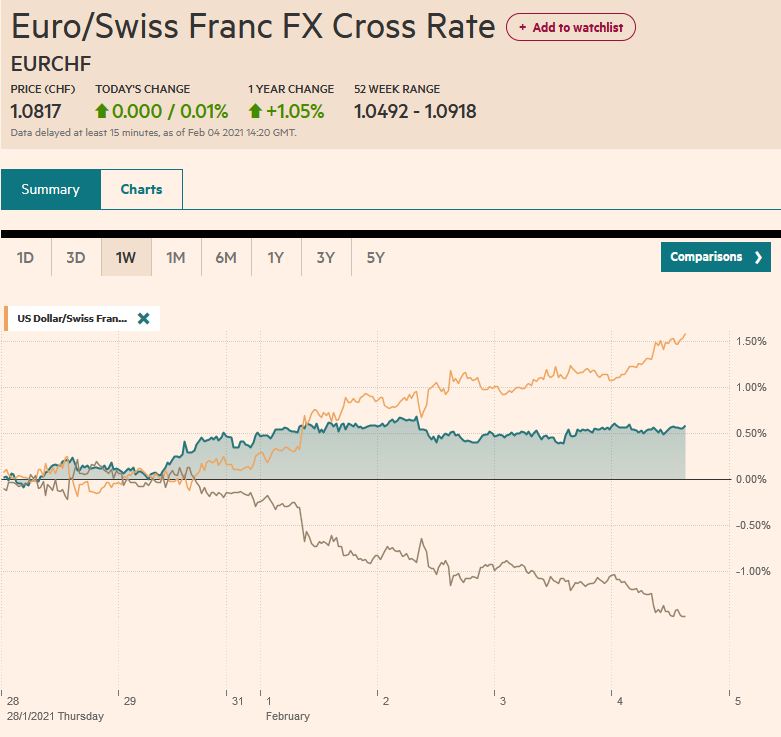

Swiss Franc The Euro has risen by 0.01% to 1.0817 EUR/CHF and USD/CHF, February 4(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The euro has been sold through .20 for the first time since December 1 and has now given back roughly half of the gains scored from the US election (~.16) to the early January high (~$.1.2350). More broadly, the greenback is bid against most of the major currencies, with the Australian dollar more resilient after reported record iron ore exports and all but a handful of emerging market currencies. Risk appetites, as expressed in the equities markets, are more subdued. The MSCI Asia Pacific Index snapped a three-day (4%+) advance, while Europe’s Dow Jones Stoxx 600 is

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Australia, Bank of England, China, Currency Movement, Featured, negative rates, newsletter, Oil, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.01% to 1.0817 |

EUR/CHF and USD/CHF, February 4(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The euro has been sold through $1.20 for the first time since December 1 and has now given back roughly half of the gains scored from the US election (~$1.16) to the early January high (~$.1.2350). More broadly, the greenback is bid against most of the major currencies, with the Australian dollar more resilient after reported record iron ore exports and all but a handful of emerging market currencies. Risk appetites, as expressed in the equities markets, are more subdued. The MSCI Asia Pacific Index snapped a three-day (4%+) advance, while Europe’s Dow Jones Stoxx 600 is consolidating in a narrow range, though holding above the gap created with yesterday’s sharply higher opening. US shares are a little firmer. Benchmark 10-year bond yields are little changed, leaving the US Treasury around 1.13%. Italian bonds also remain firm as the political drama of establishing a technocrat government continues. The price of gold lurched lower. Having settling Monday above $1860, gold has been sold through the trendline connecting the November and January lows (~$1817) and fallen to nearly $1810 before stabilizing a bit in the European morning. Oil prices are moving in the opposite direction. March WTI is advancing for the fourth session to straddle the $56-a-barrel level. It finished last week, a little above $52. |

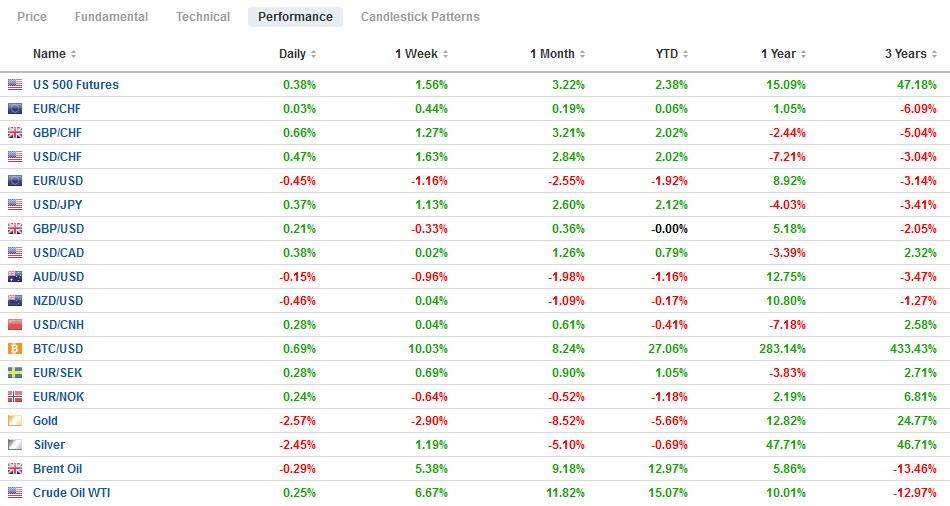

FX Performance, February 4 - Click to enlarge |

Asia Pacific

Australia’s December trade surplus was not as large as expected, and exports did not rise as anticipated, but the details were favorable. The surplus widened to A$6.79 bln from A$5.01 bln. Exports rose by 3% for the second consecutive month. Economists had looked for an acceleration. Imports, which rose by a revised 9% in November (from initially 10%), fell by 2%, as expected. On one level, it is notable that Australia completed its third consecutive year with a trade surplus. On another level, iron ore exports surged by 21% in the month to a new record of A$12.6 bln. Coal exports rose by 26% to A$3.7 bln. Moreover, the country breakdown showed that China, which had been punishing Australian exporters for Canberra’s foreign policy, relented. Australia’s exports to China rose 21% in the month of December to A$13.3 bln. Exports to Japan increased by almost a quarter to A$4.4 bln.

Reports indicate that foreign investors increased their Chinese government bonds’ purchases in January to a recovery of CNY121 bln (~$18.7 bln). Their holdings are now estimated to be about CNY2 trillion), which is about 4% of the outstanding. The inclusion of Chinese bonds in major benchmarks, coupled with the relatively high yield and an appreciating currency, makes it a favored play by real and levered accounts. Offshore investors added CNY570 bn to their holdings in 2020, more than double the net purchases in 2019.

The US dollar was confined to a 20-pip range against the Japanese yen yesterday and enjoys a slightly wider range today. It has recorded a new high for the move, just shy of JPY105.30. Today is the seventh consecutive dollar advance. The next resistance area is seen around JPY105.60, which also houses an expiring option of around $475 mln and the 200-day moving average. Given that the intraday indicators are stretched, the North American market may find it challenging to extend the greenback’s upside that much ahead of the US jobs data tomorrow. While the trade figures helped lift the Australian dollar, it remains vulnerable to the recovering US dollar. It may spend most of the remainder of the session between $0.7600, where a A$545 mln expiring option is struck, and $0.7640 area. The PBOC set the dollar’s reference rate at CNY6.4605, a little firmer than the models had it. The central bank’s liquidity provision was also seen as stingy, and this saw the overnight repo rate rise for the first time in four sessions (+19 bp to 2.05%).

| Europe

The results of the Bank of England meeting will be known shortly. The focus is not on what the BOE does. It is expected to do nothing. It is what is said that is more important, and here two issues are in focus. First are negative interest rates. The BOE wants to have its cake and eat it too: recognize that negative interest rates as a possible tool, which may help keep rates down without delivering what would appear to be a disruptive move. Officials conducted a survey, and some 160 detailed responses will be published. We note that the short-sterling futures curve implies negative rates in the June through December contracts. The two-year Gilt yields minus 8 bp. The second issue that the market will focus on are the updated economic forecasts. Given the pandemic and the Brexit-induced disruptions, it will likely revise down near-term growth prospects but could be more optimistic further out. |

Eurozone Retail Sales YoY, December 2020(see more posts on Eurozone Retail Sales, ) Source: investing.com - Click to enlarge |

Meanwhile, the BOE’s regulatory arm is reportedly warning UK financial institutions that they should not count on quick recognition by the EU of “equivalence,” which would allow UK financial services to be sold into the EU. Finance was not included much in the trade deal struck at the end of last year. The UK has indicated it will drop some European rules now that it is not obligated as a member of the EU.

The euro has been pushed below $1.20 to its lowest level since December 1. It has held above $1.1975, the (50%) retracement objective of the advance since the US election. The next (61.8%) retracement is a little below $1.19. We have noted a larger topping pattern that could project to around $1.1750. However, as North American traders return to their posts, the euro has stabilized and may squeeze higher. Initial resistance is seen around $1.2020. Note that there are options for around 2.7 bln euros struck between $1.2035 and $1.2050 that roll off today. Sterling is trading below $1.36 for the first time in about 2.5 weeks. Also of note, from a technical perspective, the five-day moving average is set to slip below the 20-day moving average for the first time since mid-December and reflects the loss of upside momentum in recent weeks. The euro is finding support near GBP0.8800. It was closer to GBP0.9200 a month ago.

America

In three large foreign policy issues, the Biden administration is continuing with previous policies. First, it has objected, and threatened sanctions as the Nord Stream 2 pipeline construction continues. Second, indications suggest no intention of lifting the ban on China’s Huawei and ZTE. Third, very early on, officials demonstrated resolve in the Pacific, confirming its umbrella protects Japan’s claim on islands that China also claims, and used a fleet to ensure freedom of navigation. It has reached out to Taiwan by inviting the de facto ambassador to the US in a move that is unprecedented since the US recognized one-China in the late 1970s. Trump also pushed China’s red line over Taiwan in his first days in office.

US oil inventories fell by a million barrels last week. An increase of half as much was expected after a 9.5 mln barrel drawdown was reported the previous week. That leaves US stocks about 4% above the five-year average for this time of year. Gasoline output rose a little to 8.4 mln barrels a day. Inventories increased by a little more than half of a day’s production last week to stand around 1% below its 5-year average.

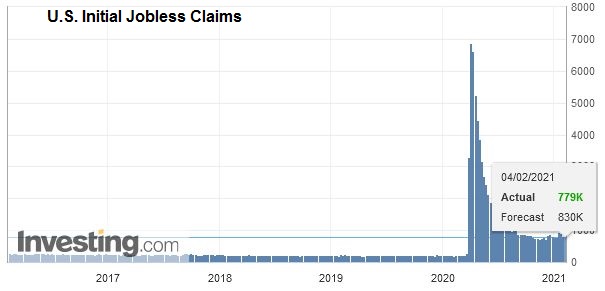

| The US sees several economic reports but, ironically, little new information. The Q4 productivity and unit labor costs are a function of Q4 GDP. Productivity fell, and unit labor costs rose. While the market may take note of the weekly jobless claims, the proximity of tomorrow’s national figures overshadows them. The information in the December factory goods orders is largely contained in the durable goods orders, which have already been released but are subject to revision today. The Fed’s Kaplan speaks again today, and his views are known. Daly speaks on a panel about the labor market later today. |

U.S. Initial Jobless Claims, February 04, 2020(see more posts on U.S. Initial Jobless Claims, ) Source: investing.com - Click to enlarge |

Canada and Mexico have quiet economic diaries today. The US dollar remains with the broad trading range set last Friday against the Canadian dollar. It is like a spring coiling, and it is often seen as a continuation pattern. Yet, ahead of tomorrow’s jobs data for both Canada and the US, the risk is more sideways action today between mostly CAD1.2760 and CAD1.2840. The greenback fell against the Mexican peso in the first two sessions this week and now is up for the second consecutive session. After recording a six-day low near MXN20.0750 yesterday, the US dollar recovered, and follow-through buying has lifted it above MXN20.28 today. There appears near-term potential toward MXN20.35-MXN20.40.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-02-08

Update February 8 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.3 bn. compared to last week, this means the SNB is selling euros and dollars.

FX Daily, January 22: Faltering Friday

FX Daily, January 22: Faltering Friday

2021-01-22

Fear that social restrictions may have to be broadened and extended is helping spur a wave of profit-taking and de-risking, which has also been encouraged by disappointingly high-frequency data. The equity rally seemed to falter a bit in the US, as the S&P 500 eked out a minor 0.03% gain yesterday.

FX Daily, December 17: Dollar Thumped

FX Daily, December 17: Dollar Thumped

2020-12-17

Overview: The prospects of a UK-EU deal and US stimulus continue to underwrite risk appetites and weigh on the dollar. Equity markets are moving higher. Led by Australia and China, the MSCI Asia Pacific Index rose to new record highs, while Dow Jones Stoxx 600 in Europe is at its best level since February.

FX Daily, December 15: The Bulls are Emboldened

FX Daily, December 15: The Bulls are Emboldened

2020-12-15

The S&P fell for the fourth consecutive session yesterday, the longest losing streak of the quarter, and this seemed to encourage profit-taking in the Asia Pacific region today. The MSCI Asia Pacific Index slipped for the second consecutive session, and even confirmation of the Chinese recovery failed to lift the Shanghai Composite.

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

2020-12-02

The selling pressure that drove the dollar lower yesterday has abated, and the greenback is paring yesterday’s loss, though the dollar-bloc currencies are showing some resilience. EC negotiator Barnier briefed ministers that the same three issues that have bedeviled the trade talks with the UK remain unresolved (fisheries, level playing field, and a conflict resolution mechanism).

FX Daily, November 27: Dollar Offered Ahead of the Weekend

FX Daily, November 27: Dollar Offered Ahead of the Weekend

2020-11-27

Equities are finishing the week on a firm tone, while the US dollar remains heavy. In the Asia Pacific, only Australia and India did not end the week on a firm note. The MSCI Asia Pacific completed its fourth consecutive weekly gain, for around a 13% gain.

FX Daily, November 5: The Dollar Slides and the Yuan Jumps

FX Daily, November 5: The Dollar Slides and the Yuan Jumps

2020-11-05

Overview: The markets did not wait for the final vote count and took stocks and bonds higher while pushing the greenback lower. While it appears Biden will be the next US President, investors seemed to like the fact that his agenda will be checked by a Senate that may remain in Republican hands. Stocks are on a tear.

FX Daily, October 15: Markets Shake and Dollar Goes Bid

FX Daily, October 15: Markets Shake and Dollar Goes Bid

2020-10-15

A combination of the surging virus, threatening the slow recovery that was already losing momentum, the lack of new stimulus in the US, and market positioning is seeing risk unwind in a big way today. Equities are selling off.

Tags: #USD,Australia,Bank of England,China,Currency Movement,Featured,negative rates,newsletter,OIL