You don’t have to take my word for it. QE doesn’t work and it never has. That’s not just my assessment, pull out any chart of interest rates for wherever gets the misfortune of having been wasted with one of these LSAP’s. If none handy, then just read what officials and central bankers write about their own programs (or those of their close and affectionate counterparts). After nearly a decade of Abenomics in Japan, the latest Japanese Prime Minister Fumio Kishida is publicly expressing his desire to move on from it. Run away at all speed. Of its purported three arrows, the Bank of Japan’s QQE was by far its biggest – in theory. . So much “money printing”, even Paul Krugman had been impressed. In practice, it always ends up with something different. Kishida is

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, Abenomics, bank loans, Bank of Japan, bonds, currencies, economy, EuroDollar, Featured, Federal Reserve/Monetary Policy, inflation, inflation expectations, interest rate fallacy, Interest rates, Japan, lending, Markets, money creation, money printing, newsletter, QQE

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| You don’t have to take my word for it. QE doesn’t work and it never has. That’s not just my assessment, pull out any chart of interest rates for wherever gets the misfortune of having been wasted with one of these LSAP’s. If none handy, then just read what officials and central bankers write about their own programs (or those of their close and affectionate counterparts).

After nearly a decade of Abenomics in Japan, the latest Japanese Prime Minister Fumio Kishida is publicly expressing his desire to move on from it. Run away at all speed. Of its purported three arrows, the Bank of Japan’s QQE was by far its biggest – in theory. |

. |

| So much “money printing”, even Paul Krugman had been impressed.

In practice, it always ends up with something different. Kishida is only somewhat guarded in his criticism, unusual for Japanese politicians particularly from the same party (Abe resigned a year ago for “health reasons”). Speaking with the Financial Times just last week, the new leader wants little to do with QQE and the rest, because it worked out well? No.

Kishida claims QQE and Abenomics achieved something for the real economy, though not much “trickled down” beyond certainly stocks moving up, leaving the vast majority with questions. Where’s the full recovery inflation, he didn’t need to ask. |

. |

|

QE is thought to work in a combination of the three ways money would influence if money was to be introduced: portfolio rebalancing, lowering interest rates, and emotional manipulation. |

. |

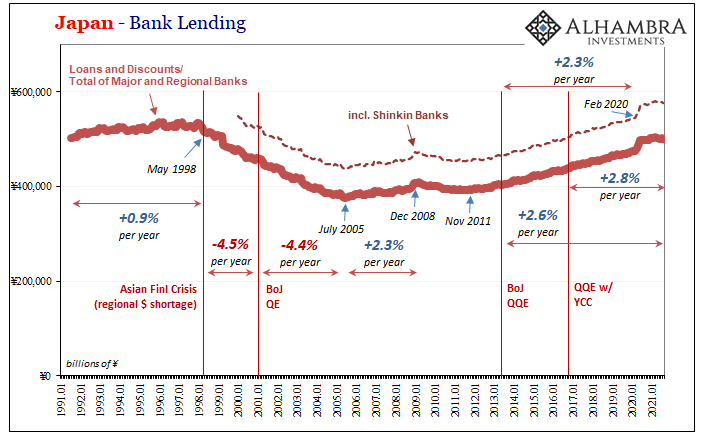

| The first, rebalancing, refers to buying bonds or other assets from banks forcing them to replace what was purchased by the central bank with other risky activities, in particular lending.

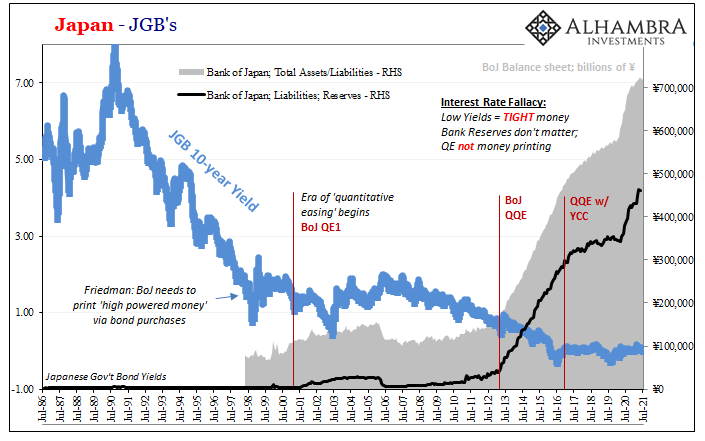

Nope. Japan is the perfect, absolutely perfect example of how this channel consistently fails (though US and European banks are no slouches when destroying the rebalancing theory, either). How about interest rates? Nothing here, either. Again, just pull out a rate chart in any jurisdiction where QE bond buying is active and then not. More often than not, yields behave in the opposite way from how they “should.” The market, not QE, always sets rates no matter how many bonds are purchased by the central bank for however long. Low interest rates don’t even mean what the theory proposes (interest rate fallacy). Sentiment? Nothing here, either. A recent screed written up at the Federal Reserve Bank of New York, flagged expertly by Emil Kalinowski, simply categorizes and attempts to compartmentalize what we already know.

Translation: don’t worry about 1970’s style Great Inflation beginning 2022, whenever central banks do QE no matter how big or how long these things can barely if ever achieve even small levels of inflation. |

. |

| The data and evidence overwhelming, central bankers themselves and now politicians having to concede on all three grounds.

Where I can help is in deconstructing how and why QE fails. It begins with a fatal conceit (same FRBNY post):

There’s a single word buried in that question which just doesn’t belong. |

. |

| Friedman said and history proves it over and over: inflation is always and everywhere a monetary phenomenon. QE doesn’t ever lead to inflation (or much by way of growth), it can’t even achieve tangible action through even a single of its channels, therefore…

We can safely eliminate central bank “money printing” from the “inflation” of 2021, and you don’t have to take my word for it. Expect these types of refutations to increase in number and noise (it only took twenty years). This can only mean consumer prices this year have been affected by non-inflation factors, such as these. And if it is non-economic, non-monetary, it isn’t inflation therefore it can’t continue nor spiral into some Great Inflation 2.0 or, for some, Weimar 2.0 and the long-predicted dollar wipeout. On the contrary, the world’s real money is – right now – being unusually unambiguous about something else entirely. |

. |

You Might Also Like

Weekly Market Pulse: Inflation Scare!

Weekly Market Pulse: Inflation Scare!

2021-10-25

The S&P 500 and Dow Jones Industrial stock averages made new all time highs last week as bonds sold off, the 10 year Treasury note yield briefly breaking above 1.7% before a pretty good sized rally Friday brought the yield back to 1.65%. And thus we’re right back where we were at the end of March when the 10 year yield hit its high for the year.

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation

2021-10-13

It was one of those signals which mattered more than the seemingly trivial details surrounding the affair. The name MF Global doesn’t mean very much these days, but for a time in late 2011 it came to represent outright fear. Some were even declaring it the next “Lehman.”

August Avoids Zero In JGB’s

August Avoids Zero In JGB’s

2021-09-28

Central banks and their staffs have long been accused of trying to hide inflation. This allegation had been a staple of their critics, those charging reckless monetary policies for creating “too much” money that had allegedly been causing price imbalances all over the financial map.

Weekly Market Pulse: What Is Today’s New Normal?

Weekly Market Pulse: What Is Today’s New Normal?

2021-08-09

Remember “The New Normal”? Back in 2009, Bill Gross, the old bond king before Gundlach came along, penned a market commentary called “On the Course to a New Normal” which he said would be:

“a period of time in which economies grow very slowly as opposed to growing like weeds, the way children do; in which profits are relatively static; in which the government plays a significant role in terms of deficits and reregulation and control of the economy; in which the consumer stops shopping until he drops and begins, as they do in Japan (to be a little ghoulish), starts saving to the grave.”

Bond Reversal In Japan, But Pay Attention To It In Germany

Bond Reversal In Japan, But Pay Attention To It In Germany

2021-07-09

Yield curve control, remember that one? For a little while earlier this year, the modestly reflationary selloff in bonds around the world was prematurely oversold as some historically significant beginning to a massive, conclusive regime change.

Anyone Remember That Whole SLR Cliff?

Anyone Remember That Whole SLR Cliff?

2021-07-02

Does anyone remember the SLR “cliff?” Of course you don’t, because in the end it didn’t seem to make any difference. For a few weeks, it was kind of ubiquitous if only in the sense that it was another one of those deep plumbing issues no one seems able to understand (forcing all the “experts” to run to Investopedia in order write something up about it).

A Clear Balance of Global Inflation Factors

A Clear Balance of Global Inflation Factors

2021-06-30

Back at the end of May, Germany’s statistical accounting agency (deStatis) added another one to the inflationary inferno raging across the mainstream media. According to its flash calculations, German consumer prices last month had increased by the fastest rate in 13 years.

The Inflation Emotion(s)

The Inflation Emotion(s)

2021-06-10

Inflation is more than just any old touchy subject in an age overflowing with crude, visceral debates up and down the spectrum reaching into every corner of life. It is about life itself, and not just quality. When the prices of the goods (or services) you absolutely depend upon go up, your entire world becomes that much more difficult.

Tags: Abenomics,bank loans,Bank of Japan,Bonds,currencies,economy,EuroDollar,Featured,Federal Reserve/Monetary Policy,inflation,inflation expectations,interest rate fallacy,Interest rates,Japan,lending,Markets,money creation,money printing,newsletter,QQE