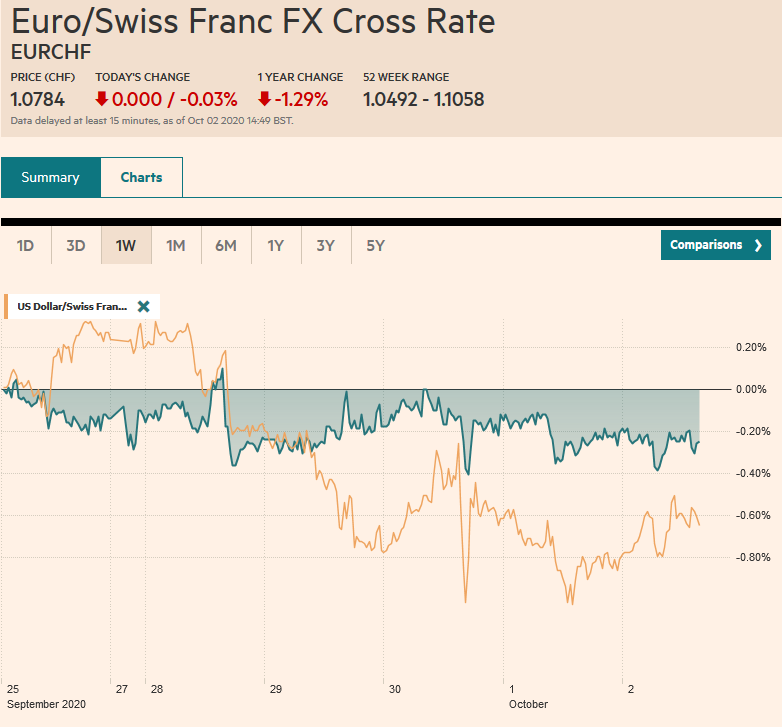

Swiss Franc The Euro has fallen by 0.03% to 1.0784 EUR/CHF and USD/CHF, October 2(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Before a US election, there is often speculation of a last-minute game-changing development. News earlier today that the US President and his wife have tested positive for the Covid virus has injected a new unknown into not only the US election but the markets as well. Many centers in Asia (China, HK, Taiwan, South Korea, and India) remain closed, while Australia and Japan surrendered early gains. European shares have recouped some of the initial sharper losses, and near midday the Dow Jones Stoxx 600 is off about 0.6% to hold on to about a 1.2% gain for the week. US shares are

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, COVID-19, Currency Movement, EMU, Featured, jobs, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.03% to 1.0784 |

EUR/CHF and USD/CHF, October 2(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Before a US election, there is often speculation of a last-minute game-changing development. News earlier today that the US President and his wife have tested positive for the Covid virus has injected a new unknown into not only the US election but the markets as well. Many centers in Asia (China, HK, Taiwan, South Korea, and India) remain closed, while Australia and Japan surrendered early gains. European shares have recouped some of the initial sharper losses, and near midday the Dow Jones Stoxx 600 is off about 0.6% to hold on to about a 1.2% gain for the week. US shares are around 1.2% lower. The bonds are not drawing much of a safe-haven bid. The US 10-year benchmark yield is around 67 bp. European yields are off slightly, though Italian bond yield is off a bit more as it dips below 80 bp to new lows. The dollar is mostly firmer. Sterling and yen are notable exceptions, while the Australian dollar, is snapping a four-day advance to lead the decliners. It is paring this week’s gains by about 0.5% leaving up about 1.6% on the week. Emerging market currencies are trading with a heavier bias, led by the Russian rouble and Mexican peso. The JP Morgan Emerging Market Currency Index is off about 0.15% and is up around 0.5% for the week. Gold is steady after approaching a nine-day high earlier (~$1917), while oil is slipping lower. The November WTI contract making new lows three-week lows near $37.20 a barrel. It is off about 6.7% this week after last week’s 2.6% fall. |

FX Performance, October 2 - Click to enlarge |

Asia Pacific

Japan’s jobless rate ticked up to 3% in August a three-month high from 2.9%. The job-to-applicant ratio deteriorated to 1.04 from 1.08. It reinforces the idea that after a strong start to Q3, the Japanese economy lost some momentum. Meanwhile, as we have anticipated, Prime Minister Suga is moving toward another supplemental budget. It would be the third and the local press is reporting it to be ready near the end of the year or January.

Australia reported that August retail sales fell by 4%, a little less than expected. It more than offsets the 3.2% gain in July and is the first decline since April’s 17.7% plunge. The new spread of the virus and lockdown of Victoria was the main drag.

The dollar fell to lows for the week against the Japanese yen, briefly dipping below JPY105 in the initial reaction to new of Trump’s contraction of the virus. It held the JPY104.90-level, where a $410 mln option is set to expire. It recovered to trade back at the lowe end of what had been this week’s range around JPY105.20. Another option (~$765 mln) is struck at JPY105.50 and also is set to expire today. The Australian dollar is off about 0.4% to snap a four-day rally that had retracement about half of its September losses. Its drop today to almost $0.7130 meets the (38.2%) retracement objective of the recent gains. Mild support near $0.7150 is seen in the European morning and a move above $0.7180 would be constructive for next week.

Europe

The eurozone’s inflation challenge remains. The preliminary September figures delivered the 0.1% month-over-month gain that was widely expected. The year-over-year rate, however, at -0.3% was a touch weaker than expected and the core rate slipped to a new record low of 0.2% from 0.4%, which was not anticipated. The low inflation is the thin edge of a wedge that is expected to be used to settle the debate between the region’s creditors and debtors. The former is looking to end the emergency stimulus as soon as the emergency is passed, while the latter looks to avoid repeating past mistakes and removing stimulus too early. The rubber meets the road at the December ECB meeting when the bond-buying program is expected to be extended.

Speculation yesterday that a break-through had been achieved in UK-EU trade talks send sterling to a two-week high near $1.30 before a cold slap of reality set in and sterling was sold back into the $1.2860-$1.2880 area. Talks between Frost and Barnier continue today. UK Prime Minister Johnson and EC President von der Leyen will hold direct talks over the weekend to map pout the path forward. The two outstanding issues remain state-aid and EU fishing rights in UK waters. The price action clearly showed buying on the rumored break-through, which we suspect to be in the first instance, short-covering. It shows the market expectations are pessimistic. There are other drivers, including the second strong wave of the virus and the Bank of England likely to ease policy next month, that also need to be weighed.

The euro dipped below $1.1700 on the news from the US, and quickly bounced but stopped shy of the $1.1750-level where a 2 bln euro option is set to expire today. There is also a 1.3 bln euro option at $1.17 that will be cut today too. Support extends to $1.1670. Near-term conviction has been undermined by the recent developments. We suspect that one implication is that if there is a strong reaction to the US employment data it may be faded. Sterling is trading within yesterday’s range (~$1.2820-$1.2980). It is encountering selling pressure in the European morning near $1.2950. There is an option for about GBP200 mln at $1.29 that rolls off today.

America

The US President and First Lady have tested positive for Covid-19. It is a tragedy and could have far-reaching implications. Some of already speculating what it means for fiscal efforts and for the election that is a little more than a month away. Some observers talk about a sympathy vote, as UK Prime Minister Johnson saw a bit more support when he became infected. Most polls had Trump trailing Biden overall and in most of the swing states. At first blush, we suspect that it is not a game-changer for the election or for the trajectory of fiscal policy.

| Back in the 1980s, as Lighthizer wrestled with the Japanese, who was said to be responsible for the US external imbalance, the monthly trade report was elicited the biggest response from the foreign market. In 1985, the year the US helped arrange the Plaza Agreement to drive the dollar lower, it recorded an annual trade deficit of $114 bln. It peaked a couple of years later around $144 bln. The August trade balance will be reported on October 6. If the median forecast is close to the money, the US would have recorded almost $130 bln trade deficit in July and August together. It has lost its sting. For years, it seems that the monthly jobs report has the biggest impact. It is the first broad glimpse into the economy in a new month in terms of hard data. It is difficult to forecast. However, it may also be losing its sting. |

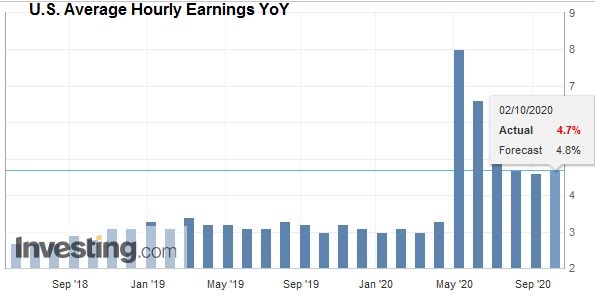

U.S. Average Hourly Earnings YoY, September 2020(see more posts on U.S. Average Hourly Earnings, ) Source: investing.com - Click to enlarge |

| The median forecast is for an 875k rise in non-farm payrolls. Investors learned yesterday that 837k Americans filed an initial claim for jobless benefits, and another 650k applied for the Pandemic Unemployment Assistance program It is true that they are non measuring the same thing, but six months after the pandemic struck and around four months since the economy began recovering, the number of people filing for unemployment benefits is four-times what it was pre-crisis. |

U.S. Nonfarm Payrolls, September 2020(see more posts on U.S. Nonfarm Payrolls, ) Source: investing.com - Click to enlarge |

| No matter what today’s employment report shows, there is a deep conviction, reinforced by the recent slew of corporate lay-off announcements, including a couple of airlines and a few large banks, that the labor market remains stressed. What improvement there is appears to be slowing, and a better sense of what are permanent and temporary lay-offs become clearer. |

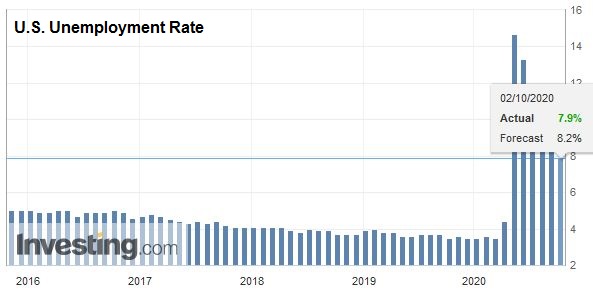

U.S. Unemployment Rate, September 2020(see more posts on U.S. Unemployment Rate, ) Source: investing.com - Click to enlarge |

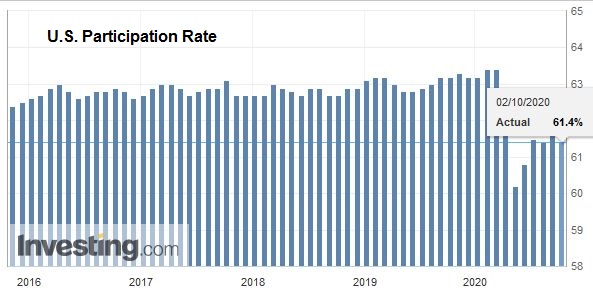

| Through September it looks as if around half of the employees returned to their jobs, which is also what the participation rate will likely show. |

U.S. Participation Rate, September 2020(see more posts on U.S. Participation Rate, ) Source: investing.com - Click to enlarge |

At yesterday’s low below CAD1.3270, the US dollar neared the (38.2%) retracement objective of the September rally. The risk-off mood has seen this area hold, and the greenback recovered toward CAD1.3330 today. Resistance is likely in the CAD1.3345-CAD1.3360 area. If this is overcome, it would signal a likely re-test on the cap near CAD1.3420. The greenback dropped around 2.8% against the Mexican peso in the last two sessions but has come back bid in light of the developments. It had approached the 200-day moving average (~MXN21.77) yesterday and is holding below yesterday’s highs (~MXN22.13). A move above yesterday’s highs could spur a move toward MXN22.25-MXN22.35.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

A flurry of deals, including the still-evolving Oracle-TikTok tie-up, helped lift equity markets in the Asia Pacific region. South Korea’s Kospi, and Indonesia, which had been battered last week, led the advance. The MSCI Asia Pacific Index rose for the third consecutive sessions. European bourses are little changed while US stocks are firmer.

FX Daily, October 1: Hope Springs Eternal

FX Daily, October 1: Hope Springs Eternal

Speculation that a new round of fiscal stimulus from the US is possible is encouraging risk-taking today. Many large Asian centers were closed for holidays today, and a technical problem prevented the Tokyo Stock Exchange from opening.

FX Daily, July 2: Dollar Thumped Ahead of US Jobs Report

FX Daily, July 2: Dollar Thumped Ahead of US Jobs Report

Market optimism over the possibility of a vaccine in early 2021 overshadowed the continued surge in US cases, where the 50k-a-day threshold of new cases has been breached. Following the NASDAQ close yesterday at record highs, global equities have advanced. Led by Hong Kong returning from yesterday’s holiday, Asia Pacific equities rallied. Most local markets rose by more than 1%, though Tokyo and Taiwan lagged.

FX Daily, July 6: New Record Number of Covid Cases Doesn’t Curtail Appetite for Risk

FX Daily, July 6: New Record Number of Covid Cases Doesn’t Curtail Appetite for Risk

Overview: A new daily high number of contagions globally has been reported, but the risk-appetites have been stoked. Chinese stocks have been on a tear. The Shanghai Composite rallied 5.7% today to bring the five-day advance to 13.6%. Most other regional markets, including Hong Kong, rallied as well (3.8%). Australia was the main exception, and it pulled back by 0.7%. It is still up a solid 3.4% over the past five sessions.

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

The optimism among investors appears to have evaporated in the face of new US-Chinese tensions, possible delays in the next US fiscal stimulus, and new record virus infections in Australia and Hong Kong. US stocks had pared early gains yesterday, and the high-flying NASDAQ finished lower after setting new record highs.

FX Daily, August 07: Position Adjustment Dominates ahead of US/Canada Employment Reports

FX Daily, August 07: Position Adjustment Dominates ahead of US/Canada Employment Reports

Escalating dramas may be behind the position adjustment today ahead of the US jobs data. The US and China feud expanded beyond Tiktok to WeChat, and efforts to tighten disclosure rules for Chinese companies listed in the US are nearing. The negotiations between the White House and the Democrats broke down, preventing or at least delaying additional stimulus.

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 28: Stocks Recover while the Greenback Consolidates

FX Daily, September 28: Stocks Recover while the Greenback Consolidates

Overview: Following the strong finish in the US before the weekend, global equities are paring last week’s slide. The MSCI Asia Pacific Index rose to for a second session. Markets in Japan, Taiwan, South Korea, and India rose by more than 1%. China and Australia were notable exceptions.

Tags: #USD,Brexit,COVID-19,Currency Movement,EMU,Featured,jobs,newsletter