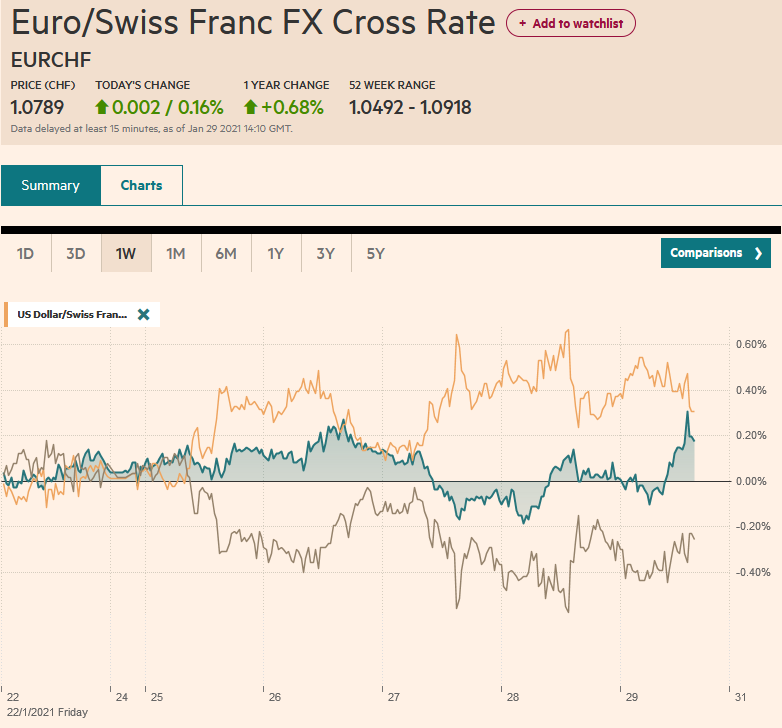

Swiss Franc The Euro has risen by 0.16% to 1.0789 EUR/CHF and USD/CHF, January 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Powerful corrective forces continue to grip the market. After a large rally to start the New Year, the correction is punishing. Most Asia Pacific equities markets were off again today to bring the week’s loss to 2.5% to 5.5% throughout the region. Europe’s Dow Jones Stoxx 600 is a little more than 1% lower on the day. The 2.4% loss for the week would be the largest since October and wipes out the month’s gain. US shares are trading heavily, and the S&P futures point to around a 1% drop, which is marginally lower for the year. Bond markets are not drawing a safe-haven bid, and

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movement, currency war, ECB, Europe, Featured, Japan, newsletter, silver, South Korea, Taiwan, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.16% to 1.0789 |

EUR/CHF and USD/CHF, January 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Powerful corrective forces continue to grip the market. After a large rally to start the New Year, the correction is punishing. Most Asia Pacific equities markets were off again today to bring the week’s loss to 2.5% to 5.5% throughout the region. Europe’s Dow Jones Stoxx 600 is a little more than 1% lower on the day. The 2.4% loss for the week would be the largest since October and wipes out the month’s gain. US shares are trading heavily, and the S&P futures point to around a 1% drop, which is marginally lower for the year. Bond markets are not drawing a safe-haven bid, and yields are mostly 2-4 bp higher. Italian bonds are performing best as the market anticipates some kind of resolution to the political turmoil without resort to disruptive and distracting elections. The 10-year US Treasury yield is about 1.07%, a four basis point increase on the week. Only the Norwegian krone is stronger against the dollar today among the major currencies. Of note, despite risk-off, the weakest of the major currencies today are the Australian dollar and Japanese yen, off around 0.5%. Emerging market currencies are mixed, and the JP Morgan Emerging Market Currency Index is up a little today but is still off about 0.25% for the week. If sustained, it would be the sixth consecutive weekly decline. Gold is firm but continues to consolidate around $1850 (200-day moving average). Silver has reportedly drawn interest from the swarm of retail investors. The metal was up nearly 5% yesterday and is up nearly another 1% today. Near $27.10, silver at three-week highs. March WTI is little changed and is in the lower end of its recent consolidative range ($52-$54). |

FX Performance, January 29 - Click to enlarge |

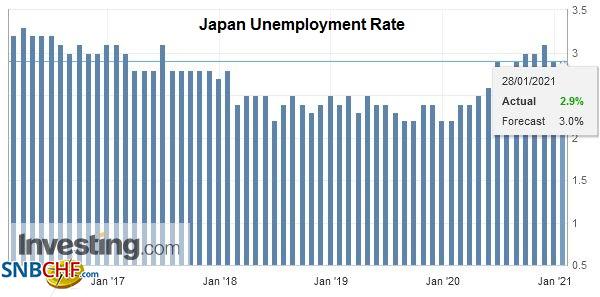

Asia PacificJapan’s economy finished 2020 on a weak note. Retail sales fell by 0.8% in December, a little more than expected, and follows a 2.1% decline in November. Industrial output tumbled 1.6% in December for a 3.2% year-over-year contraction. Unemployment was unchanged at 2.9%. The preliminary PMIs show economic activity is still contracting, and areas that account for around 60% of GDP are in a formal state of emergency. The BOJ does not meet until March. Talk that it would pull back from its ETF buying has been dampened by the recent volatility, while some speculate that officials could tolerate a wider range for the 10-year yield. |

Japan Unemployment Rate, December 2020(see more posts on Japan Unemployment Rate, ) Source: investing.com - Click to enlarge |

South Korea and Taiwan data points point to a regional recovery, despite Japanese woes. Seoul reported a 3.7% jump in December industrial output, a multiple of what was expected. Taipei reported Q4 GDP rose 4.9% year-over-year, making it one of the few economies to expand in 2020. Over the weekend, China’s PMI will be released, and a little softening is expected within the expansion.

The Japanese yen’s safe-haven appeal always seemed more complicated to us than “buy yen when there is trouble”. We often saw it linked to unwinding its funding role (borrowed and sold to finance the purchase of higher beta assets, and when those assets go south, which they invariably do, the trade is unwound the funding currency has to be bought back too). Despite the dramatic equity reversal, the yen is at its weakest level against the dollar since mid-November. The greenback has risen more than 0.5% against the yen today, its third consecutive advancing session. It appears that participants turned more cautious as the JPY105-level came into view. Three-month implied volatility is firm just below 6%, which is still soft. The 100-day average is closer to 6.8%. We suspect the spot move today is exhausted or nearly so. Support now is seen in the JPY104.40-JPY104.60 area.

The Australian dollar recovered smartly yesterday after dipping below $0.7600 briefly and reached almost $0.77 late in North America. However, there has been no follow-through selling, and the Aussie is on its backfoot. Recall that it finished last year just below $0.7700. A convincing break of $0.7600 now points to $0.7500. The PBOC’s dollar reference rate was set at CNY6.4709, which was weaker than the bank model’s suggested. In recent days, the reference rate was set higher than the models projected. We have been following for you the snugging–tightening financial conditions short of a formal rate hike– by the PBOC. It continues even though officials injected liquidity for the first time this week. The overnight repo rate rose 28 bp to 3.33% today, a nearly six-year high. Month-end and tax payments have increased the demand for liquidity as the PBOC withdrew it. It hit a low last month of about 60 bp. It appears that officials are trying to force de-levering ahead of the Lunar New Year when it will likely pump in more liquidity. The Chinese yuan has appreciated by about 1.35% against the US dollar on the month, making it among the strongest emerging market currencies.

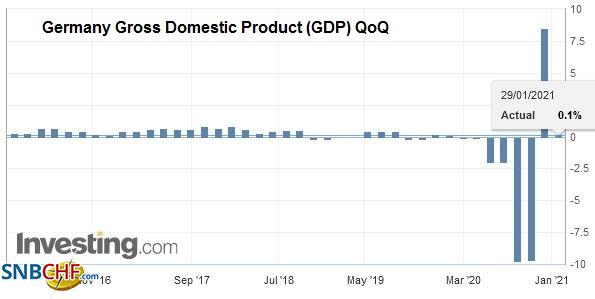

EuropeThe preliminary estimates of Q4 GDP for Germany, France, and Spain were all a little better than expected. However, the limited market impact is reasonable given the risks of contraction in Q1. Germany’s GDP rose by 0.1%. Most were looking for stagnation. Year-over-year, the world’s fourth-largest economy contracted by 2.9%. |

Germany Gross Domestic Product (GDP) QoQ, Q4 2020(see more posts on Germany Gross Domestic Product, ) Source: investing.com - Click to enlarge |

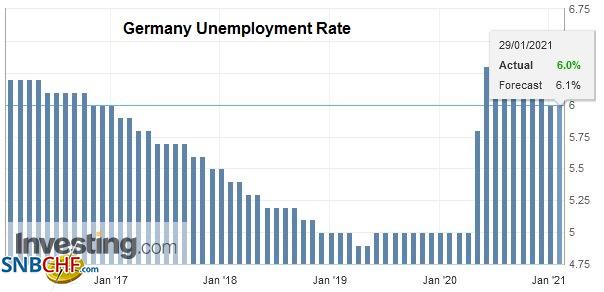

| Separately, it also reported that January unemployment was steady at 6.0%. Helped by a surge in consumer spending in December (23%), France’s Q4 GDP fell by 1.3%, considerably better than the median forecast (Bloomberg survey) of a 4% contraction. |

Germany Unemployment Rate, January 2021(see more posts on Germany Unemployment Rate, ) Source: investing.com - Click to enlarge |

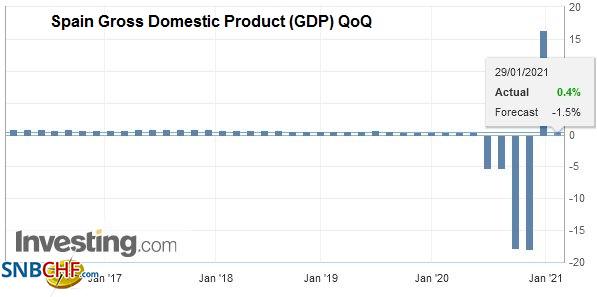

| A recovery in Spain’s retail sales also helped Q4 GDP. Rather than contract, like nearly everyone expected, the economy grew by a modest 0.4%. Spain also reported preliminary January CPI figures. Following Germany, VAT-led surge in prices, Spain’s January CPI slipped 0.3% on the month, but due to the base effect (January 2019, it fell by 1.4%) rose by 0.6% year-over-year, the highest since last February. |

Spain Gross Domestic Product (GDP) QoQ, Q4 2020(see more posts on Spain Gross Domestic Product, ) Source: investing.com - Click to enlarge |

A recent flurry of comments about the euro and the possibility of cutting rates has spurred talk of the forever currency wars. It is a mistake. Was there any talk of currency wars when Trump or Mnuchin tried talking the dollar down? There have been several other countries, mostly emerging market countries, that have intervened. One major country, Sweden, announced a program to buy foreign currencies, but that is designed to shift the funding of its reserves to SEK borrowing. Reports that measure the dollar’s sell-off since March are cherry-picking the spike high during the early days of the pandemic. Claims that Yellen rejected the strong dollar policy are in error. Even though she did not use the loaded phrase, she articulated its spirit. The US would not seek to purposely devalue the dollar to gain competitive advantage, and it wants other countries to do the same. Lastly, the ECB did not talk about a rate cut; a couple members did. Lagarde, though, at the recent ECB meeting was clear. All of the ECB’s tools are available and can be adjusted in several dimensions. Given ECB’s Makhlouf’s comments, playing down the need for a rate cut seems like there is an internal debate at the ECB that bled into the public space.

The euro is trading quietly in about a 35 tick range today within yesterday’s range, which was within Wednesday’s range (~$1.2060-$1.2170). It finished last week near $1.2170 and ended last year near $1.2215. The intraday technical readings are stretched. Immediate resistance is seen around $1.2140. Sterling is trading quietly but lower within the well-worn ranges seen over the past couple of weeks. It has closed below $1.36 since January 18. The top end of the range is not as clear. It reached almost $1.3760 in the middle of the week. It finished last week near $1.3685.

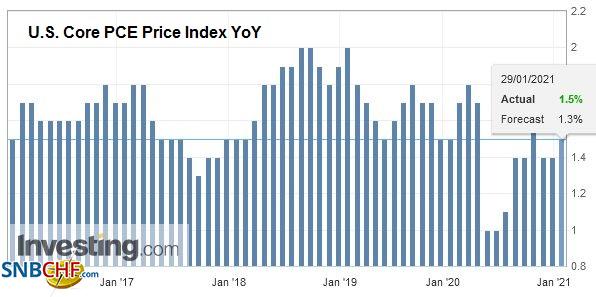

AmericaThe US reports December personal income and consumption data today, but there really is no new information in it. Yesterday’s Q4 GDP estimate (4%) incorporated today’s reports. One interesting note from the GDP report was that consumer spending on services rose 4% while goods purchases slipped by 0.4%. The monthly PCE deflator may draw some attention, but there is still little in the hard data to justify elevated concerns despite the rise in inflation expectations. The headline deflator, which the Fed targets at an average rate of 2%, may have ticked up to 1.2% from 1.1%. The core rate, which the Fed talks about but does not target, may have slipped to 1.3% from 1.4%. |

U.S. Core PCE Price Index YoY, December 2020(see more posts on U.S. Core PCE Price Index, ) Source: investing.com - Click to enlarge |

Canada reports November GDP figures today. The economy is expected to have expanded by 0.4% in November as it did in October. It would leave the Canadian economy about 3.2% smaller than November 2019. Next week, Canada reports the January jobs data. The labor market is expected to have stabilized after losing almost 53k jobs last month. Mexico reported a record trade surplus in December yesterday ($6.2 bln vs. expectations for $4.6 bln). It suggests upside risk to the Q4 GDP report today. The median forecast (Bloomberg survey) is for a 3.1% expansion after 12.1% in Q3.

The US dollar reached CAD1.2880 yesterday, its highest level since December 23. The weakness in equities and risk-off took a toll. The greenback has pared yesterday’s gains and was sold to almost CAD1.2815. Although some more slippage is possible with support seen around CAD1.2800, the intraday technical readings suggest the downside may be limited. The US dollar finished last week near CAD1.2735. This would be the third consecutive weekly advance, and it could be the largest since last October. The greenback rose to a new high for the year against the Mexican peso yesterday (~MXN20.46), just shy of our MXN20.50 target. Like the Canadian dollar, the peso has been better bid in Europe today. However, the intraday technical indicators are stretched. Look for the US dollar to find support ahead of MXN20.12.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, September 1: Dollar Lurches Lower

FX Daily, September 1: Dollar Lurches Lower

2020-09-01

The US dollar has been sold-off across the board. The euro approached $1.20, and sterling neared $1.3450. The greenback traded below CAD1.30 for the first time since January. Most emerging market currencies but the Turkish lira, are also advancing today.

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

2020-08-31

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 2: Corrective Pressures Give the Greenback a Reprieve

FX Daily, September 2: Corrective Pressures Give the Greenback a Reprieve

2020-09-02

After poking above $1.20 for the first time in more than two years, the euro reversed lower yesterday and is continuing to succumb to profit-taking pressures today. Comments from ECB’s Lane appeared to trigger a reversal yesterday throughout the currency markets.

FX Daily, September 11: Still Reluctant to take Euro above $1.19 but Sterling Remains Unloved

FX Daily, September 11: Still Reluctant to take Euro above $1.19 but Sterling Remains Unloved

2020-09-11

Yesterday’s roller-coaster price action has not had much impact on today’s activity. The slide in US equities after early gains failed to prevent Japanese, Chinese, and Hong Kong equities from advancing, though other markets in the region were not as resilient.

FX Daily, September 24: Darkest Before Dawn

FX Daily, September 24: Darkest Before Dawn

2020-09-24

The two recent market developments, push lower in stocks, and higher in the dollar is continuing. Tuesday’s gains in the S&P 500 and NASDAQ were unwound on Wednesday and this is helping drag global markets lower. The MSCI Asia Pacific Index fell for the fourth consecutive session today and many markets (India, Shenzhen, Taiwan, and Korea) fell more than 2% and most others were off more than 1%.

FX Daily, October 1: Hope Springs Eternal

FX Daily, October 1: Hope Springs Eternal

2020-10-01

Speculation that a new round of fiscal stimulus from the US is possible is encouraging risk-taking today. Many large Asian centers were closed for holidays today, and a technical problem prevented the Tokyo Stock Exchange from opening.

FX Daily, November 18: Balancing Pandemic Surge with Optimism about Vaccine

FX Daily, November 18: Balancing Pandemic Surge with Optimism about Vaccine

2020-11-18

News that Tokyo will go to its highest alert as it faces a rising contagion snapped a 12-day rally in the Nikkei, but most bourses in the Asia Pacific region excluding Japan advanced, though Chinese equities were mixed. European equities are narrowly mixed as the Dow Jones Stoxx 600 continues to gyrate within Monday’s range.

FX Daily, December 11: Brexit Fears Weigh on Sterling

FX Daily, December 11: Brexit Fears Weigh on Sterling

2020-12-11

Overview: The odds of a UK-EU agreement and new stimulus before year-end in the US have faded and are sapping risk appetites ahead of the weekend. Although most Asia Pacific equity markets gained, China and Australia were notable exceptions, European shares are heavy, and the Dow Jones Stoxx 600 is near three-week lows.

Tags: #USD,Currency Movement,currency war,ECB,Europe,Featured,Japan,newsletter,silver,South Korea,Taiwan