Summary:

By the standards of previous generations, the middle class has been stripmined of income, assets and purchasing power. What does it take to be middle class nowadays? Defining the middle class is a parlor game, with most of the punditry referring to income brackets as the defining factor. People tend to self-report that they belong to the middle class based on income, but income is not the key metric: 12 other factors are more telling measures of middle class membership than income. In Why the Middle Class Is Doomed (April 17, 2012) I listed five minimum threshold characteristics of membership in the middle class: 1. Meaningful healthcare insurance (i.e. not phantom insurance with ,000 deductibles, etc.) and life

Topics:

Charles Hugh Smith considers the following as important: 5) Global Macro, Featured, newsletter, The United States

This could be interesting, too:

By the standards of previous generations, the middle class has been stripmined of income, assets and purchasing power. What does it take to be middle class nowadays? Defining the middle class is a parlor game, with most of the punditry referring to income brackets as the defining factor. People tend to self-report that they belong to the middle class based on income, but income is not the key metric: 12 other factors are more telling measures of middle class membership than income. In Why the Middle Class Is Doomed (April 17, 2012) I listed five minimum threshold characteristics of membership in the middle class: 1. Meaningful healthcare insurance (i.e. not phantom insurance with ,000 deductibles, etc.) and life

Topics:

Charles Hugh Smith considers the following as important: 5) Global Macro, Featured, newsletter, The United States

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

By the standards of previous generations, the middle class has been stripmined of income, assets and purchasing power.

What does it take to be middle class nowadays? Defining the middle class is a parlor game, with most of the punditry referring to income brackets as the defining factor.

People tend to self-report that they belong to the middle class based on income, but income is not the key metric: 12 other factors are more telling measures of middle class membership than income.

In Why the Middle Class Is Doomed (April 17, 2012) I listed five minimum threshold characteristics of membership in the middle class:

1. Meaningful healthcare insurance (i.e. not phantom insurance with $5,000 deductibles, etc.) and life insurance.

2. Significant equity (25%-50%) in a home or equivalent real estate

3. Income/expenses that enable the household to save at least 6% of its income

4. Significant retirement funds: 401Ks, IRAs, etc.

5. The ability to service all debt and expenses over the medium-term if one of the primary household wage-earners lose their job

I then added a taken-for-granted sixth:

6. Reliable vehicles for each wage-earner

Author Chris Sullins suggested adding these additional thresholds:

7. If a household requires government assistance to maintain the family lifestyle, their Middle Class status is in doubt.

8. A percentage of non-paper, non-family home hard assets such as family heirlooms, precious metals, tools, etc. that can be transferred to the next generation, i.e. generational wealth.

9. Ability to invest in offspring (education, extracurricular clubs/training, etc.).

10. Leisure time devoted to the maintenance of physical/spiritual/mental fitness.

Correspondent Mark G. recently suggested two more:

11. Continual accumulation of human and social capital (new skills, networks of collaborators, markets for one’s services, etc.)

And the money shot:

12. Family ownership of income-producing assets such as rental properties, bonds, etc.

The key point of these thresholds is that propping up a precarious illusion of consumption and status signifiers does not qualify as middle class. To qualify as middle class (that is, what was considered middle class a generation or two ago), the household must actually own/control wealth that won’t vanish if the investment bubble du jour pops, and won’t be wiped out by a medical emergency.

In Chris’s phrase, “They should be focusing resources on the next generation and passing on Generational Wealth” as opposed to “keeping up appearances” via aspirational consumption financed with debt.

What does it take in the real world to qualify as middle class?

Here are my calculations based on our own expenses and those of our friends in urban America. We can quibble about details endlessly, so these are mid-range estimates. These reflect urban costs; rural towns/cities will naturally have significantly lower cost structures. Please make adjustments as suits your area or experience, but please recall that tens of millions of people live in high-cost left and right-coast cities, and millions more have high heating/cooling/commuting costs.

The wages of those employed by Corporate America or the government do not reflect the total cost of benefits such as healthcare insurance. Self-employed people like myself pay the full costs of benefits, so we have to realize there is no ideal average of household expenses. Some households pay very little of their actual healthcare expenses, other pay for part of these costs and still others pay most or all of their healthcare insurance and co-pays.

1. Healthcare. Let’s budget $15,000 annually for healthcare insurance. Yes, if you’re 23 years old and single, you will pay less, so this is an average. If you’re older (I’m 64), $15,000 a year only buys you and your spouse stripped down coverage: no eyewear, medication or dental coverage–and that’s if your existing plan is grandfathered in. (If you want non-phantom ObamaCare coverage, the cost zooms up to $2,000/month or $24,000 annually.)

Add in co-pays and out-of-pocket expenses, and the realistic annual total is between $15,000 and $20,000 annually: Your family’s health care costs: $19,393 (this was before ACA).

Let’s say $15,000 annually is about as low as you can reasonably expect to maintain middle class healthcare.

2. Home equity. Building home equity requires paying meaningful principal. Let’s say a household has a 15-year mortgage so the principal payments are actually meaningfully adding to equity, unlike a 30-year mortgage. Let’s say $5-$10,000 of $25,000 in annual mortgage payments is interest (deductible) and $15-$20,000 goes to principal reduction.

3. Savings. Anything less than $5,000 in annual savings is not very meaningful if college costs, co-pays for medical emergencies, etc. are being anticipated, and $10,000 is a more realistic number given the need to stockpile cash in the event of job loss or reduced hours/pay. So let’s go with a minimum of $5,000 in cash savings annually.

4. Retirement. Let’s assume $6,000 per wage earner per year, or $12,000 per household. That won’t buy much of a retirement unless you start at age 25, and even then the return at current rates is so abysmal the nestegg won’t grow faster than inflation unless you take horrendous risks (and win).

5. Vehicles. The AAA pegs the cost of each compact car at $7,000 annually, so $14K per year assumes two compacts each driven 15,000 miles. The cost declines for two paid-for, well-maintained clunkers and increases for sedans and trucks. Let’s assume a scrimp-and-save household who manages to operate and insure two vehicles for $10,000 annually.

6. Social Security and Medicare Taxes. Self-employed people pay full freight Social Security and Medicare taxes: 15.3% of all net income, starting with dollar one and going up to $127,200 for SSA. But let’s take a household of two employed wage-earners and put in $8,000.

Property taxes: These are low in many parts of the country, but let’s assume a level between New Jersey/New York/California level of property tax and very low property tax rates: $10,000 annually.

Income tax: There are too many complexities, so let’s assume $2,000 in state and local taxes and $5,000 in federal taxes for a total of $7,000.

7. Living expenses: Some people spend hundreds of dollars on food each week, others considerably less. Let’s assume a two-adult household will need at least $12,000 annually for food, utilities, phone service, Internet, home maintenance, clothing, furnishings, books, films, etc., while those who like to dine out often, take week-ends away for skiing or equivalent will need more like $20,000.

8. Donations, church tithes, community organizations, adult education, hobbies, etc.: Let’s say $2,000 annually at a minimum.

Note that this does not include the cost of maintaining boats, RVs, pools, etc., or the cost of an annual vacation.

Here’s the annual summary:

Healthcare: $15,000

Mortgage: $25,000

Savings: $5,000

Retirement: $12,000

Vehicles: $10,000

Property taxes: $10,000

Income and Social Security/Medicare taxes: $15,000

Living expenses: $12,000

Other: $2,000

Mortgage: $25,000

Savings: $5,000

Retirement: $12,000

Vehicles: $10,000

Property taxes: $10,000

Income and Social Security/Medicare taxes: $15,000

Living expenses: $12,000

Other: $2,000

Minimum Total: $106,000

Vacations, travel, unexpected expenses, etc: $5,000.

Realistic Total: $111,000

That’s almost double the median household income of $59,000. Note that this $111,000 household income has no budget for lavish vacations, luxury vehicles, large pickup trucks, boats, second homes, college expenses, etc. There is no budget for private schooling. Most of the family income goes to the mortgage, taxes and healthcare. Savings are modest, along with living expenses and retirement contributions. This is a barebones budget.

$111,000 household income is right about the cut-off point for the top 20% of household income. How close are you to the top 1%?

Toss in a jumbo mortgage, college tuition paid in cash, an aging parent to care for or any of a dozen other major expenses and the minimum quickly rises to $155,000, which puts the household in the top 10% of household income.

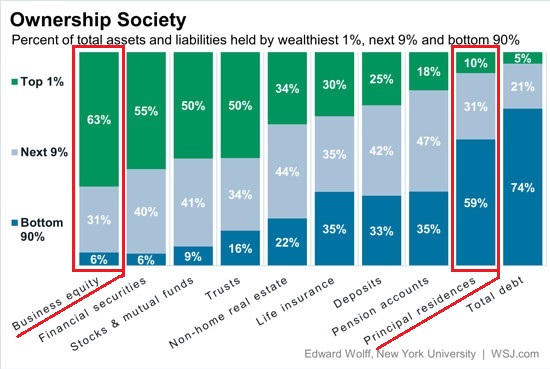

| How can we even talk about a “middle class” when the minimum thresholds put the household in the top 20%? And we haven’t even considered the ultimate minimum threshold of middle class membership: family ownership of income-producing assets such as businesses, rental properties, bonds, etc.The key takeaway of this chart is the concentration of the household wealth of the bottom 90% in the family home. The wealthy and upper-middle class own income-producing assets, while the bottom 90% own some life insurance, cash and pensions, but their largest asset by far is the family home. (They also “own” a tremendous amount of debt.) |

Ownership Society - Click to enlarge |

The problem is life insurance, cash and pensions don’t generate much income, and neither does the family home. Households counting on the equity in bubble-priced housing are not factoring in the unwelcome reality that all bubbles pop, even housing bubbles that can’t possibly pop.

To have the equivalent security and generational wealth enjoyed by the middle class two generations ago, households have to check off all 12 minimum thresholds. I’m not sure there is a “middle class” any more; if we use these 12 minimum thresholds, the U.S. now has a super-wealthy class (top .01%), a very wealthy class (top .5%), an upper class (top 9.5% below the wealthy) and the rest (bottom 90%), with varying levels of security and assets but at levels far below what median-income households enjoyed in bygone eras.

By the standards of previous generations, the middle class has been stripmined of income, assets and purchasing power.

My new book is The Adventures of the Consulting Philosopher: The Disappearance of Drake. For more, please visit the book's website.

Tags: Featured,newsletter