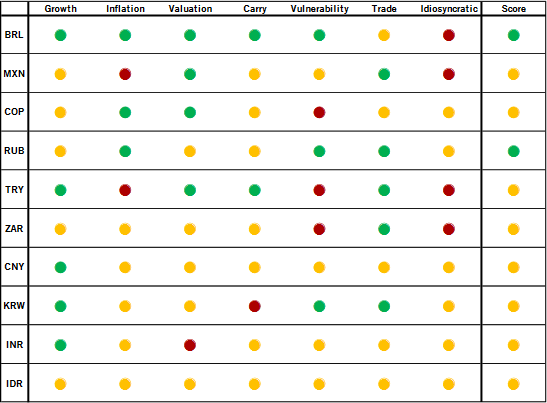

The scope of this note is to present a score card for Emerging Market (EM)currencies, designed to assess the attractiveness of a given currency over the coming 12 months. The scorecard (see chart), constructed using a rules – based methodology, suggests that the Russian rubble and the Brazilian real are currently among the most attractive EM currencies. EM FX scorecard - Click to enlarge Construction of the EM FX scorecard The criteria we singled out to analyse the relative attractiveness of EM currencies are growth, inflation, valuation, carry, vulnerability to external shocks, trade and idiosyncratic drivers. Growth Higher – frequency data than that provided in quarterly GDP reports are needed for the

Topics:

Luc Luyet considers the following as important: Brazilian real, Currency drivers, EM currencies, Featured, global macro, Macroview, newsletter, Pictet Macro Analysis, Russian rouble

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

The scope of this note is to present a score card for Emerging Market (EM)currencies, designed to assess the attractiveness of a given currency over the coming 12 months. The scorecard (see chart), constructed using a rules – based methodology, suggests that the Russian rubble and the Brazilian real are currently among the most attractive EM currencies.

|

EM FX scorecard - Click to enlarge |

Construction of the EM FX scorecard

The criteria we singled out to analyse the relative attractiveness of EM currencies are growth, inflation, valuation, carry, vulnerability to external shocks, trade and idiosyncratic drivers.

Growth

Higher – frequency data than that provided in quarterly GDP reports are needed for the scorecard. We use monthly growth – related indicators such as business surveys, and industrial production and retail sales reports whenever available.

We compute the z-score for all time series and then average them to produce an overall z-score, allowing us to assess how these indicators of economic activity compare historically. The higher the indicator, the better it is for the growth outlook and therefore for the currency. We consider an indicator between +1 and -1 as being neutral for a currency. An indicator above +1 is positive for a currency, and an indicator below -1 is negative.

Inflation

We use the annual change in headline inflation as a further input into the scorecard.

We then compute the z-score, so that we can make a historical comparison of inflation dynamics. An indicator that signals a risk of high inflation is deemed negative for the value of the currency. We consider an indicator between +1 and -1 as being neutral for a currency. An indicator above +1 is negative for a currency, and an indicator below -1 is positive.

Valuation

We use the deviation of the real effective exchange rate from its 10 – year average as a measure of the under – or overvaluation of a currency. We deem a deviation of more than 10% above the 10 – year average as indicating that a currency is overvalued, whereas a deviation percent of more than 10% below the 10 – year average means a currency is undervalued. Between these two markers, currency valuations are consider ed neutral.

Carry

We use the 12 – month deposit rate spread over the US dollar as an indicator of the carry potential of a given EM currency. The signal given by this indicator is analysed in relation to a universe of major EM currencies. More precisely, after having measured the range of spreads in this universe, we segment it into three sub – ranges of equal size. Currencies in the sub – segment that have high deposit spreads over the US dollar are deemed to offer an attractive carry while currencies in the sub – segment with the lowest deposit spreads over the US dollar are deemed unattractive in terms of carry. Furthermore, given than investments in EM currencies are usually funded via the US dollar, a negative spread will automatically be signalled as negative regardless of its position within the range of spreads.

Vulnerability to external factors

We use the current account balance as a percentage of GDP and the ratio of short – term external debt to FX reserves as an indication of how vulnerable a currency is to external shocks.

Serious current account deficits or a shortfall in FX reserves compared to short – term external debt is automatically considered a negative signal. Either an elevated current account surplus or a large FX reserve is necessary to signal that the external buffers protecting a currency are strong.

Trade

We use an openness index, based on the sum of imports and exports divided by GDP, as a way to assess the exposure of an economy to global economic trends. Consequently, assumptions need to be made about the health of the global economy.

We use a fixed threshold to determine if an economy is deemed significantly open. A positive mark is given to the currencies of these countries if global conditions are viewed as favourable and a negative mark if global conditions are seen as unfavourable.

Idiosyncratic factors

Score

A currency’s grade, or score, is obtained by simply taking a equi-weighted average of all the above input.

BRL and RUB score high mark

At present, our scoreboard (see chart) suggests that BRL and RUB are the most attractive currencies among our selection of EM currencies.

The Brazilian real scores highest on most of our metrics given improving economic activity, falling inflation, its attractive valuation, the high carry attached and strong external buffers. The main issue facing the real is politics (i.e. idiosyncratic factors) given the danger that progress on social security reform falters ahead of the October general elections. The Russian rouble also scores highly, mostly given its decent carry and strong external buffer.

Regarding idiosyncratic criteria, current NAFTA negotiations represent a clear and present danger for the Mexican peso, although our view remains that an unilateral withdrawal from NAFTA by the Trump administration remains unlikely given likely opposition from a pro – trade US Congress (see Flash Note). The Turkish lira and South African rand could be weighed down by ongoing political uncertainty. In the case of South Africa, recent positive developments reduce the risk of a Moody’s credit downgrade and have led to a sharp rally in the currency in December (6% in trade – weighted terms). It is also interesting to note that no EM FX in our scorecard has a bad mark, highlighting improvements in the quality of growth, credible central banks (which have helped reduced the risk of high inflation) and stronger external buffers in many emerging markets.

Tags: Brazilian real,Currency drivers,EM currencies,Featured,Macroview,newsletter,Russian rouble