Now it’s the Russian’s fault. Belligerence surrounding Donbas and Ukraine, raw materials and energy supplies to Europe threatened by Putin’s coiled bear. Why wouldn’t markets grow worried? There’s always a reason why we shouldn’t take these things seriously, or quickly dismiss them out of hand as the temporary product of whichever political fear-of-the-day. This isn’t to write that these things aren’t important in any sense; no doubt anyone in or near Ukraine right now would have something powerful to say about these implications. . . When the eurodollar futures curve first inverted back on December 1, it was quickly cast into the same light as oil prices then crashing, each alleged to be a reaction to the sudden appearance of omicron. The successor to

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, currencies, Deflation, economy, eurodollar futures, Featured, Federal Reserve/Monetary Policy, FOMC, inflation, inversion, jay powell, Markets, newsletter, rate hikes, Russia

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Now it’s the Russian’s fault. Belligerence surrounding Donbas and Ukraine, raw materials and energy supplies to Europe threatened by Putin’s coiled bear. Why wouldn’t markets grow worried?

There’s always a reason why we shouldn’t take these things seriously, or quickly dismiss them out of hand as the temporary product of whichever political fear-of-the-day. This isn’t to write that these things aren’t important in any sense; no doubt anyone in or near Ukraine right now would have something powerful to say about these implications. |

. |

. |

|

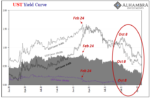

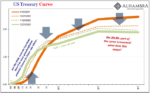

| When the eurodollar futures curve first inverted back on December 1, it was quickly cast into the same light as oil prices then crashing, each alleged to be a reaction to the sudden appearance of omicron. The successor to devilish delta, the new variant was immediately declared the next big potential world-tanking coronavirus disruption.Yet, here we are at almost the end of February, closing in on three months later. Omicron is nearly forgotten, never having come anywhere close to “achieving” its disruptive promise. Eurodollar inversion, on the other hand, it has only gotten more antagonistically uncomfortable as the weeks slide by.

Notable now this week, not Red Russia rather inversion has taken hold of the reds. Remember, the reds are supposed to be Fed and unbroken rate hikes. So, not only is this distortion and upset upsetting for what it means in the world, it is equally in-your-face for the rate hikers at the FOMC facing, they still believe, more inflationary pressures than any others. |

. |

What these chromodynamics mean is a growing perceived likelihood that Powell’s rate hike intentions get spoiled somewhere along the way, and maybe not too far into the otherwise indeterminable stretch of distant future. While Wall Street’s mouthpieces rush to outdo each other forecasting more and more aggressive rate hikes because, they uniformly say, inflation is just out of control, and the public lulled into believing those the only possibilities, the real stuff in the real markets is already wondering just how few the Fed gets done before the “surprise” cut-off.

Not only that, this broadening, deepening inversion is verging on implying the “unthinkable”; that once the FOMC is shaken out of its rate hikes by a starkly different and unavoidable reality, policymakers might even get pressed into, gasp, rate cuts perhaps only a little further on into the time ahead.

But it’s not unthinkable, is it? We just did all this and it wasn’t all that long ago, 2019 barely three years past. The problem, mostly, is hardly anyone knows the details, the markets, or even what truly happened.

Powell’s FOMC right now, today, is setting itself up for that same kind of embarrassing failure. If it comes, it won’t be because of omicron or delta, nor would it be the next Greek letter which will almost certainly speedily enter the public pandemic discourse.

It’s not Russia and Ukraine.

Instead, it’s the same reason why I just wrote a review of what should have already been long forgotten, the Fedwire anniversary.

The absolutely crucial Euro$ futures market is seriously inverted. What must it be thinking? @EmilKalinowski and I ponder the near-term contracts and the still-pretty-near-term contracts that appear to be rejecting the reasoning behind rate hikes.https://t.co/Je7BdoAwrn pic.twitter.com/CXmP65yUrC

— Jeffrey P. Snider (@JeffSnider_AIP) February 23, 2022

The world is always full of geopolitical noise, with the pandemic environment only too fertile from which to harvest a whole bunch more. Remember the North Koreans in 2018 were about to start WW3, before then “trade wars” succeeding in taking over as the primary distraction.

No, it actually takes a whole lot more than the “prospects” for war, war, war to get the curves down and keep them there for this long. That much perfectly consistent, straightforward, and easy to understand once you cover your ears up to filter out all those distracting sounds.

Pity Ukraine, too, there is actually today another kind of red warning spreading over the entire eurodollar’s world.

You Might Also Like

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

2022-01-28

It’s not hard to reason why there continues to be this conflict of interest (rates). On the one hand, impacting the short end of the yield curve, the unemployment rate has taken a tight grip on the FOMC’s limited imagination. The rate hikes are coming and the markets like all mainstream commentary agree that as it stands there’s nothing on the horizon to stop Jay Powell’s hawkishness.

The Hawks Circle Here, The Doves Win There

The Hawks Circle Here, The Doves Win There

2022-01-26

We’ve been here before, near exactly here. On this side of the Pacific Ocean, in the US particularly the situation was said to be just grand. The economy was responding nicely to QE’s 3 and 4 (yes, there were four of them by that point), Federal Reserve Chairman Ben Bernanke had said in the middle of 2013 it was becoming more than enough, creating for him and the FOMC coveted breathing space so as to begin tapering both of those ongoing programs.A full and complete recovery he believed was on schedule if not getting way ahead of it.

Good Time To Go Fish(er)ing Around The Yield Curve

Good Time To Go Fish(er)ing Around The Yield Curve

2022-01-21

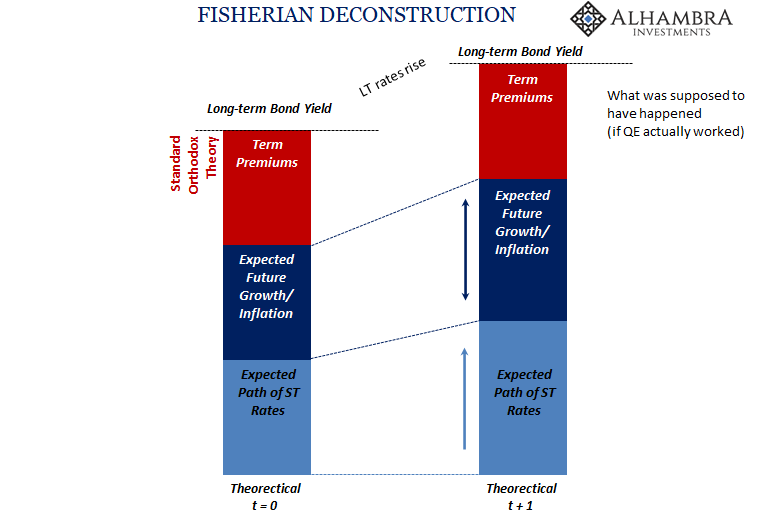

It should be as simple as it sounds. Lower LT UST yields, less growth and inflation. Thus, higher LT UST yields, more growth and inflation. Right? If nominal levels are all there is to it, then simplicity rules the interpretation. Visiting with George Gammon last week, he confessed to committing this sin of omission.

Conflict Of Interest (rates): 10-year Treasury Yield Highest in Almost Two Years

Conflict Of Interest (rates): 10-year Treasury Yield Highest in Almost Two Years

2022-01-12

The dollar was high and going higher. Emerging markets had been seriously complaining. In one, the top central banker for India outright warned, “dollar funding has evaporated.” The TIC data supported his view, with full-blown negative months, net selling from afar that’s historically akin to what was coming out of India and the rest of the world.

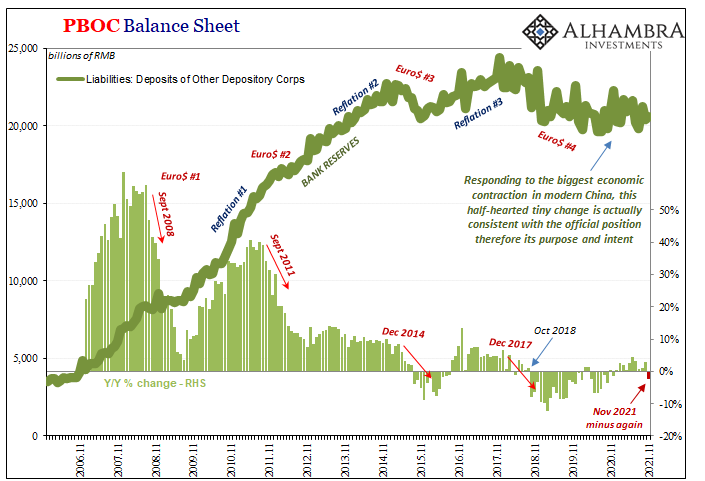

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

2021-12-25

If there is a better, more fitting way to head into the Christmas holiday in the United States than by digging into the finances and monetary flows of the People’s Bank of China, then I just don’t want to know what it is. Contrary to maybe anyone’s rational first impression that this is somehow insane, there’s much we can tell about the state of the world, the whole world and its “dollars”, right from this one key data source.

Start Long With The (long ago) End of Inflation

Start Long With The (long ago) End of Inflation

2021-12-24

With the eurodollar futures curve slightly inverted, the implications of it are somewhat specific to the features of that particular market. And there’s more than enough reason to reasonably suspect this development is more specifically deflationary money than more general economic concerns.

This Is A Big One (no, it’s not clickbait)

This Is A Big One (no, it’s not clickbait)

2021-12-02

Stop me if you’ve heard this before: dollar up for reasons no one can explain; yield curve flattening dramatically resisting the BOND ROUT!!! everyone has said is inevitable; a very hawkish Fed increasingly certain about inflation risks; then, the eurodollar curve inverts which blasts Jay Powell’s dreamland in favor of the proper interpretation, deflation, of those first two.

Short Run TIPS, LT Flat, Basically Awful Real(ity)

Short Run TIPS, LT Flat, Basically Awful Real(ity)

2021-10-28

Over the past week and a half, Treasury has rolled out the CMB’s (cash management bills; like Treasury bills, special issues not otherwise part of the regular debt rotation) one after another: $60 billion 40-day on the 19th; $60 billion 27-day on the 20th; and $40 billion 48-day just yesterday.

Tags: Bonds,currencies,Deflation,economy,eurodollar futures,Featured,Federal Reserve/Monetary Policy,FOMC,inflation,inversion,jay powell,Markets,newsletter,rate hikes,Russia