Joseph Y. Calhoun

October 24, 2018

SNB & CHF

Stocks have stumbled into October with the S&P 500 down about 6% as I write this. The source of equity investors’ angst is always hard to pinpoint and this is no exception but this correction doesn’t seem to be due to concerns about economic growth. At least not directly.

The most common explanation for the pullback in stocks – 6% doesn’t even qualify as a correction – is rising interest rates but I think it is a...

Read More »

Charles Hugh Smith

October 23, 2018

SNB & CHF

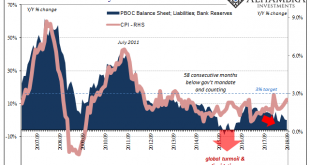

Falling asset inflation plus rising cost inflation equals stagflation.

Inflation is a funny thing: we feel it virtually every day, but we’re told it doesn’t exist—the official inflation rate is around 2.5% over the past few years, a little higher when energy prices are going up and a little lower when energy prices are going down.

Historically, 2.5% is about as low as inflation gets in a mass-consumption economy like...

Read More »

Charles Hugh Smith

October 22, 2018

SNB & CHF

Humiliation and fear of a catastrophic decline in status foment mutiny and rebellion.

I recently finished The Bounty: The True Story of the Mutiny on the Bounty, a painstakingly researched history of the mutiny, but with a focus on how the story was shaped by influential families after the fact to save the life of one mutineer, Peter Haywood, and salvage the reputation of the leader, Fletcher Christian, via a carefully...

Read More »

Charles Hugh Smith

October 21, 2018

SNB & CHF

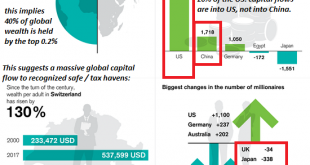

The key here is the gains generated by owning US-denominated assets as the USD appreciates.

Is the Greatest Bull Market Ever finally ending? One straightforward approach to is to follow the money, i.e. global capital flows: assets that attract positive global capital flows will continue rising if demand for the assets exceeds supply, and assets that are being liquidated as capital flees the asset class (i.e. negative...

Read More »

Jeffrey P. Snider

October 20, 2018

SNB & CHF

It was for a time a somewhat curious dilemma. When it rains it pours, they always say, and for China toward the end of 2015 it was a real cloudburst. The Chinese economy was slowing, dangerous deflation developing around an economy captured by an unseen anchor intent on causing havoc and destruction. At the same time, consumer prices were jumping where they could do the most harm.

The Chinese had a pork problem in...

Read More »

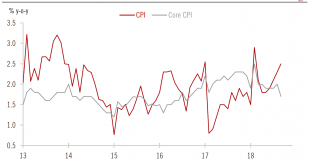

Dong Chen

October 19, 2018

SNB & CHF

Inflation is unlikely to be a constraint on central bank’s policy.

The headline consumer price index (CPI) in China picked up slightly in September, rising by 2.5% year-over-year (y-o-y) compared with 2.3% in August, driven by higher food price and fuel prices. Excluding food and energy, core inflation in China actually eased to 1.7% y-o-y in September from 2.0% in August.

Looking forward, we see some moderate upward...

Read More »

Jeffrey P. Snider

October 18, 2018

SNB & CHF

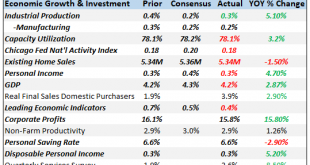

The calendar last month hadn’t yet run out on US Industrial Production as it had for US Retail Sales. The hurricane interruption of 2017 for industry unlike consumer spending extended into last September. Therefore, the base comparison for 2018 is against that artificial low. As such, US IP rose by 5.1% year-over-year last month. That’s the largest gain since 2010.

While that may be, over the last five months American...

Read More »

Jeffrey P. Snider

October 17, 2018

SNB & CHF

The clock really was ticking on this so-called economic boom. A product in many economic accounts of Keynesian-type fantasy, the destructive effects of last year’s hurricanes in sharp contrast to this year’s (which haven’t yet registered a direct hit on a major metropolitan area or areas, as was the case with Harvey and Irma) meant both a temporary rebound birthed by rebuilding as well as an expiration date for those...

Read More »

Charles Hugh Smith

October 16, 2018

SNB & CHF

Here’s the difference between a recession and a depression: you can’t get blood from a stone, or make an insolvent entity solvent with more debt.

There are two basic differences between a recession and a depression:

1. Duration: a recession typically lasts between 6 and 18 months, while a depression drags on for years or even decades, often masked by official propaganda as “slow growth” or “stagnation.”

2. The basic...

Read More »

Charles Hugh Smith

October 15, 2018

SNB & CHF

By the standards of previous generations, the middle class has been stripmined of income, assets and purchasing power.

What does it take to be middle class nowadays? Defining the middle class is a parlor game, with most of the punditry referring to income brackets as the defining factor.

People tend to self-report that they belong to the middle class based on income, but income is not the key metric: 12 other factors...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org