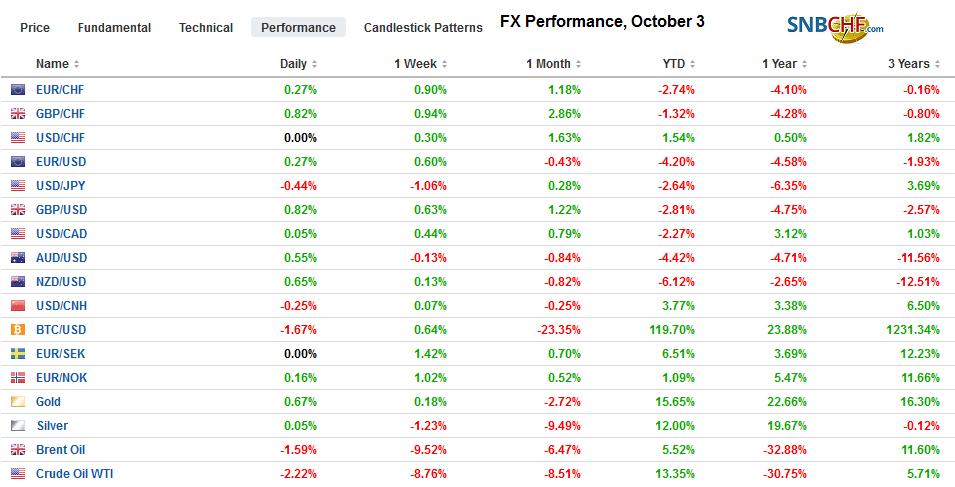

FX Performance, October 3 - Click to enlarge |

Asia Pacific

After writing about Hong Kong’s emergency powers yesterday, we are nevertheless surprised by reports today that this could happen as early as tomorrow. Our point was that China’s interest could be best served by letting Hong Kong deal with the demonstrations and that Hong Kong had the power to do so. The authority stems from a legacy of UK rule. The Emergency Regulation Ordinance dates back to 1922 and was last used by the UK in 1967. Initial reports follow indications that policy groups were advocating imposing curfews and banning masks. Chief Executive Lam will reportedly invoke the authority tomorrow. It grants extensive powers.

Japan’s flash service and composite PMI were confirmed at 52.8 and 51.5, respectively. Both declined from August levels (53.3 and 51.9 respectively). However, the August readings were the best this year and the pullback levels both gauges at their second-best levels. Nevertheless, pressure appears to be mounting on the BOJ to ease policy at the meeting at the end of October. The BOJ’s Funo emphasized the mounting global risks on top of domestic challenges. Efforts to steepen the yield curve by buying fewer long-dated bonds could be enhanced by cutting the short-end. The deposit rate is currently set at minus 10 bp.

The dollar briefly frayed important support we identified at JPY107. Technically, it is potentially the neckline of a double top (~JPY108.50), which, if convincingly penetrated, could signal a move toward JPY105.50. There are about $885 mln of options set between JPY107.00 and JPY107.03 that expire today. On the upside, there are roughly $2.2 bln in expiring options between JPY107.50 and JPY107.75. The Australian dollar is posting a minor gain after making a marginal new 10-year low yesterday near $0.6670. Slightly firmer PMI readings (but a smaller trade surplus) did not prevent extending the beginning of the recovery seen yesterday. It needs to retake the $0.6740 area to begin repairing the technical damage.

EuropeDeja Vu all over again. UK Prime Minister Johnson will again suspend parliament. This time he seeks a shorter prorogation starting October 8 and extending until the Queen’s Speech on October 14. The UK Supreme Court ruled about a week ago that Johnson’s previous attempt was unlawful. The Court noted that rather than a five-week suspension that the more normal prorogation lasts 4-6 days. |

Eurozone Retail Sales YoY, August 2019(see more posts on Eurozone Retail Sales, ) Source: investing.com - Click to enlarge |

| The EU has not rejected the offer out of hand, though it is clear that it is not acceptable in this form. There are two other considerations it appears. First, is it really Johnson’s last best offer, and second, with both Corbyn and Farage rejecting Johnson’s proposals, will he have any better luck than May?

The eurozone PMI was worse than the flash. |

Eurozone Producer Price Index (PPI) YoY, August 2019(see more posts on Eurozone Producer Price Index, ) Source: investing.com - Click to enlarge |

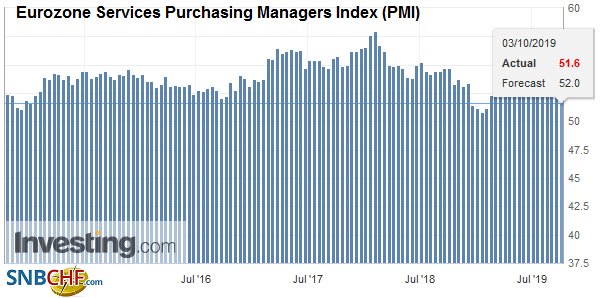

| The services PMI fell to 51.6 from the preliminary 52.0 and August’s 53.5. |

Eurozone Services Purchasing Managers Index (PMI), September 2019(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

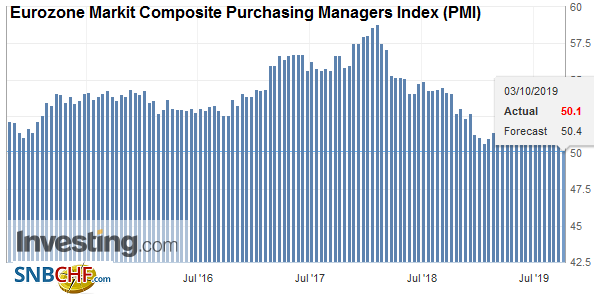

| The composite was dragged lower by downward revisions in Germany and France. It is barely above the 50 boom/bust level at 50.1. The flash was at 50.4, and in August the composite PMI was at 51.9. EMU, it would seem, is stagnating at best. Although the German economic institutes use a more complicated definition of a recession than the two consecutive quarters of contraction, they have lowered their growth forecasts and called for fiscal stimulus earlier this week. |

Eurozone Markit Composite Purchasing Managers Index (PMI), September 2019(see more posts on Eurozone Markit Composite PMI, ) Source: investing.com - Click to enlarge |

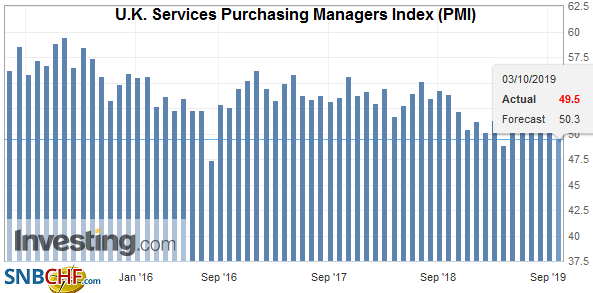

| To be sure, it is not just EMU. The UK economy also hit a wall last month. It services PMI joined the manufacturing below 50 (services 49.5 vs. 50.6 in August) The composite PMI fell to 49.3 from 50.2 and appears to be a new three-year low. Sweden too reported dismal data. The poor manufacturing PMI seen earlier this week (46.3 vs. 51.8) and weak services PMI today (49.8 vs. 54.2) drove the composite to a six-year low (48.8 vs.53.5). |

U.K. Services Purchasing Managers Index (PMI), September 2019(see more posts on U.K. Services PMI, ) Source: investing.com - Click to enlarge |

Turkey reported a larger than expected drop in inflation, and this will set up another rate cut when the central bank meets on October 24. The headline CPI fell to 9.26% from 15.01%, and the core rate stands at 7.54%, down from 13.6%. The sharp decline is mostly a function of the base effect from the lira’s sharp depreciation last year. While there may still be some progress next month, the bulk of the improvement is behind it. Note that monthly inflation readings are slowly accelerating: The average in Q4 18 was 0.28% a month. In Q1 19, it was 0.75% average per month and this increased to 0.89% in Q2 and 1.07% in Q3.

The euro posted back-to-back gains yesterday for the first time in three weeks, and it is trying to extend its streak to three sessions, which it has been unable to do for two months. A couple of expiring options may deter aggressiveness ahead of tomorrow’s US jobs data, where the market does seem to be preparing for a disappointment. There is an option for 1.2 bln euros at $1.0970 and anther 1.7 bln euro at $1.10. The $1.10-level also houses the 20-day moving average, which the euro has not closed above since September 17. Initial support now is seen near $1.0940. Sterling is steady. It has not been above $1.2250 for the past four-sessions and continues to hold below it today. Unless it rises above $1.2325, it will be the third session of lower highs. After testing $1.22 on Tuesday, sterling is recording high lows. Yesterday’s low was slightly above $1.2225 and today it has not been below $1.2265.

AmericaThe US announced its retaliatory measures against Europe after the WTO ruled that Airbus was improperly subsidized. The US is going for the maximum the WTO is allowing even though, in 6-8 months, the WTO appears likely to find that Boeing was also illegally subsidized, giving the EU the right to strike back. In addition to aircraft from Europe that will have a 10% additional levy, a wide range of consumer goods, including single malt Irish and Scotch whiskey, some garments and blankets, coffee, cheese, and olives. Note that aircraft parts are not included in the list of goods and this was important for the Airbus assembly plant in Mobile, Alabama. The tariffs will go into effect on October 18. The US-European trade conflict has been simmering just below the surface since early in the Trump Administration. Europe had been subject to the steel and aluminum tariffs the US claim for national security. The US continues to threaten to slap tariffs on auto imports and must decide by mid-November. |

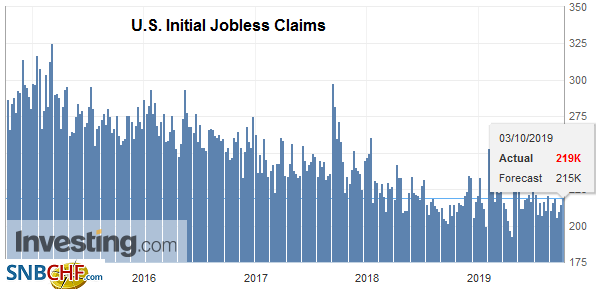

U.S. Initial Jobless Claims, October 2019(see more posts on U.S. Initial Jobless Claims, ) Source: investing.com - Click to enlarge |

| The US calendar is busy today, while diary for Canada and Mexico is light. The US non-manufacturing ISM and the services PMI are the highlights. Earlier this week, the market seemed to ignore the uptick in the manufacturing PMI and focused on the weakness of the ISM. Similarly, yesterday, the market focused on the statistically insignificant miss of the ADP private-sector jobs estimate (135k instead of 140k median forecast in the Bloomberg survey). This is about psychology and seems to reflect the bias among market participants, especially after the data surprise models were near there best levels of the year. August factory goods (expected to have fallen slightly) and the final durable goods orders report are also to be released today, alongside weekly jobless claims. Two Fed governors (Clarida and Quarles) and two regional presidents (Meister and Kaplan) speak today, but the keen interest lies with Powell’s talk tomorrow. |

U.S. ISM Non-Manufacturing Purchasing Managers Index (PMI), September 2019(see more posts on U.S. ISM Non-Manufacturing PMI, ) Source: investing.com - Click to enlarge |

Oil prices fell for the seventh consecutive session and reached a two-month low near $52 a barrel. The broader softness has been sparked by concerns about demand, but the proximate trigger was the largest build in oil stocks according to the EIA in four months. The industry’s estimate (API) of a 5.9 mln barrel draw had short-term traders leaning the wrong way. Total commercial crude and refined product inventories are above year-ago levels.

It seemed that disappointing US economic data spurred the Canadian dollar losses yesterday, as US equities tumbled and oil prices fell. The US dollar shot up to its best level in a month, through the 200-day moving average (~CAD1.33) and recorded an outside up day (trading on both sides of the previous day’s range and then closing above its high). The greenback’s gains have been extended today toward CAD1.3340. A trendline connecting the late May and early September highs comes in near CAD1.3335 today. Above CAD1.3350 and the US dollar can test the September 3 high near CAD1.3385. The US dollar ended a five-day advance against the Mexican peso yesterday after briefly pushing through MXN19.86. Our objective was MXN19.90. Initial support is seen near MXN19.68.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$TRY,Brexit,Currency Movement,Eurozone Markit Composite PMI,Eurozone Producer Price Index,Eurozone Retail Sales,Eurozone Services PMI,Featured,Hong Kong,newsletter,Trade,U.K. Services PMI,U.S. Initial Jobless Claims,U.S. ISM Non-Manufacturing PMI