Last Friday, S&P Global (the merged successor to IHS Markit) reported that its PMI for German manufacturing fell to 54.1. It hadn’t been that low for more than a year and a half. Worse than that, the index for New Orders dropped below 50 for the first time since the middle of 2020. The excuses are plentiful, as there’s COVID, supply problems, Russia, a drop in demand. Wait, what was that last one? The S&P Global Flash Germany Manufacturing PMI fell to 54.1 in April of 2022 from 56.9 in March, below forecasts of 54.1, and pointing to the slowest growth in factory activity since August of 2020 amid reports of severe supply disruption and a drop in demand for goods. emphasis added Since I’ve belated decided to date Euro$ #5 to around May 2021 using various financial

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, Brazil, currencies, economy, Featured, Federal Reserve/Monetary Policy, industrial production, Japan, Markets, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Last Friday, S&P Global (the merged successor to IHS Markit) reported that its PMI for German manufacturing fell to 54.1. It hadn’t been that low for more than a year and a half. Worse than that, the index for New Orders dropped below 50 for the first time since the middle of 2020. The excuses are plentiful, as there’s COVID, supply problems, Russia, a drop in demand.

Wait, what was that last one?

emphasis added Since I’ve belated decided to date Euro$ #5 to around May 2021 using various financial markets, including the euro’s value against the dollar, what about the global economy and its various constituent parts? Quite a lot in it also points to around mid-year last year, particularly in the goods and industrial economy which is more important for #5 than it had been for #4 and the previous others. |

. |

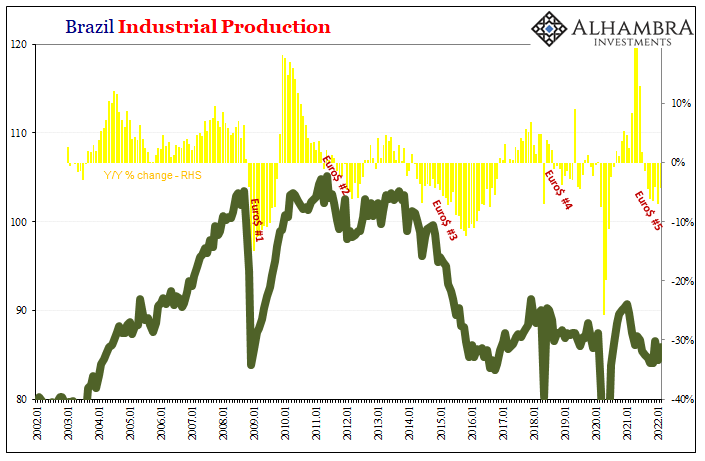

| This is simply because, hopped up on government interference, the goods economy was far and away the biggest contributor to what had been Reflation #4. US consumers, in particular, went crazy online shopping much if not most of which was made then shipped from overseas.

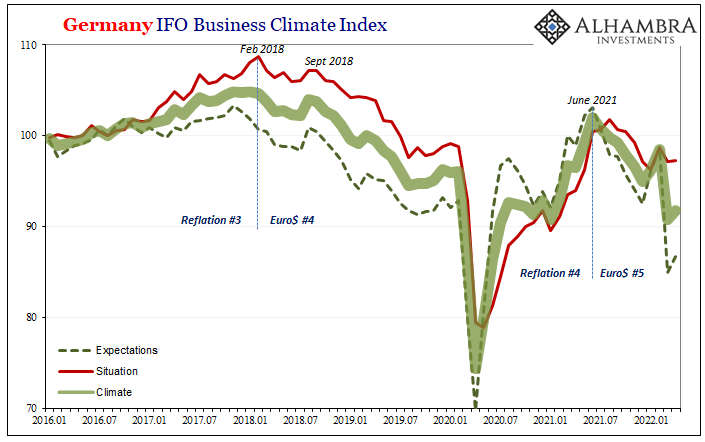

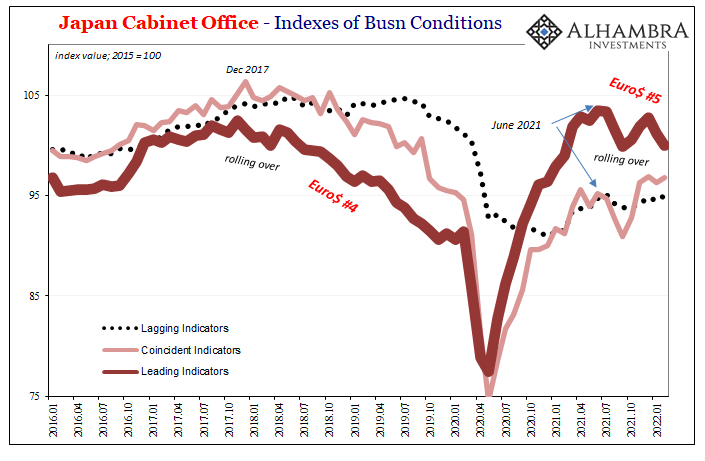

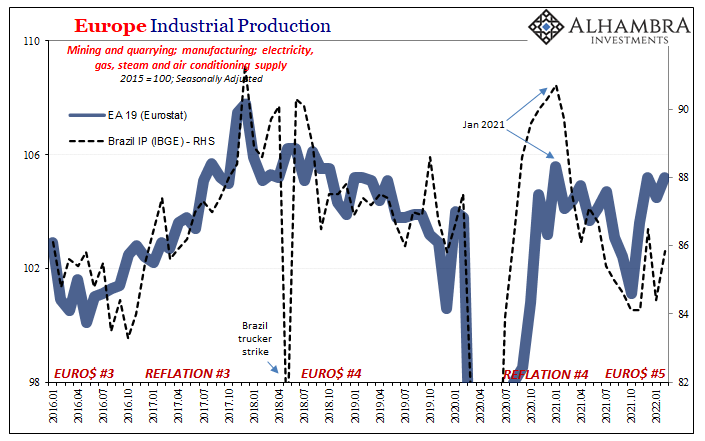

And even then, the price illusion created by transportation inelasticity made it all seem far greater than it ever was. This was also true in the important goods connection between Germany and China. Beginning with Germany, from sentiment to industrial output, the peak registered back around April to June across data and surveys. |

. |

| It’s basically the same story one place to the next with a few exceptions here or there. Very little actual recovery and what was recovered started being lost close to the time market conditions and prices flipped to Euro$ #5.

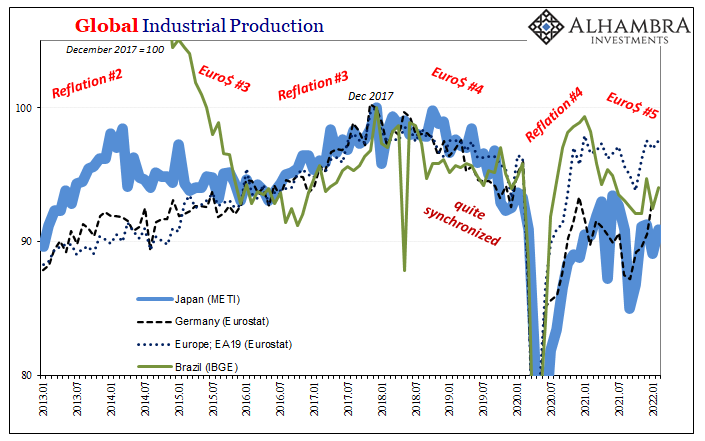

Below is a sample from Germany and Japan as leading indicators, with Brazil thrown in because of the price illusion generating an even larger mistaken impression about its health and contributions to the global economy. Far more bad than good(s), much more consistent with Germany and Japan than not, a Euro$ #5 in the global goods economy which had emerged right when markets said it would. |

. |

. |

|

. |

|

. |

You Might Also Like

Shanghai’s Current Plight Began in 2017

Shanghai’s Current Plight Began in 2017

2022-04-23

The first chapters to China’s new story now playing out in Shanghai were written down in October 2017. Planning for them had begun years earlier, their author Xi Jinping requiring more research before committing them to paper. Communist authorities there had grown increasingly concerned about the lack of growth potential for its political system by then utterly dependent for a quarter-century on the economy growing.

China, Japan, And The Relative Pre-March Euro$ Calm In February

China, Japan, And The Relative Pre-March Euro$ Calm In February

2022-04-22

The month of February 2022, the calm before the latest storm. Russians went into Ukraine toward the month’s end, collateral shortage became scarcity, maybe a run right at February’s final day, and then serious escalations all throughout March – right down to pure US Treasury yield curve inversion.Given that setup, it was unsurprising to find Treasury’s February TIC data mostly unremarkable.

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

2022-04-21

Trust the Fed. Ha! It’s one thing for money dealers to look upon Jay Powell’s stash of bank reserves with remarkable disdain, more immediately damning when effects of the same liquidity premiums in the real economy create serious frictions leaving the entire world exposed to the consequences. When all is said and done, the Federal Reserve has created its own doom-loop from which it won’t likely escape.

China’s Imports Outright Declined In March, And COVID Was The Reason Why But Not Really

China’s Imports Outright Declined In March, And COVID Was The Reason Why But Not Really

2022-04-16

The guy said this was going to be the future. Not just of China, for or really from the rest of the world. Way back in October 2017, at the 19th Communist Party Congress newly-made Emperor Xi Jinping blurted out his grand redesign for Socialism with Chinese Characteristics.

It Wouldn’t Be TIC Without So Much Other

It Wouldn’t Be TIC Without So Much Other

2022-03-23

With the Fed (sadly) taking center stage last week, and market rejections of its rate hikes at the forefront, lost in the drama was January 2022 TIC. Understandable, given all its misunderstood numbers are two months behind at their release. There were some interesting developments regardless, and a couple of longer run parts that deserve some attention.

White-Hot Cycles of Silence

White-Hot Cycles of Silence

2021-12-28

We’re only ever given the two options: the economy is either in recession, or it isn’t. And if “not”, then we’re led to believe it must be in recovery if not outright booming already. These are what Economics says is the business cycle. A full absence of unit roots. No gray areas to explore the sudden arrival of only deeply unsatisfactory “booms.”

The ‘Growth Scare’ Keeps Growing Out Of The Macro (Money) Illusion

The ‘Growth Scare’ Keeps Growing Out Of The Macro (Money) Illusion

2021-11-26

When Japan’s Ministry of Trade, Economy, and Industry (METI) reported earlier in November that Japanese Industrial Production (IP) had plunged again during the month of September 2021, it was so easy to just dismiss the decline as a product of delta COVID.

The Enormously Important Reasons To Revisit The Revisions Already Several Times Revisited

The Enormously Important Reasons To Revisit The Revisions Already Several Times Revisited

2021-10-29

Extraordinary times call for extraordinary commitment. I never set out nor imagined that a quarter century after embarking on what I thought would be a career managing portfolios, researching markets, and picking investments, I’d instead have to spend a good amount of my time in the future taking apart how raw economic data is collected, tabulated, and then disseminated.

Tags: Bonds,Brazil,currencies,economy,Featured,Federal Reserve/Monetary Policy,industrial production,Japan,Markets,newsletter