The months of November and December aren’t always easily comparable year to year when it comes to American shopping habits. For a retailer, these are the big ones. The Christmas shopping season and the amount of spending which takes place during it makes or breaks the typical year (though last year, there was that whole thing in March and April which has had a say in each’s final annual condition). The calendar being what it is – we’ve never been forced to use the French Revolutionary datebook, thankfully, not yet – there are quirks. Pertaining to US retail sales, the Census Bureau, the government’s agency given the task of keeping track, it really comes down to the number of weekends each way. That final one in November one year could be the first one for

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, Auto Sales, bonds, consumer spending, currencies, economy, employment, Featured, Federal Reserve/Monetary Policy, industrial production, light vehicle sales, Markets, Motor Vehicle Assemblies, newsletter, Retail sales, Unemployment

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

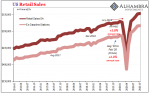

| The months of November and December aren’t always easily comparable year to year when it comes to American shopping habits. For a retailer, these are the big ones. The Christmas shopping season and the amount of spending which takes place during it makes or breaks the typical year (though last year, there was that whole thing in March and April which has had a say in each’s final annual condition).

The calendar being what it is – we’ve never been forced to use the French Revolutionary datebook, thankfully, not yet – there are quirks. Pertaining to US retail sales, the Census Bureau, the government’s agency given the task of keeping track, it really comes down to the number of weekends each way. That final one in November one year could be the first one for December the following year. This can lead to unusually large discrepancies between unadjusted data and seasonally-adjusted estimates. The latter attempt to make for, in Christmas shopping terms, homogenized calendars – without all the fuss and bother of running amok Jacobins. |

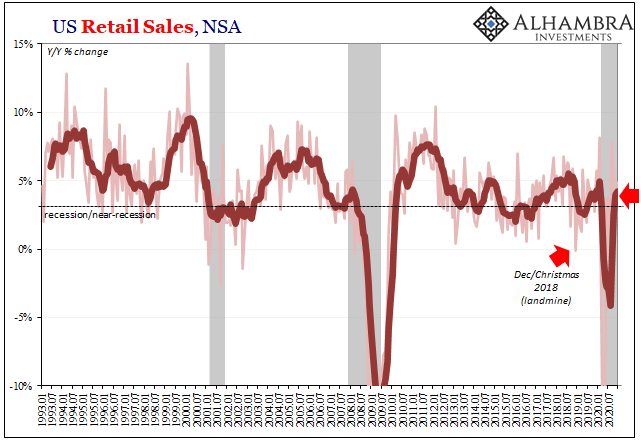

U.S. Retail Sales, NSA, Jan 1993 - Jul 2020 - Click to enlarge |

| With the in-between weekend ending up in December 2020 where it had been included in November 2019, the sales figures skew accordingly. The Census Bureau tells us that, unadjusted, November seemed low and December appeared better (revised 2.00% year-over-year and 4.85%, respectively).Seasonally-adjusted, neither was particularly good (3.74% and 2.94%, respectively). And if you combine November and December 2020’s unadjusted together, on a holiday basis the two months together were just 3.5% above the same pair in 2019.

Or was that awesome? It’s hard to tell because of the circumstances surrounding last year and its massive economic recession. In any other year, growth rates for holiday shopping down around 3% is cause for recessionary concerns. However, could it be a minor miracle that retail sales are positive at all? The government would surely like to believe so because, given the employment situation, that Christmas wasn’t a complete wipeout seems like a win for Treasury (the Fed would like to jump on this, too, but any idea of QE’s “V” is long forgotten now). |

U.S. Retail Sales, Jan 2016 - Dec 2020 - Click to enlarge |

| However, concerns rise here, too, given that on a monthly basis retail sales had declined in each of the three months of Q4. |

U.S. Retail Sales, Jan 1992 - 2020 - Click to enlarge |

| Like the labor market, consumer spending ended 2020 going in the wrong direction. Therefore, what had been motivated “stimulus” indifference has been transformed into urgency.

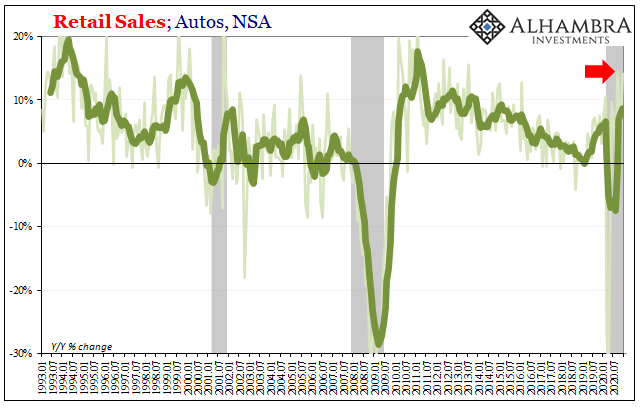

It’s also difficult to say just how urgent government aid and stipends really need to be coming from the consumer spending data. This thing about auto sales that we’ve been documenting for months has reached an untenable point; Census says auto sales are practically booming, but practically no one else agrees. In the retail sales numbers, auto sales leaped by 14% year-over-year, and not for the first time of late. |

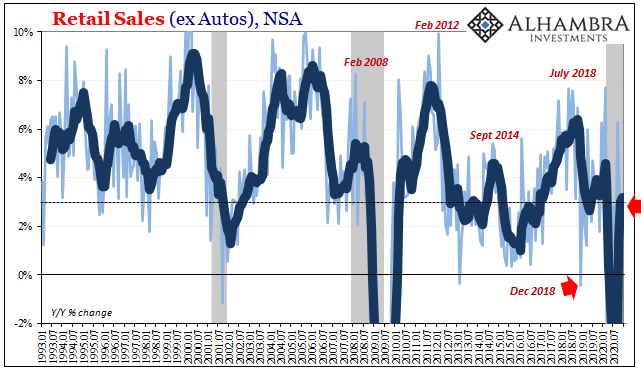

U.S. Retail Sales ex Autos, Jan 1993 - Dec 2020 - Click to enlarge |

| What that means for overall retail, if you take autos out, the combined holiday period goes from 3.5% (noted above) down to just 2.5%. That’s how much of a positive contribution this apparent splurging may have made. |

U.S. Retail Sales Autos, Jan 1993 - Dec 2020 - Click to enlarge |

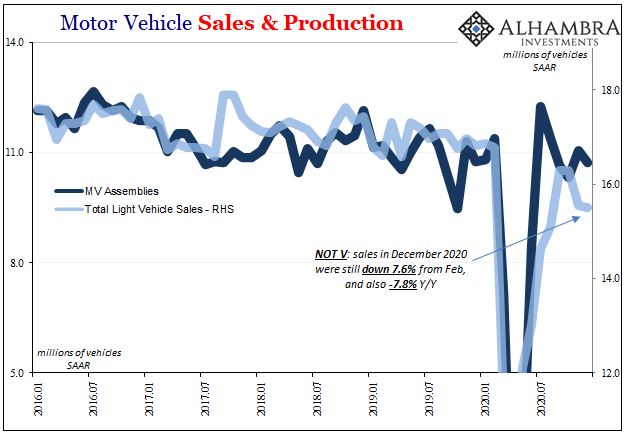

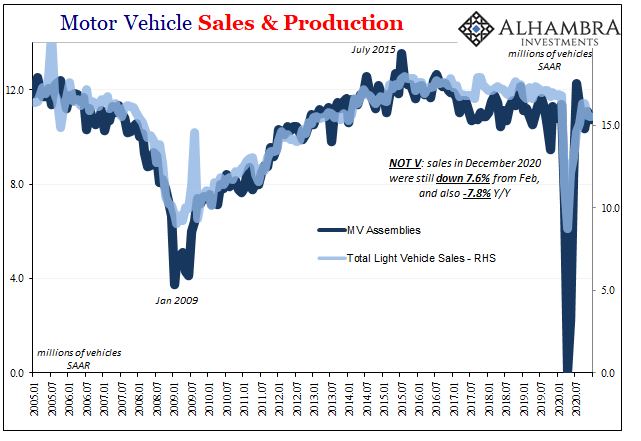

Motor Vehicle Sales & Production, Jan 2016 - Dec 2020 - Click to enlarge |

|

| However, if you go to the BEA’s estimates for light vehicle sales (which only tallies the number of units, unlike retail auto sales which tries to figure the total dollar value of everything sold) the auto sector is going in the clear opposite direction. In this series, the number of units moved in November 2020 was around 15.6 million (SAAR), or 8.4% fewer than during November 2019. Estimates for December 2020 (not released yet) are a little lower still, 15.5 million, which would be 7.8% less than December 2019.

Auto sales up 14%, or down 8%? According to another data source, the Federal Reserve, domestic auto production seems to be corresponding with the -8%. |

Motor Vehicle Sales & Production, Jan 2005 - Dec 2020 - Click to enlarge |

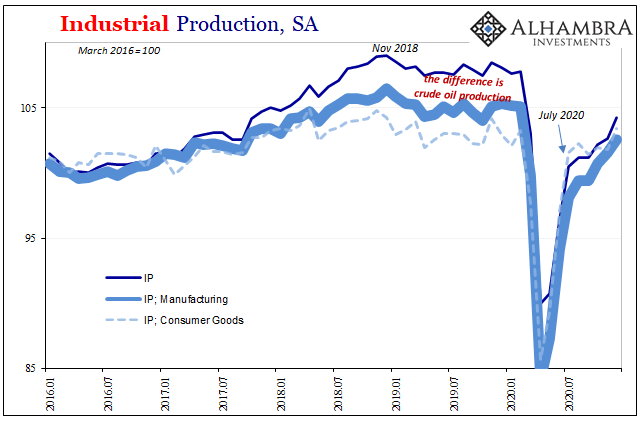

| In its Industrial Production series, the number of Motor Vehicle Assemblies (MVAS) in December was just 10.7 million (SAAR). Prior to this year, there had only been 7 months since the start of 2014 when output had been less than 10.75 million.

In other words, presumed production of cars and light trucks continues to move along at an unusually low level even though automakers in the US (according to the IP figures) and around the world (using other data) basically shut down production earlier in 2020 for the equivalent of almost three full months (half levels in March, near 100% in April, only slightly more in May, and then a little better than half in June). |

U.S. Industrial Production, Jan 2016 - Dec 2020 - Click to enlarge |

| Why aren’t carmakers producing at full speed and then some to make up for nearly a quarter-year of lost output? If the Census Bureau’s numbers are accurate, you’d think they’d be running three full shifts night and day to catch back up.

The discrepancy isn’t used cars, either. Though sales at used car dealers (included in the Census Bureau estimates) are up, too, they only make up about 1/9th to 1/10th of retail auto sales. It raises questions about data sources and integrity which quite naturally might arise given the ongoing situation. If auto sales are so far out of line – too high and too deferential to anticipated “stimulus” effects – in Census, might other data be the same even if not quite to this same level of difference? |

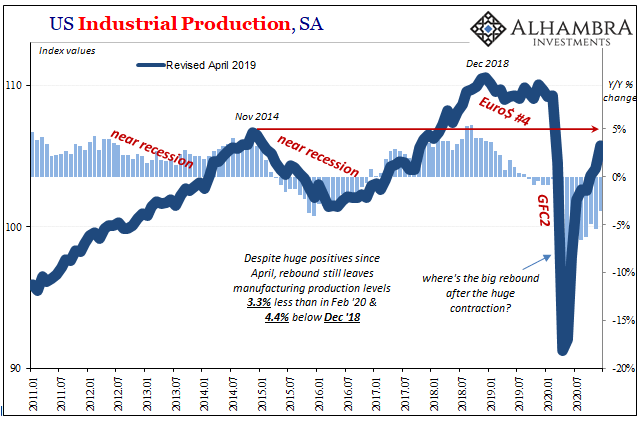

U.S. Industrial Production, SA, Jan 2011 - 2020 - Click to enlarge |

| Redbook index estimates, for example, have been running substantially less on average than rates put up pre-COVID. |

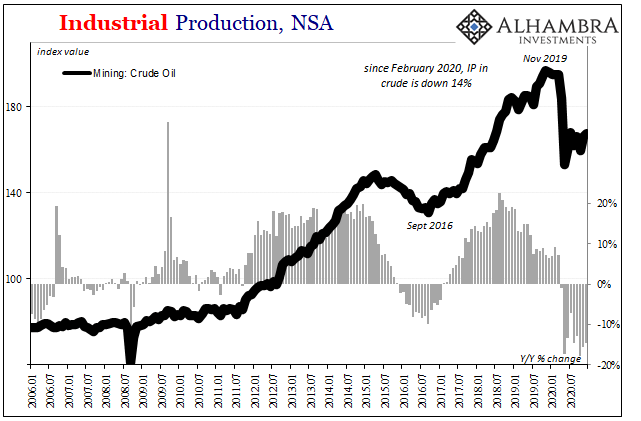

U.S. Industrial Production, Mining Crude, Jan 2006 - 2021 - Click to enlarge |

| That’s really what the entire IP estimates suggest. Not just in autos, but across-the-board American industrial output lags these spending figures to a substantial extent. Even though the Fed figures IP rose at a noticeably better rate in December (seasonally-adjusted when compared to November), overall total production remains down more than 3% compared to February and more than 4% compared to the prior peak which dates all the way back to the end of 2018.

That’s less output than November 2014. Forget any ideas about a labor bottleneck. |

Personal Income & Spending, Jan 2017 - 2020 - Click to enlarge |

If this is so, and the labor data sure looks like it, then it should be a factor to consider when thinking about what comes next and what 2021 ends up looking like. Vaccines, sure, but what else? Even though bond yields are up when compared to November and the lows in August, why aren’t they up more considering the supposed inflationary “consensus” gripping other asset classes?

Retail sales and especially autos only got halfway to a “V.” From these other data sources, the economy’s not even close to halfway having reached last year’s very, very welcome finish. The amount of lost activity throughout the majority of 2020, right up into December, it’s hard to believe that won’t matter; or if it does end up being a problem, Uncle Sam’s checks will, unlike Japan’s, render any longer run damage and consequences inconsequential. |

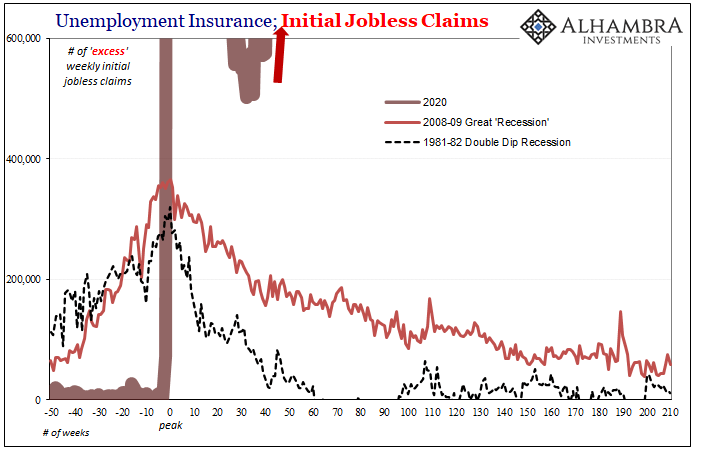

U.S. Unemployment Insurance; Initial Jobless Claims - Click to enlarge |

You Might Also Like

Extending the Summer Slowdown

Extending the Summer Slowdown

2020-11-20

A big splurge in September, and then not much more in October. While it would be consistent for many to focus on the former, instead there is much about the latter which, for once, is feeding growing concerns. Retail sales, American consumer spending on goods, has been the one (outside of economically insignificant housing) bright spot since summer

A Japanese Stall?

A Japanese Stall?

2020-07-24

In sharp contrast to the sentimental deference towards central bank stimulus exhibited by Germany’s ZEW, for example, similar Japanese surveys are starting to describe potential trouble developing. Like Germany, Japan is a bellwether country and a pretty reliable indicator of global economy performance.

Six Point Nine Times Two Equals What It Had In Twenty Fourteen

Six Point Nine Times Two Equals What It Had In Twenty Fourteen

2020-11-17

It was a shock, total disbelief given how everyone, and I mean everyone, had penciled China in as the world’s go-to growth engine. If the global economy was ever going to get off the ground again following GFC1 more than a half a decade before, the Chinese had to get back to their precrisis “normal.”

Of Incomplete Plans and Recoveries

Of Incomplete Plans and Recoveries

2020-07-21

At the monthly press conference China’s National Bureau of Statistics (NBS) now regularly gives whenever the Big Three economic accounts are updated (this time along with quarterly GDP), spokesman Liu Aihua was asked by a reporter from Reuters to comment on how the global economic recession might impact the Communist government’s long range goal of reaching its assigned GDP target.

*These* Are The Real Huge Jobs Numbers, And They Will Make Your Blood Run Cold

*These* Are The Real Huge Jobs Numbers, And They Will Make Your Blood Run Cold

2020-08-24

There is simply no way to spin these figures as anything good. Not just the usual ones were talking about here, but more so some new data that you probably haven’t seen before. Beginning with the regular, it doesn’t matter that the level of initial jobless claims has declined substantially over the past few weeks

China’s Hole Puzzle

China’s Hole Puzzle

2020-09-16

One day short of one year ago, on September 16, 2019, China’s National Bureau of Statistics (NBS) reported its updated monthly estimates for the Big 3 accounts. Industrial Production (IP) is a closely-watched indicator as it is relatively decent proxy for the entire goods economy around the world. Retail Sales in the post-Euro$ #2 context give us a sense of the Chinese economy’s persistent struggle to try to “rebalance” without the pre-2008 boost China had obtained through actual global growth contributing to its export orientation. The third of the Big 3 is Fixed Asset Investment (FAI), the real secret behind the country’s rapid modernization. FAI is how the Chinese view their own future, whether that’s as a rebalanced consumer-led economy leaping off into a brand new paradigm; or one

There Have Actually Been Some Jobs Saved, Only In Place of Recovery

There Have Actually Been Some Jobs Saved, Only In Place of Recovery

2020-12-04

The ISM reported a small decline in its manufacturing PMI today. The index had moved up to 59.3 for the month of October 2020 in what had been its highest since September 2018. For November, the setback was nearly two points, bringing the headline down to an estimate of 57.5.

This Global Growth Stuff, China Still Wants A Word

This Global Growth Stuff, China Still Wants A Word

2020-12-16

Before there could be “globally synchronized growth”, it had been plain old “global growth.” The former from 2017 appended the term “synchronized” to its latter 2014 forerunner in order to jazz it up. And it needed the additional rhetorical flourish due to the simple fact that in 2015 for all the stated promise of “global growth” it ended up meaning next to nothing in reality.Oddly the same for 2017’s update heading into 2018 and 2019.

Tags: Auto Sales,Bonds,consumer spending,currencies,economy,employment,Featured,Federal Reserve/Monetary Policy,industrial production,light vehicle sales,Markets,Motor Vehicle Assemblies,newsletter,Retail sales,Unemployment