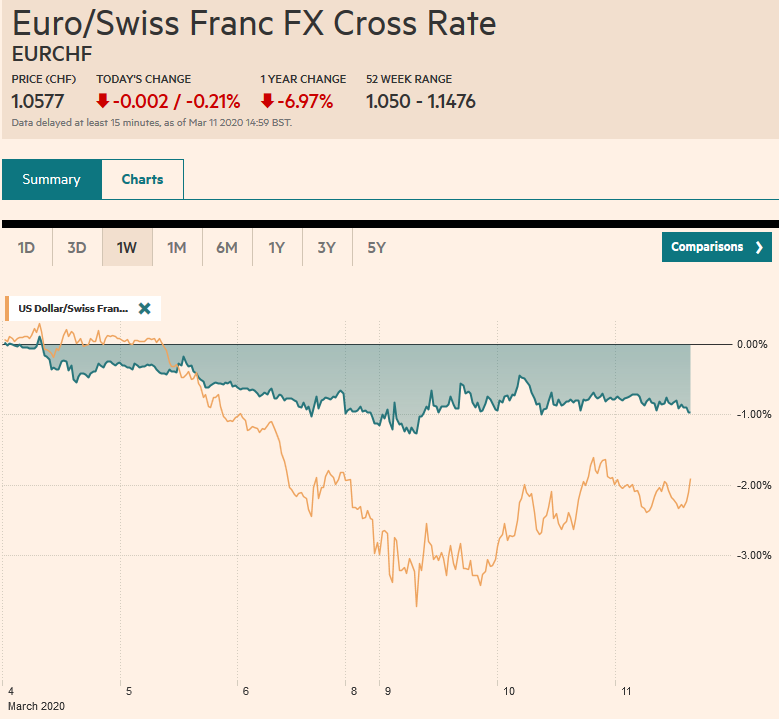

Swiss Franc The Euro has fallen by 0.21% to 1.0577 EUR/CHF and USD/CHF, March 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The S&P 500 and Dow Jones Industrials sold off after the higher open and briefly traded below yesterday’s lows. Investors seemed disappointed that the Trump Administration was not ready with specific policies after Monday’s tease that had initially helped lift Asia Pacific and European markets earlier on Tuesday. This sparked a sharp decline in Europe into the close. Several individual European markets posted bearish outside down days by trading above yesterday’s highs and then reversing to close at new lows. However, as investors concluded that US fiscal support would be

Topics:

Marc Chandler considers the following as important: 4) FX Trends, 4.) Marc to Market, Bank of England, COVID-19, Currency Movement, Featured, newsletter, Oil, USD

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Swiss FrancThe Euro has fallen by 0.21% to 1.0577 |

EUR/CHF and USD/CHF, March 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

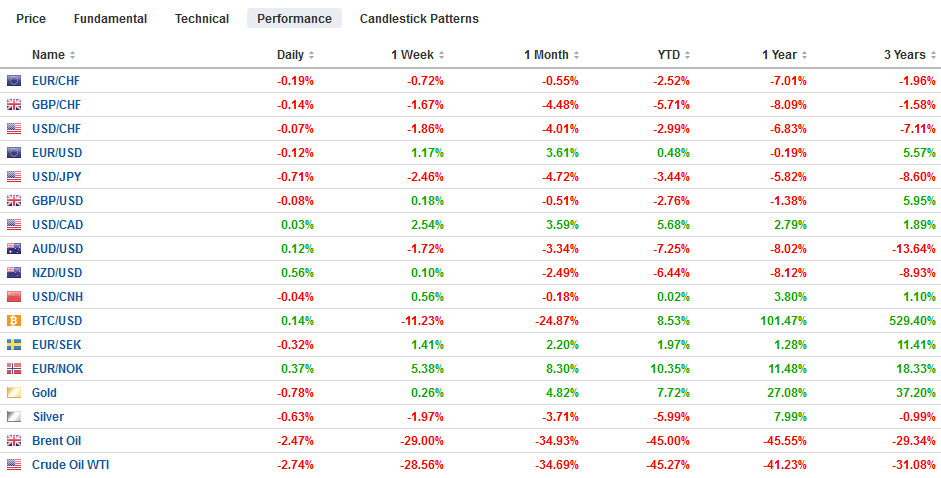

FX RatesOverview: The S&P 500 and Dow Jones Industrials sold off after the higher open and briefly traded below yesterday’s lows. Investors seemed disappointed that the Trump Administration was not ready with specific policies after Monday’s tease that had initially helped lift Asia Pacific and European markets earlier on Tuesday. This sparked a sharp decline in Europe into the close. Several individual European markets posted bearish outside down days by trading above yesterday’s highs and then reversing to close at new lows. However, as investors concluded that US fiscal support would be forthcoming US stocks rallied to new highs late in the session. Yet, after the close, official comments gave a sense that there was still no agreement, and President Trump did not attend the White House briefing. US stocks softened in early electronic trading, which weighed on Asia-Pacific markets. The Bank of England delivered an emergency 50 bp cut and some other credit easing measures shortly before the UK markets opened a few hours before the government unveils its. Sterling initially fell but quickly recovered to new session highs. European equities are higher, and the Dow Jones Stoxx 600 is about 2% higher, led by financials, energy, and materials. US shares are unable to build on yesterday’s gains, and the S&P 500 is a little more than 1% lower after yesterday’s nearly 5% advance. Core European 10-year benchmark yields are 3-5 bp higher, while peripheral bond yields are lower, led by around 10 bp declines in Italy and Greece. The US 10-year Treasury yield is off about seven basis points (to 73 bp) after rising 26 bp yesterday. The dollar is trading heavily against all the major currencies. Emerging market currencies are mixed, with eastern and central European currencies faring best, with the Mexican peso and South African rand picking the rear, with 0.4%-0.5% losses. Gold is up 0.5% to recoup about a third of yesterday’s decline, while crude pares its more than 10% gain and is straddling $34 a barrel. |

FX Performance, March 11 - Click to enlarge |

Asia Pacific

Japan saw its first case of the coronavirus two months ago, and pressure continues to mount on the Abe government to take bolder action. Abe’s public support has fallen to its lowest level in more than a year and a half. The government funds committed are not new spending but using reserves from previous budgets, including December’s JPY13.2 trillion package. The handling of the public health crisis contrasts with how it handled the earthquake, tsunami, and nuclear accident that took place nine years ago today.

Australia is expected to unveil its fiscal response tomorrow. Reports suggest it will spend A$2.4 bln and include 100 pop-up clinics. South Korea is also putting together an extra budget. On monetary policy, several central banks that do not meet soon, like South Korea, India, and Malaysia, are seen as potential candidates to make emergency cuts.

The dollar rose 3.2% against the yen yesterday finish the North American session near JPY105.65. It had not risen through there and consolidated by easing to almost JPY104 in late Asia before the higher European equity market appeared to help it recover above JPY105. A $420 mln option at JPY105.50 expires today. A three-day trendline on the hourly charts intersects near JPY105 at the end of today’s session. The Australian dollar is firm above $0.6500 as it consolidates in the lower end of yesterday’s range that saw it briefly trade above $0.6600. Support is seen in the $0.6465-$0.6480 area. The dollar rose to a six-day high against the Chinese yuan (~CNY6.9665) to close a gap created on March 4. Chinese lending data from February was considerably weaker than expected, but the Lunar New Year skewed the data in any event and did not seem to impact CNY or CNH.

EuropeThe Bank of England surprised nearly everyone by delivering an emergency 50 bp rate cut (brings the base rate to 25 bp) a few hours before the budget is unveiled. It also took other credit measures to help ease the strain, including reducing banks’ capital requirements to facilitate easy access to cheap credit. Note that BOE Governor Carney’s term ends next week, and Andrew Bailey will succeed him on March 16, and the next MPC is on March 26. Given the variable lag and leads of monetary policy, the move now is more about showing a coordinated government response. |

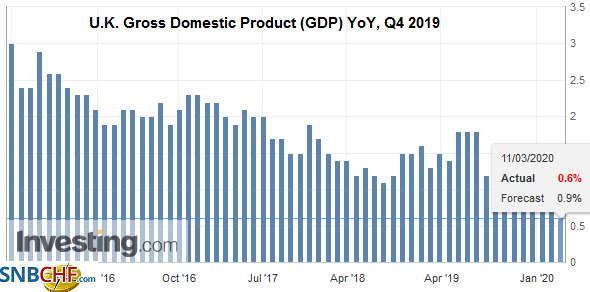

U.K. Gross Domestic Product (GDP) YoY, Q4 2019(see more posts on U.K. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

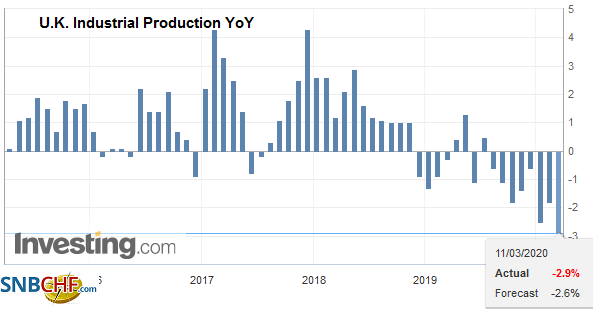

| Covid-19 is casting a pall over the UK’s budget that will be presented by Chancellor of the Exchequer Sunak about an hour before the US equity market opens. The budget is expected to boost infrastructure spending, in part to help prepare the UK for leaving exiting the standstill agreement with the EU at the end of the year. More spending on the National Health Service has been promised. A tougher stand on immigration is expected. A cap or a cut in taxes has been suggested. Data reported today was mostly weaker than expected with the January GDP flat (economists had expected a 0.1% gain). Industrial output slipped by 0.1%, and the median forecast in the Bloomberg survey called for a 0.3% increase.Services underperformed, and construction saw a 0.8% decline instead of a 0.1% gain that had been forecast. On the other hand, the January trade surplus (GBP4.2 bln) was considerably better than the small deficit anticipated. |

U.K. Industrial Production YoY, January 2020(see more posts on U.K. Industrial Production, ) Source: investing.com - Click to enlarge |

ECB President Lagarde held an emergency call with EMU leaders and central bankers and pleaded with officials to deliver rapid fiscal support. Italy, the hardest hit by the coronavirus outside of China, is taking Lagarde’s plea to heart and appears to be more than doubling its existing package of support to 25 bln euros. The ECB policy meeting is tomorrow, and dramatic action is expected to include a cut in rates, more asset purchases, and some adjustment to the long-term loan facility (TLTRO) that could target lending to small and medium-sized businesses on more friendly terms. There is also some thought to adjust the tiering (application of negative rates to deposits at the ECB), which, if Swiss or Danish ratios are adopted, billions of euros may be freed up for the creditor banks.

The euro held yesterday’s low near $1.1275 and traded up to about $1.1365 in late Asia before easing in the European morning back to $1.13, where new bids were found. There is an option for a billion euros struck there that expires today, and 1.2 bln euro option there expires on Friday. The $1.1360 area corresponds to a (38.2%) retracement of the pullback from the week’s high near $1.15, and $1.1385 is the next (50%) retracement. The intraday technicals appear to favor the upside in the North American morning. Sterling reached $1.32 on Monday and a low after the BOE surprise move of around $1.2830. With its recovery, it has retraced (38.2%) of the decline near $1.2975. The next retracement is found $1.3015. However, the intraday technicals are not as supportive as they are for the euro.

America

The US seems to be trailing as much as a few weeks behind many other countries in testing, social distancing, and preparing for the high risk of broad contagion. Containment has given way to mitigation. As trial truly gets underway, the number of US cases is bound to rise sharply. Trump seems to be trying to get congressional support for a payroll savings tax, which is used primarily to fund Social Security. Currently, employees and employers each pay 6.2% on up to $137k in salary for Social Security. Another 1.45% is paid both parties for Medicare. A two percentage point cut for employees, like Obama pushed through in 2010, would cut about $150 bln, if employers were included, it would be $300 bln. Congressional Democrats seem to prefer legislating sick leave pay. Nearly a quarter of Americans do not have paid sick leave, mostly employed by small and medium-sized businesses. The Democrats also are talking about extending unemployment insurance.

Some in Congress representing oil-producing areas are talking about support for the shale industry. Like Saudi Arabia and Russia, the key is not the cost of actually bringing a barrel of black gold from the bowels of the earth, but to cover fixed costs. In Russia and Saudi Arabia, those fixed costs come from government spending. For the shale producers, it is in the form of debt servicing. In recent years, the US budget agreement between the Republicans and Democrats was made possible by oil sales from the US Strategic Petroleum Reserves. The US was to auction 12 mln barrels to raise $450 mln for the FY20 budget.The bids were due today, but yesterday the Trump Administration suspended the auction. The FY21 budget proposals call for the sale of 15 mln barrels.

US oil inventories are rising. API estimated a 6.4 mln barrel increase last week. The EIA estimate is regarded as more accurate, and according to it, oil inventories are growing about 25% faster than a year ago through the first nine weeks of the year. Meanwhile, Saudi Arabia has indicated it will sell oil out of its inventories as an apparent signal of its intent. Russia claimed it could boost output by 200k-300k bpd in the near-term and as much as 500k bpd over the medium-term. If they both have to tap their sovereign wealth funds, the Saudis would likely have to sell Treasuries, while Russia has already divested most of its Treasuries, though it is believed to be a large holder of Chinese bonds. Meanwhile, for some countries, this might be a good time to build or add on to strategic oil reserves. The next OPEC+ meeting will be held in May or June, and a new deal should not be ruled out quite yet. Meanwhile, Mexico’s Finance Minister indicated that the country’s income has been fully protected by its oil hedges and that he was more concerned about the virus than the drop in oil prices.

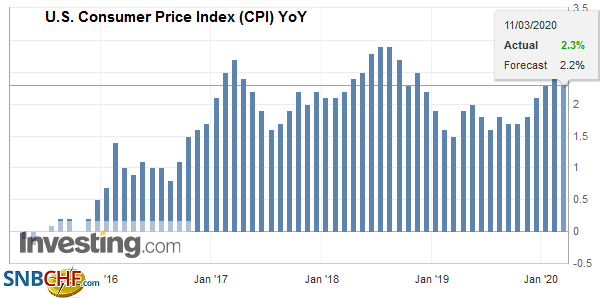

| The US reports February CPI figures. They will draw passing interest. The headline is expected to be flat, which given the base effect, means that the year-over-year rate can ease to 2.2% from 2.5%. The core rate may see a 0.2% rise on the month, which would keep the year-over-year rate steady at 2.3%. |

U.S. Consumer Price Index (CPI) YoY, February 2020(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

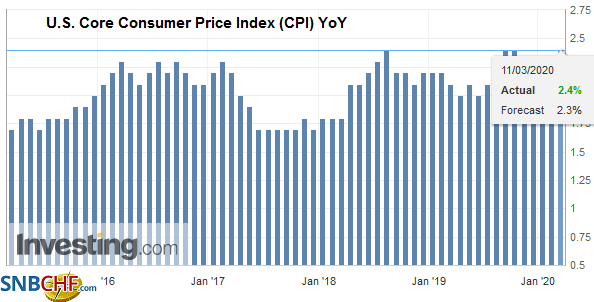

| The data will likely have little impact as the broader risk appetite is key, and investors look toward next week’s FOMC meeting, where the market has settled on 75 bp rate cut as the most likely scenario. Separately, Canada is expected to unveil its fiscal response, which is likely to include, among other things, quicker access to unemployment benefits. |

U.S. Core Consumer Price Index (CPI) YoY, February 2020(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The US dollar traded between CAD1.36 and CAD1.38 yesterday and is hovering around the middle of that range today. A tighter range of CAD1.3650-CAD1.3750 appears to be the focus. The US dollar is firm against the Mexican peso and is near yesterday’s high (~MXN21.09). Ideas that Banxico will intervene through its fx swap facility appears to be deflecting some speculation. A move above MXN21.12 could spur a move toward MXN21.40.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Bank of England,COVID-19,Currency Movement,Featured,newsletter,OIL