Perspectives Pictet

Perspectives Pictet

[embedded content] Following the Fed’s recent dovish turn, we could expect other central banks to follow suit. However, according to Frederik Ducrozet, Strategist at Pictet Wealth Management, the ongoing trade tensions and idiosyncratic constraints facing central banks today could limit their room to manoeuvre. We expect the European, Japanese and Chinese central banks to contribute to rising global liquidity this year, more than offsetting any quantitative tightening by the Fed.

Read More »Do not hesitate to contact Pictet for an investment proposal. Please contact Zurich Office, the Geneva Office or one of 26 other offices world-wide.

Pictet Perspectives – What to expect from central banks this year

Following the Fed’s recent dovish turn, we could expect other central banks to follow suit. However, according to Frederik Ducrozet, Strategist at Pictet Wealth Management, the ongoing trade tensions and idiosyncratic constraints facing central banks today could limit their room to manoeuvre. We expect the European, Japanese and Chinese central banks to contribute to rising global liquidity this year, more than offsetting any quantitative tightening by the Fed....

Read More »Pictet Perspectives – What to expect from central banks this year

Following the Fed’s recent dovish turn, we could expect other central banks to follow suit. However, according to Frederik Ducrozet, Strategist at Pictet Wealth Management, the ongoing trade tensions and idiosyncratic constraints facing central banks today could limit their room to manoeuvre. We expect the European, Japanese and Chinese central banks to contribute to rising global liquidity this year, more than offsetting any quantitative tightening by the Fed....

Read More »Japan: Q4 GDP disappoints

Japanese economy expands below expectations, while external uncertainties weigh on outlook.Japanese GDP rebounded by 0.3% quarter-on-quarter (q-o-q) in Q4 (1.4% annualised) after contracting by 0.7% q-o-q in Q3 (-2.6% annualised) due to a series of natural disasters over the summer. In year-over-year (y-o-y) terms, output remained virtually unchanged.Domestic demand was the main driving force for the rebound in Q4, while external demand continued to be a drag.A fairly strong domestic capex...

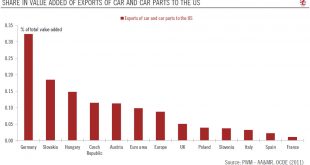

Read More »Euro area : What if car tariffs lie ahead ?

New US auto tariffs may impact the economy significantly more than the previous tariffs on steel and aluminium.Among the key risks for our euro area outlook, the threat of US auto tariffs is of major importance.The US Commerce Department’s investigation on national security threats posed by auto imports is due to be concluded on 17 February.Given the complexity of the global auto supply chain, it is very complicated to isolate the effect of a one-off increase in US tariffs on European...

Read More »Still moderate US inflation

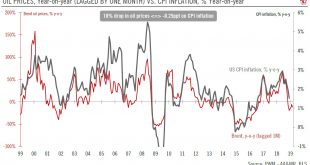

Latest data released confirm our expectations of modest US inflation this year.CPI inflation in January moderated to 1.6% y-o-y, from 1.9% in December (and versus 2.4% on average over the past twelve months).The biggest driver of this moderation was the sharp drop in global oil prices; given recent oil movements, we estimate that headline inflation could slide towards 1% y-o-y in coming months.Excluding energy and food, core CPI inflation remained at 2.2% y-o-y in January.There are signs...

Read More »Reserve Bank of Australia’s upbeat stance turns upside down

Dovish signals on monetary policy reduce upside for the Australian dollar.On 6 February, Philip Lowe, governor of the Reserve Bank of Australia (RBA), sent clear dovish signals, indicating that a rate cut was now as probable as a rate hike. This led to a significant decline in the Australian dollar. This change in the RBA’s stance highlights increasing concerns around the Australian economic outlook.This change in monetary stance mostly reflects increasing concerns over the accumulation of...

Read More »GLOBAL INDICATORS

With further deterioration in the global manufacturing Purchasing Manager's Index (PMI) to 50.7 in January, the global economy is flirting with recession.January’s deterioration in sentiment was widespread, with the notable exception of the US. However, it is possible that January pessimism was largely caused by December’s poor financial markets. If this is indeed the case, it is likely that we will see a bounce in sentiment in the months ahead, following January’s rebound in markets.The...

Read More »Weekly View – May awaits her Valentine

The CIO office's view of the week aheadLast week’s State of the Union speech revealed little news, but President Trump’s conciliatory tone toward bipartisan deal making was apparent, particularly around infrastructure spending and drug prices. In contrast, he remained firm in his stance on China, although with an economic (i.e. trade), rather than geopolitical emphasis. While there is some uncertainty on the future of a US-China trade agreement, especially in the wake of Trump’s cancelled...

Read More »Taking account of regime shifts

Understanding what economic regime we are in and for how long before we transition to a different one is vital for any strategic asset allocation.Predicting the returns for different asset classes is the Holy Grail of asset allocation. The problem is that risk premiums and returns are instable over time. According to our analysis, over the long term (our data stretches back 115 years) there is a 90 percent probability of achieving an annual average return of 8 percent with a 60/40 portfolio....

Read More »