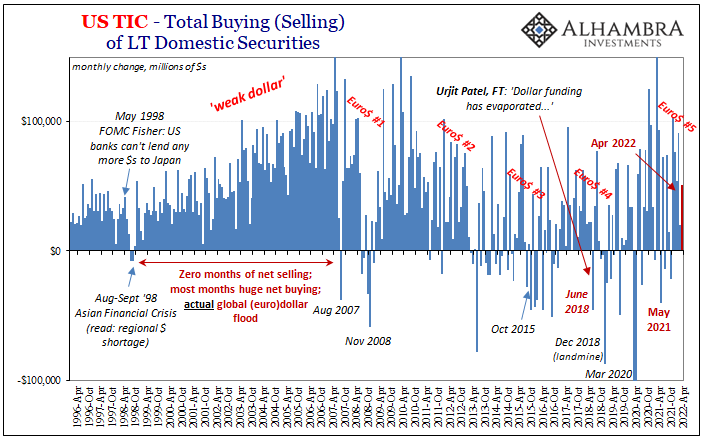

If the March gasoline/oil spike hit a weak global economy really hard and caused what more and more looks like a recessionary shock, a(n un)healthy part of it was the acceleration of Euro$ #5 concurrently rippling through the global reserve system. This much was apparent right from the start, with financial markets gone haywire three months ago (mid-March seasonal bottleneck), and then more of the same into April right to now. The updated TIC data for the month of April is everything we already expected, including the usual after-the-fact corroboration of the situation displayed to us in real-time by market performance. The stand-outs were definitely Japan and China, both JPY and CNY together careening towards the eurodollar, global recession risk abyss. Before

Topics:

Jeffrey P. Snider considers the following as important: $CNY, 5.) Alhambra Investments, bonds, China, currencies, economy, eurodollar system, Featured, Federal Reserve/Monetary Policy, global dollar shortage, Japan, JPY, Markets, newsletter, tic

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| If the March gasoline/oil spike hit a weak global economy really hard and caused what more and more looks like a recessionary shock, a(n un)healthy part of it was the acceleration of Euro$ #5 concurrently rippling through the global reserve system. This much was apparent right from the start, with financial markets gone haywire three months ago (mid-March seasonal bottleneck), and then more of the same into April right to now.

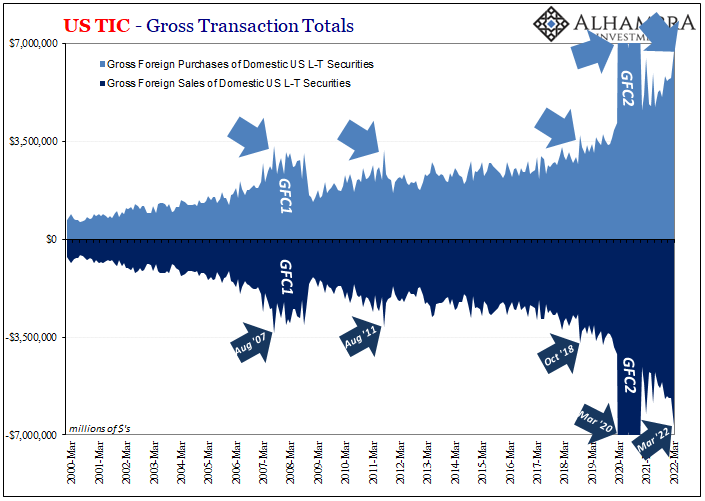

The updated TIC data for the month of April is everything we already expected, including the usual after-the-fact corroboration of the situation displayed to us in real-time by market performance. The stand-outs were definitely Japan and China, both JPY and CNY together careening towards the eurodollar, global recession risk abyss. Before those, first the usual overlay. |

. |

| Official institutions selling USTs (not because they hate America, or even as UST prices were falling), and US banks liabilities to be laid out overseas decelerated even further to their lowest cumulative point since last March (with a negative for this April).

Both those being key warning signs about escalating global dollar shortage. |

. |

. |

|

. |

|

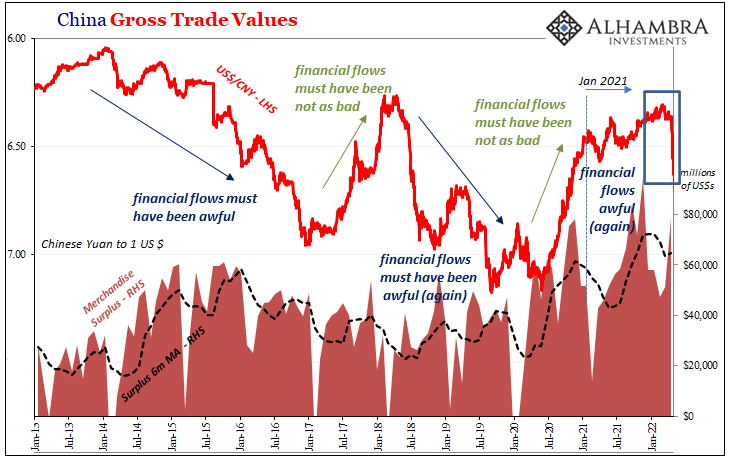

| Against that backdrop, yeah, plummeting CNY and JPY. According to TIC, government efforts in each those places were ramped way up attempting to address what can only have been a rampaging (likely collateral-disrupted) funding environment across much of Asia.

Blame will fall on Xi’s reckless shanghai of Shanghai, but as should become more apparent as more time goes by and with more data confirming this is globally synchronized in all the familiar if unwelcome eurodollar ways; not COVID no matter how much Zero-COVID might get applied even in key global places like China’s industrialized East. The TIC figures now released are as striking as the drop in each currency had been when taking place. |

. |

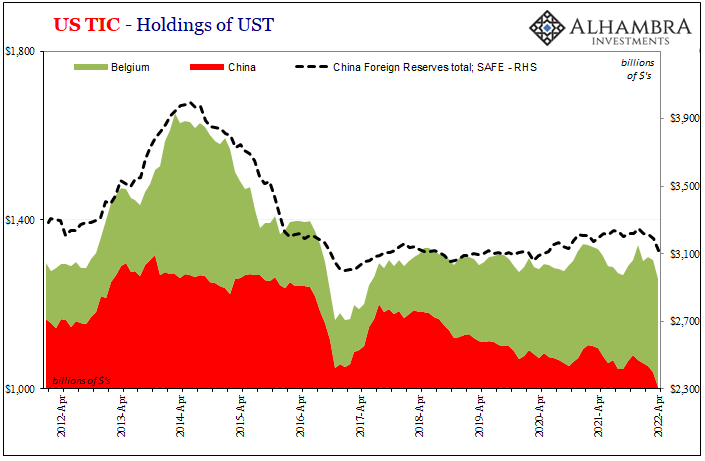

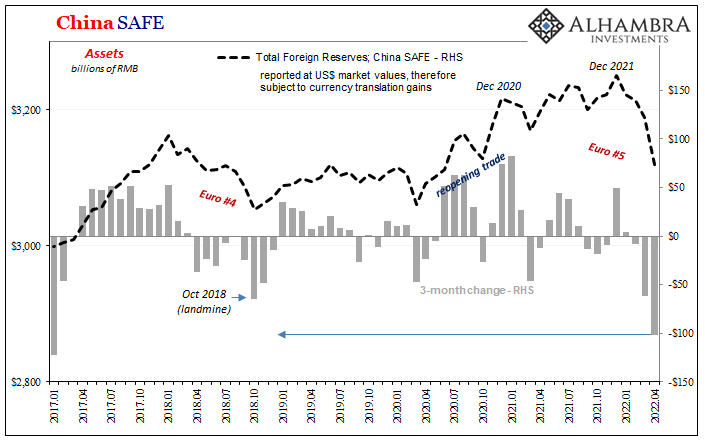

| Taking Mainland China first, registered holdings of USTs fell to just barely more than $1 trillion, down by $36.2 billion in April alone to the lowest reported balance in well over a decade.

There was also a substantial decline in USTs reported for Belgium, almost $10 billion, which we associate with China for very good reasons (see: below China/Belgium TIC charted against SAFE). This was a combined $45.1 billion just in April which goes right along with the equally significant reduction in SAFE holdings reported from China – and, of course, CNY’s near-crash. |

. |

. |

|

. |

|

. |

|

. |

|

| It’s worth reiterating what’s demonstrated (conclusively) by this data, beginning with the fact that China’s yuan isn’t being purposefully “devalued” as a matter of policy, rather the Chinese commercial and financial requirements are being stripped of “dollars” as a function of this increasingly difficult and dangerous Euro$ #5.

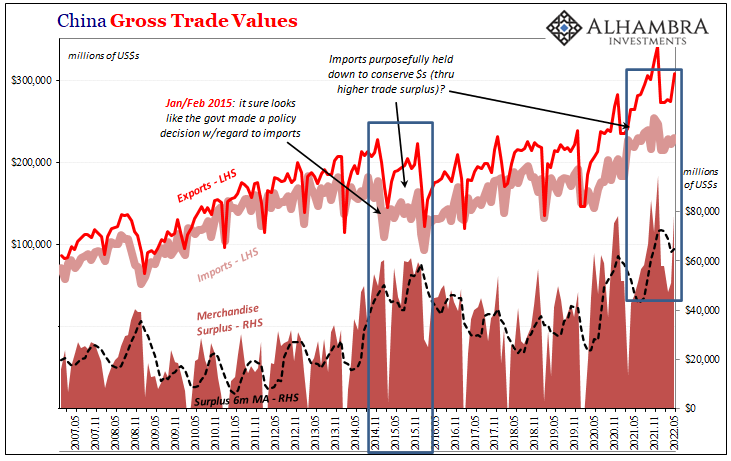

While China continues to enjoy record and near-record merchandise trade surpluses, therefore a surplus of “dollars” from it, the reason they aren’t and haven’t been able to literally bank those surpluses is what you see above – the negative financial eurodollar flows had to have been so much worse (which we already knew, just more corroboration from here an American source). |

. |

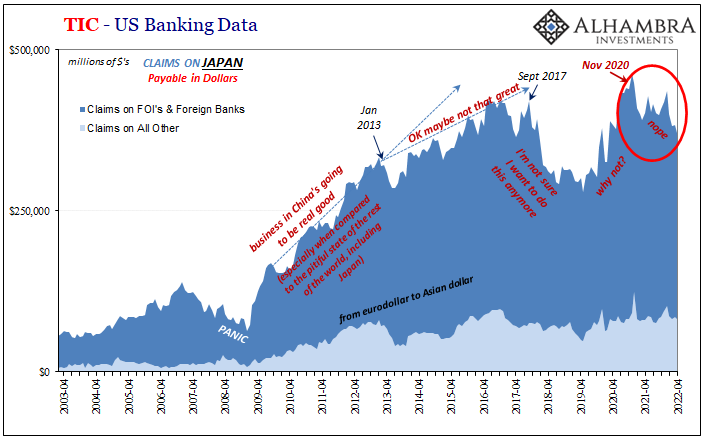

| The implications, obviously, extend far beyond Beijing’s limited reach and capacity to affect CNY’s trajectory therefore China’s quite perilous monetary condition (despite conventional thinking totally contrary; we’re constantly led to believe there is no more effective, nearly omniscient technocratic ideal than the CCP’s PBOC which performs far more like the hapless bureaucrats at the Fed in just being along for what is always the eurodollar’s ride).

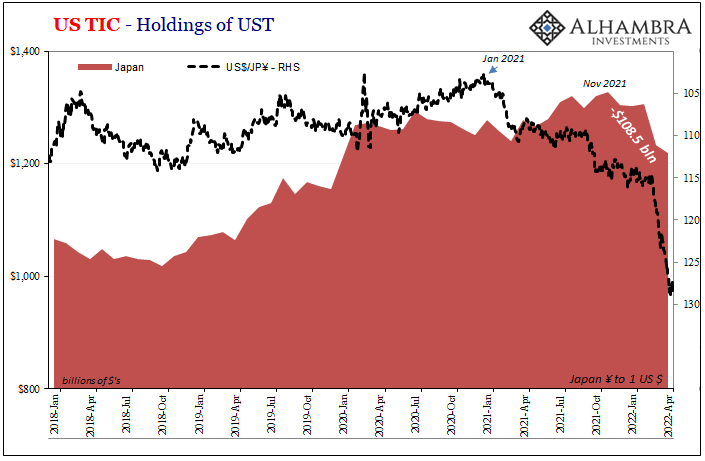

In this case, the wreckage has extended to China’s primary eurodollar benefactors located in Japan. This sort of contagious baby-out-with-the-bathwater behavior by the global eurodollar system had become more apparent during the earlier stages of Euro$ #4, now taken to new extremes for reasons that I think relate to Japan’s own increasingly perilous situation (see: paying 40% more for 10% fewer imports of food and fuel). Japan has its own serious problems in addition to its major financial institutions being so closely linked to risky, unrewarding China by redistributing much toward the Chinese dollar short. For April TIC data, registered UST holdings in Tokyo fell again after March’s big plunge. |

. |

|

. |

| https://t.co/Ll8vCoF2XU— Jeffrey P. Snider (@JeffSnider_AIP) April 29, 2022

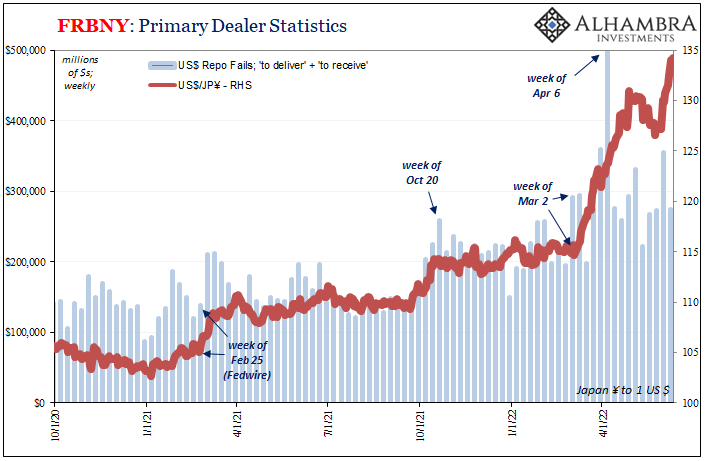

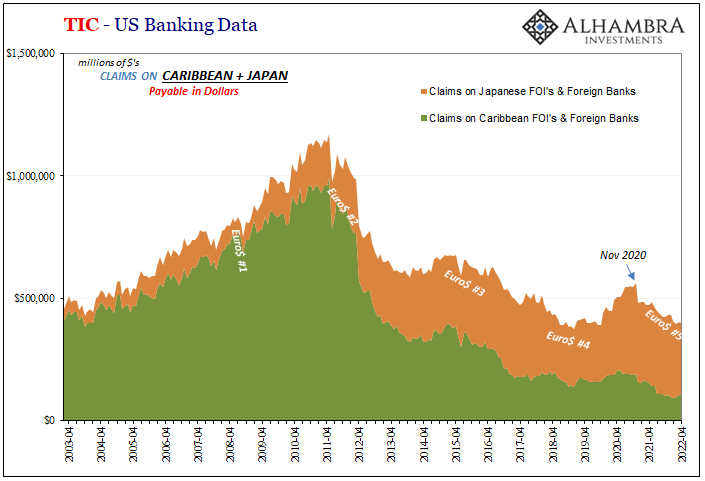

Because of this rather unique situation, eurodollars via Tokyo on their way to Shanghai, and the potential (though hidden therefore unable to be confirmed yet easily and reasonably suspected) for widespread, tortuous use of collateral-for-collateral swaps underpinning much of it, the last few years have seen a close(r) correlation between implied collateral availability (repo fails) and JPY’s own fate. We need only be reminded of this growing fragility by the Bank of Japan’s rather absurd “collateral pool” created during 2016’s Euro$ #3 debacle (which obviously didn’t help in the long run, as anyone with common sense might’ve long ago guessed). In terms of overall bank liabilities beside collateral, US banks appear to be lending less to their Japanese counterparts, directly by increasing the costs of funding when charging higher rates or indirectly by demanding more (or better) collateral. April recorded another large decline of US bank liabilities extended to Japan (below). This, however, not a new development rather one that has accelerated since, drum roll, last December when the eurodollar futures curve first inverted and swap spreads detoured toward the exact wrong direction (from inflation and rate hikes). |

. |

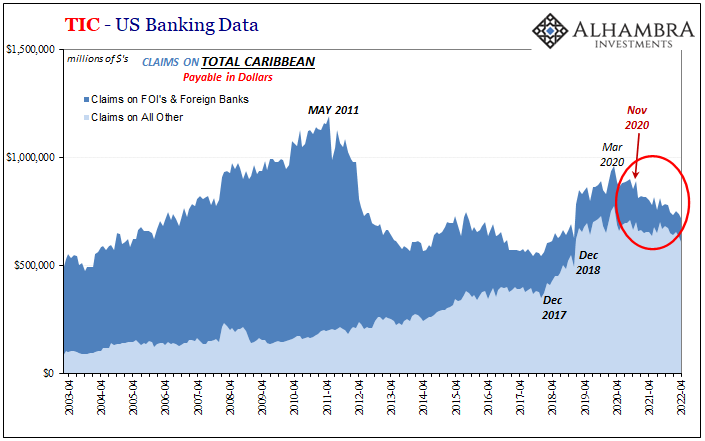

| What’s interesting is how much of a correlation there now seems to be between this type of eurodollar retrenchment between US banks and the Japanese and the same between US banks and those located in Emil Kalinowski’s current homeland in the Caribbean.

TIC-indicated dollar activity to both of those very different places dropped sharply during the month of April. American bank liabilities reported to the Caribbean are way down, -11% year-over-year, updated at just $716.9 billion being the lowest since December 2018 (and might actually be worse given data and discontinuity issues regarding CLOs). |

. |

| Bank liabilities to Japan are the worst since February 2020. |

. |

. |

|

| None of this is, or indicates, genuine inflation. Quite the contrary, all these same familiar symptoms are clear signs of deflationary money that has been working through the global system for quite a long time already to have now (in April) reached these accelerating, recession-inducing proportions storming across the world.

Since the eurodollar way of doing financial and commercial business means globally synchronized, we’re not just dealing with a global dollar shortage that’s a financial and economic burden and reduction for the global economy outside the US, up-to-date economic data like the current state of financial markets pretty clearly shows the domestic side already greatly affected by the gathering storm. It was never delta or omicron, as many tried to claim, and it isn’t the Fed’s rate hikes or Russia’s misadventures (though that really hasn’t helped and may have been the final straw). Currencies aren’t being purposefully devalued. Foreigners are being forced to sell USTs, not ditching them voluntarily because they worry over a dollar crash that never happens, and sure isn’t happening right now. This remains the eurodollar’s world, and we are all – everyone everywhere – trying to live in it. Since March and April, it’s become a whole lot more difficult. If you hadn’t already noticed. |

. |

You Might Also Like

Looking Back At Chaotic March Through TIC

Looking Back At Chaotic March Through TIC

2022-05-20

March ended up being a pretty wild ride. Lost amidst the furor over Russia’s invasion of Ukraine, the month began with a couple clear “collateral days. T-bill rates along with repo fails echoed that same shortfall before the yield curve then joined the eurodollar futures curve being inverted.

Industrial Synchronized Demand

Industrial Synchronized Demand

2022-05-11

Are the industrial commodities starting to get a whiff of demand side rejection? Short run trends suggest that this could be the case. From copper to iron and the highest (formerly) of the high flyers, aluminum, this particular group has been exhibiting a rather synchronized setback going back to the end of March, start of April.

CNY’s Drop Wasn’t ‘Devaluation’ in ’15 nor ’18, and It Isn’t ‘Devaluation’ Now

CNY’s Drop Wasn’t ‘Devaluation’ in ’15 nor ’18, and It Isn’t ‘Devaluation’ Now

2022-04-25

For one thing, that whole Bretton Woods 3 thing is really off to an interesting start. And by interesting, I mean predictably backward. According to its loud and leading proponent, China’s yuan was supposed to be ascending while the dollar sank, its first step toward what many still claim will end up in some biblical-like abyss.

The (less) Dollars Behind Xi’s Shanghai of Shanghai

The (less) Dollars Behind Xi’s Shanghai of Shanghai

2022-04-25

What everyone is saying, because it’s convenient, is that China’s zero-COVID policies are going to harm the economy. No. Economic harm of the past is the reason for the zero-COVID policies. As I showed yesterday, the cracking down didn’t just show up around 2020, begun right out in the open years beforehand, born from the scattering ashes of globally synchronized growth.

China, Japan, And The Relative Pre-March Euro$ Calm In February

China, Japan, And The Relative Pre-March Euro$ Calm In February

2022-04-22

The month of February 2022, the calm before the latest storm. Russians went into Ukraine toward the month’s end, collateral shortage became scarcity, maybe a run right at February’s final day, and then serious escalations all throughout March – right down to pure US Treasury yield curve inversion.Given that setup, it was unsurprising to find Treasury’s February TIC data mostly unremarkable.

China More and More Beyond ‘Inflation’

China More and More Beyond ‘Inflation’

2022-04-17

If only the rest of the world could have such problems. Chinese consumer prices were flat from February 2022 to March, even though gasoline and energy costs predictably skyrocketed. According to China’s NBS, gas was up 7.2% month-over-month while diesel costs on average gained 7.8%.

It Wouldn’t Be TIC Without So Much Other

It Wouldn’t Be TIC Without So Much Other

2022-03-23

With the Fed (sadly) taking center stage last week, and market rejections of its rate hikes at the forefront, lost in the drama was January 2022 TIC. Understandable, given all its misunderstood numbers are two months behind at their release. There were some interesting developments regardless, and a couple of longer run parts that deserve some attention.

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)

2022-01-14

A full part of the inflation hysteria, the first one, was the dollar’s looming crash. The currency was, too many claimed, on the verge of collapse by late 2017, heading downward and besieged on multiple fronts by economics and politics alike.

Tags: $CNY,$JPY,Bonds,China,currencies,economy,eurodollar system,Featured,Federal Reserve/Monetary Policy,global dollar shortage,Japan,Markets,newsletter,tic