Shipping container rates have been dropping since early March – right around the time when we had just experienced our “collateral days” and then stood by to witness chaotic financial fireworks, inversions, the whole thing. The bane of the logistical supply-side snafu-ing, it has been container redistribution mucking the goods economy up.The recent and sharp decline in container rates, according to Freightos, is because China’s been closed down by Xi’s pursuit of his madman persona. With Shanghai locked up, freight just hasn’t been able to move. In the meantime, with manufacturing still restricted, transpacific ocean rates continued to fall. Asia – US West Coast rates fell 18% this week to ,455/FEU and are 28% lower than at the start of the lockdown in late

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, China, commodities, Crude Oil, currencies, economy, Featured, Federal Reserve/Monetary Policy, gasoline, Inventory, Markets, newsletter, Oil, oil production, WTI, wti futures curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Shipping container rates have been dropping since early March – right around the time when we had just experienced our “collateral days” and then stood by to witness chaotic financial fireworks, inversions, the whole thing. The bane of the logistical supply-side snafu-ing, it has been container redistribution mucking the goods economy up.The recent and sharp decline in container rates, according to Freightos, is because China’s been closed down by Xi’s pursuit of his madman persona. With Shanghai locked up, freight just hasn’t been able to move.

Asia – US West Coast rates fell 18% this week to $11,455/FEU and are 28% lower than at the start of the lockdown in late March. Though this sounds suspiciously more like a demand problem than one of supply restriction, shippers confidently expect a (short run) rebound in container rates as the Chinese loosen up and let goods flow again; “Most in the industry are expecting pent up demand to send a surge of ocean exports towards destination ports like LA/Long Beach when manufacturing in Shanghai rebounds.” If this was true, why wouldn’t container rates be rising already? |

. |

| Here’s a thought: what if retailers and wholesalers in the US have instead used the Shanghai mess to just cancel orders? Hey, since you all are closed anyway, just don’t bother. Save us the fuss.

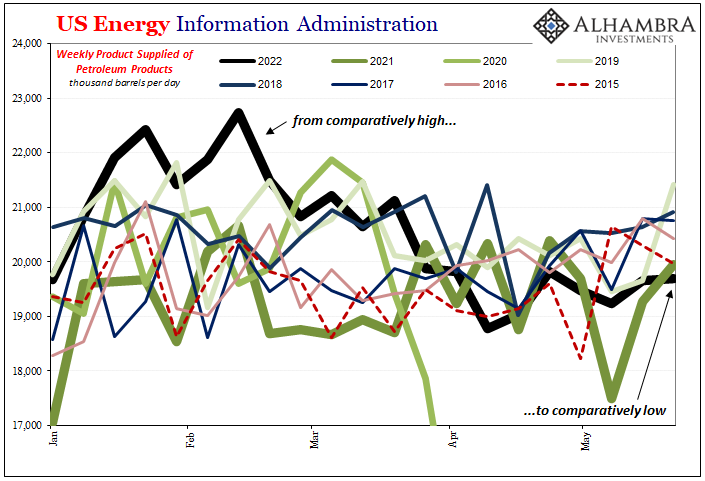

We all heard from Target and Walmart about consumers. They aren’t buying much high value stuff at least not from these big boxers, though anecdotes are spreading among other retailers, too. In fact, maybe the biggest story when it comes to specifically US demand (though it’s not different in Europe, Japan, or the rest of Asia) is its ongoing, very open destruction. High gasoline prices have recently gone higher still, a new record this week, even as Americans have already substantially scaled back driving (and also transporting goods, as well as people). According to the US Energy Information Administration, gasoline “supplied” (an industry term for how much the energy sector supplied to satisfy actual user demand) remained at its lowest level since 2013 for this time of year. This is supposed to be the start of peak driving season, and so far of May 2022 only May 2020 experienced less gasoline demand. As you can see below, the amount supplied should have started higher by now, only it hasn’t this year; the deviation has only gotten worse. With gasoline predicted to continue rising, demand will only be more suspect going forward. The same is true of all petroleum products, too. |

. |

. |

|

. |

|

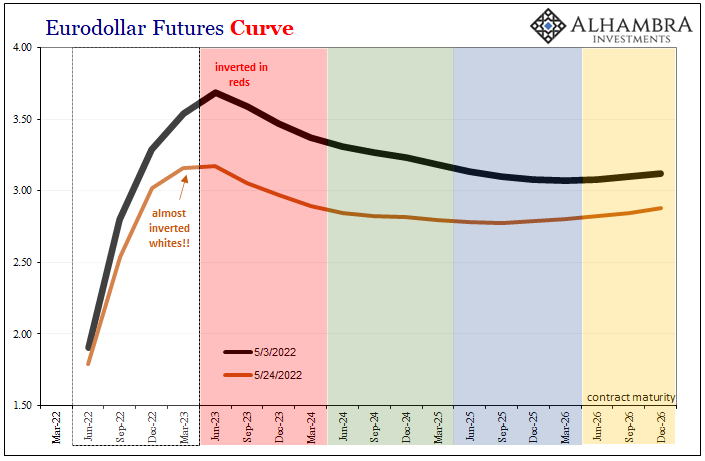

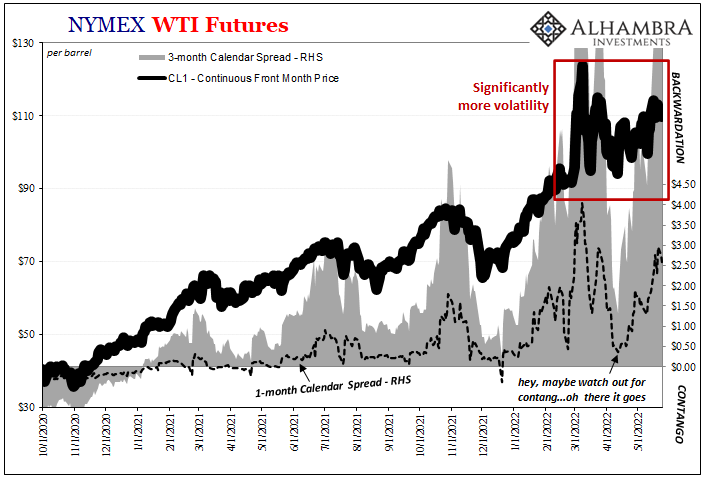

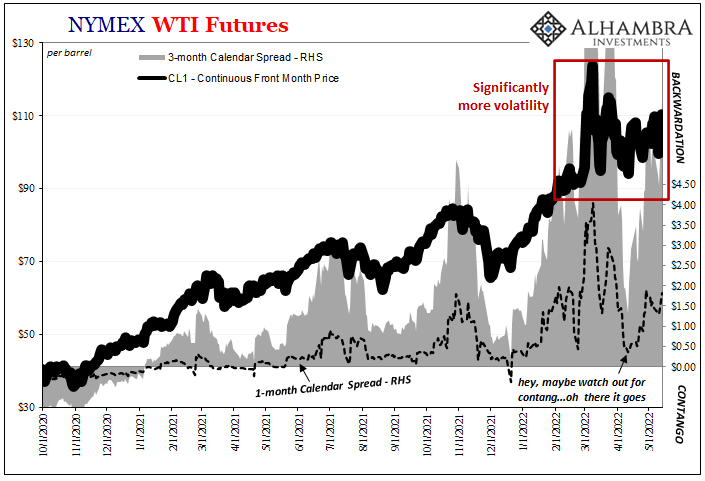

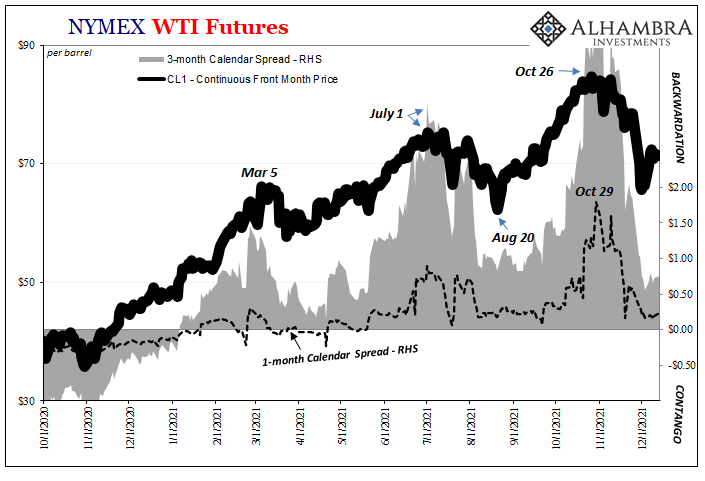

| So far as the market for crude oil is concerned, none of this appears to be concerning in it. Prices remain very firm, and the WTI futures curve as steep in backwardation as ever. For however questionable demand has become, or might still become, attention remains fixed upon lack of supply – amplified by the ever-present Russian threat to cut off energy from Europe, thereby stripping global markets of even more product.

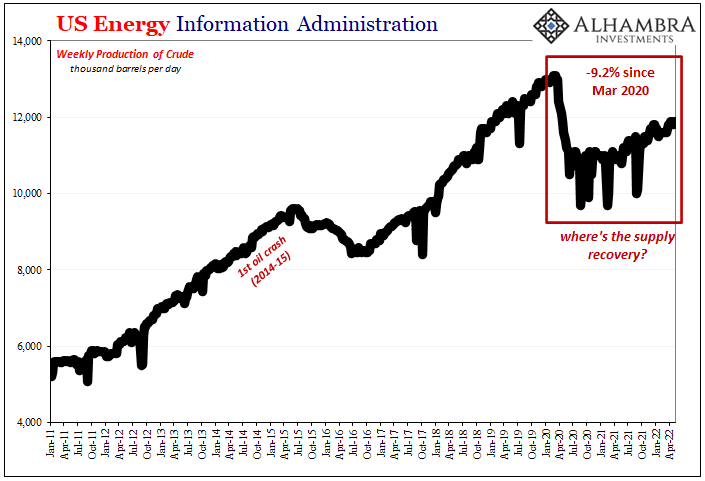

As it is here in the US, despite dropping demand, crude and gasoline stocks are even lower. Therefore, prices and curve steepness. |

. |

. |

|

. |

|

. |

|

| But if we’re thinking beyond strictly oil prices and the oil market, it is this key measure of falling demand that should headline all commentary. There is a reason why the rest of financial (and money) markets are positioning the way they have.

Rate hike rejection is all about the potential for a global drop-off way beyond mere domestic gasoline or oil usage. If Americans suddenly can’t drive as much, then, like Target and Walmart have reported, they aren’t buying as much leaving the goods economy already bloated with increasingly scarce storage capacity (warehouse availability is at a record low already) and no need to make and ship more of the same from China. |

. |

. |

|

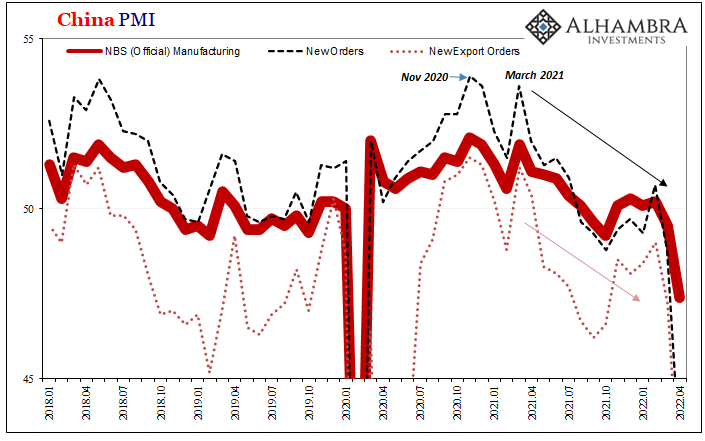

Freight rates just might be coming down, maybe staying down this time because oversaturated US traders have used the Shanghai fiasco to begin adjusting their own supply chain stuffing. And if you’re already moving to cancel China, maybe give the Japanese or European a call, too. Forget it, Japan Inc. We’re all filled up here, European manufacturer. The bullwhip does work in various ways, in addition to inventory liquidations. We’ll have more inventory data tomorrow with the release of the advanced wholesale inventory figures (expected to show another +2% m/m increase). When you look at the various Chinese PMIs, for example, the plunge in new orders especially among export orders is at least consistent with that idea. According to China’s NBS, the New Export Order index for its Manufacturing survey crashed to 41.6 in April (from already falling pre-lockdown 47.2 in March, down from 49.0 in February). It isn’t expected to rebound much for May (we won’t know until the data is released next week). Again, lockdowns are blamed. Maybe it’s all just being demanded. |

. |

You Might Also Like

Crude Contradictions Therefore Uncertainty And Big Volatility

Crude Contradictions Therefore Uncertainty And Big Volatility

2022-05-18

This one took some real, well, talent. It was late morning on April 11, the crude oil market was in some distress. The price was falling faster, already down sharply over just the preceding two weeks. Going from $115 per barrel to suddenly less than $95, there was some real fear there.But what really caught my attention was the flattening WTI futures curve.

Industrial Synchronized Demand

Industrial Synchronized Demand

2022-05-11

Are the industrial commodities starting to get a whiff of demand side rejection? Short run trends suggest that this could be the case. From copper to iron and the highest (formerly) of the high flyers, aluminum, this particular group has been exhibiting a rather synchronized setback going back to the end of March, start of April.

Weekly Market Pulse: Welcome Back To The Old Normal

Weekly Market Pulse: Welcome Back To The Old Normal

2022-05-03

Stagflation. It’s a word that strikes fear in the hearts of investors, one that evokes memories – for some of us – of bell bottoms, disco, and Jimmy Carter’s American malaise. The combination of weak growth and high inflation is the worst of all worlds, one that required a transformational leader and a cigar-chomping central banker to defeat the last time it came around.

Not Good Goods

Not Good Goods

2022-04-24

The goods economy in the United States is – maybe was – the lone economic bright spot. That in and of itself should’ve provoked more caution, instead there was the red-hot recovery to sell under the cover of supply shock pricing changes. The sheer spending on goods, and how they arrived, each unabashedly artificial from the get-go.

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

2022-04-21

Trust the Fed. Ha! It’s one thing for money dealers to look upon Jay Powell’s stash of bank reserves with remarkable disdain, more immediately damning when effects of the same liquidity premiums in the real economy create serious frictions leaving the entire world exposed to the consequences. When all is said and done, the Federal Reserve has created its own doom-loop from which it won’t likely escape.

China More and More Beyond ‘Inflation’

China More and More Beyond ‘Inflation’

2022-04-17

If only the rest of the world could have such problems. Chinese consumer prices were flat from February 2022 to March, even though gasoline and energy costs predictably skyrocketed. According to China’s NBS, gas was up 7.2% month-over-month while diesel costs on average gained 7.8%.

Playing Dominoes

Playing Dominoes

2021-12-19

That was fast. Just yesterday I said watch out for when the oil curve flips from backwardation to contango. When it does, that’s not a good sign. Generally speaking, it means something has changed with regard to future expectations, at least one of demand, supply, or also money/liquidity.

Weekly Market Pulse: Discounting The Future

Weekly Market Pulse: Discounting The Future

2021-12-07

The economic news recently has been better than expected and in most cases just pretty darn good. That isn’t true on a global basis as Europe continues to experience a pretty sluggish recovery from COVID. And China is busy shooting itself in the foot as Xi pursues the re-Maoing of Chinese society, damn the economic costs.

Tags: Bonds,China,commodities,Crude Oil,currencies,economy,Featured,Federal Reserve/Monetary Policy,gasoline,Inventory,Markets,newsletter,OIL,oil production,WTI,wti futures curve