[This article is part of the Understanding Money Mechanics series, by Robert P. Murphy. The series will be published as a book in late 2020.] In addition to the Keynesian perspective (covered in chapter 14), a relatively new challenge to the Austrian framework comes from the “market monetarists” and their endorsement of a central bank policy of “level targeting” of nominal gross domestic product (sometimes abbreviated as NGDPLT1). Although not as widespread as the Keynesian paradigm, market monetarism is arguably a more serious competitor to the Austrian school when it comes to monetary theory and business cycle analysis, because many of the leaders of the new approach are self-described libertarians with positions at free market organizations. The most obvious

Topics:

Robert P. Murphy considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

[This article is part of the Understanding Money Mechanics series, by Robert P. Murphy. The series will be published as a book in late 2020.]

In addition to the Keynesian perspective (covered in chapter 14), a relatively new challenge to the Austrian framework comes from the “market monetarists” and their endorsement of a central bank policy of “level targeting” of nominal gross domestic product (sometimes abbreviated as NGDPLT1). Although not as widespread as the Keynesian paradigm, market monetarism is arguably a more serious competitor to the Austrian school when it comes to monetary theory and business cycle analysis, because many of the leaders of the new approach are self-described libertarians with positions at free market organizations.

The most obvious example is Scott Sumner—the undisputed leader of the market monetarists—who has an economics PhD from the University of Chicago and occupies (as of this writing) the Ralph G. Hawtrey Chair of Monetary Policy at the Mercatus Center at George Mason University. In addition, Sumner is one of a handful of regular contributors at Liberty Fund’s popular economics blog, EconLog.

Although Sumner himself is modest and points to precursors in the academic literature, in his online writings over the years he almost single-handedly convinced many fans of the free market that the severity of the Great Recession was not the inevitable fallout from malinvestments made during the housing boom, but instead was due to the Federal Reserve’s tight monetary policy from 2008 onward.

Although Sumner himself is modest and points to precursors in the academic literature, in his online writings over the years he almost single-handedly convinced many fans of the free market that the severity of the Great Recession was not the inevitable fallout from malinvestments made during the housing boom, but instead was due to the Federal Reserve’s tight monetary policy from 2008 onward.In light of the standard Austrian view of the business cycle in general (summarized in chapter 8) and the housing boom in particular (summarized in chapter 11), it would be an understatement to say that the market monetarist approach differs dramatically in both its diagnosis and prescription. Inasmuch as the market monetarists have gained supporters who might otherwise have endorsed the Austrian view of recessions, it is important for the current volume to critically assess this new paradigm. For concreteness, this chapter focuses specifically on Sumner’s work, but the treatment is applicable to the entire market monetarism approach.

The Legacy of Milton Friedman’s Monetarism

In order to understand Sumner’s approach—including the very label “market monetarism”—it is necessary to first review some of the work of Milton Friedman, the famous Chicago school economist closely associated with monetarism.2

After the Great Depression, the standard Keynesian view (as we explained in chapter 14) was that aggressive monetary policy—at least as conventionally conceived—had been tried but had failed. After all, during the early 1930s central banks rapidly expanded their asset purchases while slashing interest rates to very low levels. Yet this apparently “easy money” policy didn’t resuscitate aggregate demand and restore full employment, leading the Keynesians to conclude that the global economy was stuck in a “liquidity trap” requiring budget deficits to escape. In the famous metaphor, the Keynesian assessment of the Great Depression was that central banks had been “pushing on a string.”

Milton Friedman and Anna Schwartz overturned this consensus with their famous 1963 book A Monetary History of the United States, 1867–1960. The chapter in the book dealing with the Great Depression years was also published as a separate volume entitled The Great Contraction: 1929–1933.

In contrast to the standard view that the Fed had tried a loose monetary policy that was impotent, Friedman and Schwartz argued that the Federal Reserve had actually adopted a tight policy. Specifically, even though the Fed expanded the monetary base by some 20 percent from 1929–33,3 a broader measure of money—M2—had nonetheless declined by a third over this period. (Recall that this was a period of bank runs, when depositors were rushing to withdraw their funds from the banks. In a fractional reserve system, mass withdrawals from banks will cause M1 and M2 to decline, even if the central bank doesn’t itself “tighten.”) It is not surprising, Friedman and Schwartz argued, that consumer prices and real output collapsed when the Fed allowed the overall money stock (used by the public) to drop so rapidly.

In contrast to the standard view that the Fed had tried a loose monetary policy that was impotent, Friedman and Schwartz argued that the Federal Reserve had actually adopted a tight policy. Specifically, even though the Fed expanded the monetary base by some 20 percent from 1929–33,3 a broader measure of money—M2—had nonetheless declined by a third over this period. (Recall that this was a period of bank runs, when depositors were rushing to withdraw their funds from the banks. In a fractional reserve system, mass withdrawals from banks will cause M1 and M2 to decline, even if the central bank doesn’t itself “tighten.”) It is not surprising, Friedman and Schwartz argued, that consumer prices and real output collapsed when the Fed allowed the overall money stock (used by the public) to drop so rapidly.Just as the low interest rates of the 1930s were not a sign of loose money, Friedman argued that high interest rates were not necessarily a sign of tight money, either. In a 1997 article for the Wall Street Journal,4 he recommended that the Bank of Japan increase the rate of monetary growth to stimulate its lackluster economy, and then argued:

Initially, higher monetary growth would reduce short-term interest rates even further. However, as the economy revives, interest rates would start to rise. That is the standard pattern and explains why it is so misleading to judge monetary policy by interest rates. Low interest rates are generally a sign that money has been tight, as in Japan; high interest rates, that money has been easy. [Friedman 1997, bold added.]

Friedman then tied the lesson back to his view of the Great Depression:

The Fed [in the early 1930s] pointed to low interest rates as evidence that it was following an easy money policy and never mentioned the quantity of money. The governor of the Bank of Japan…referred to the “drastic monetary measures” that the bank took in 1995 as evidence of “the easy stance of monetary policy.” He too did not mention the quantity of money. Judged by the discount rate, which was reduced to 0.5% from 1.75%, the measures were drastic. Judged by monetary growth, they were too little too late, raising monetary growth from 1.5% a year in the prior three and a half years to only 3.25% in the next two and a half.

After the U.S. experience during the Great Depression, and after inflation and rising interest rates in the ’70s and disinflation and falling interest rates in the ’80s, I thought the fallacy of identifying tight money with high interest rates and easy money with low interest rates was dead. Apparently, old fallacies never die. [Friedman 1997, bold added.]

Being trained at the University of Chicago himself, Scott Sumner is an expert on the legacy of Milton Friedman. Sumner believes that he is doing for the interpretation of the Great Recession what Friedman (and Schwartz) did for the Great Depression.

Scott Sumner’s Market Monetarism

As we documented in chapter 7, after the global financial crisis struck in the fall of 2008, the Fed unveiled a variety of new lending programs, slashed its policy rate to virtually zero, and doubled the monetary base—all in a matter of months. In light of these unprecedented actions, both economists and the general public understandably concluded that the Fed was engaged in a very easy money policy.

Yet Scott Sumner—starting at his lonely blog—managed to eventually convert a large portion of the profession to his startling claim that the Great Recession was caused by tight money. A full account of his argument is linked in the endnotes,5 but we can summarize his argument as follows:

- Just as Milton Friedman taught, it is misleading to look at the Fed’s (virtually) zero percent interest rates, or massive expansion of the monetary base, as indicating easy money from late 2008 onward.

- Instead, we should look at a much better indicator, namely the growth rate of nominal gross domestic product (NGDP). That is, economists should look at the growth in final spending on goods and services (without adjusting for price inflation) to assess whether monetary policy has been too easy or too tight. As Sumner argued in mid-2009:

Between the early 1990s and 2007, NGDP grew at just over five percent per year. Because the real GDP growth rate averaged nearly three percent, we ended up with a bit more than two percent inflation, which was widely believed to be the Fed’s implicit target. Beginning around August 2008, however, NGDP slowed sharply, and then fell at a rate of more than four percent over the following several quarters. Indeed the decline in NGDP during 2009 is likely to be the steepest since 1938. This produced what may end up being the deepest and most prolonged recession since 1938. [Sumner 2009]6

- The reason Sumner believes that a drop in the growth rate—let alone an actual decline—in “nominal spending” is so damaging, is that wages and some other prices are “sticky,” at least in the short to medium run. In Sumner’s words:

as of early 2008 the U.S. economy featured many wage and debt contracts negotiated under the expectation that NGDP would keep growing at about five percent per year. Because nominal GDP is essentially total national gross income, if it falls sharply it becomes much harder for debtors to repay loans, and much harder for companies to pay wages and salaries. The almost inevitable consequence is that unemployment rises sharply, and debt default rates soar. [Sumner 2009]

- Rather than focus on interest rate or monetary growth targets, Sumner instead recommends that the Fed adjust policy such that NGDP grows at 5 percent per year. In a typical year, this 5 percent growth would be composed of 3 percent real GDP growth and 2 percent price inflation. However, if there were a recession and real output dropped by a percentage point (i.e., real GDP growth of –1 percent), then Sumner would still insist that total nominal spending grow by 5 percent that year, meaning that now price inflation would have to be 6 percent.

- Furthermore, Sumner advocates a “level target,” meaning that if the Fed misses its target and NGDP grows at, say, only 3 percent in one year, then it must grow at 7 percent the next in order for the level of NGDP in the second year to catch up to where it should have been. Hence the official title of Sumner’s proposal: NGDPLT.

- The final subtlety is that Sumner argues that the right time to gauge Fed policy is immediately, according to the market’s expectation. In other words, Sumner doesn’t want the Fed to look backwards over the course of twelve months to see if NGDP in fact grew at the target 5 percent. Rather, Sumner wants Fed officials to look at a “futures market” in NGDP contracts to see what investors predict the level of NGDP will be twelve months from now. If the expected growth rate of NGDP is different from the 5 percent target, then the Fed can “passively” expand or contract its balance sheet in order to move expected future NGDP in the right direction.

- Because of Sumner’s similarity to Friedman, and because of his proposal to use a futures market in NGDP contracts to effectively automate Fed policy, Sumner’s framework was eventually dubbed (by a fan) “market monetarism.”

It would be difficult to overstate Sumner’s personal role in elevating market monetarism from a heretical notion in late 2008 to a set of ideas being seriously discussed by central bankers (as well as economics bloggers). Indeed, after a press conference in which Fed chair Ben Bernanke announced (what would be called) the beginning of QE3 and mentioned NGDP targeting, George Mason University economist Tyler Cowen declared it “Scott Sumner day.”7

Problems with Market Monetarism

For the purposes of this primer on money mechanics, we will only sketch some of the problems with the market monetarist framework. The following considerations are not offered as an exhaustive critique.

| Problem No. 1: Monetary Growth Accelerated after the 2008 Crisis

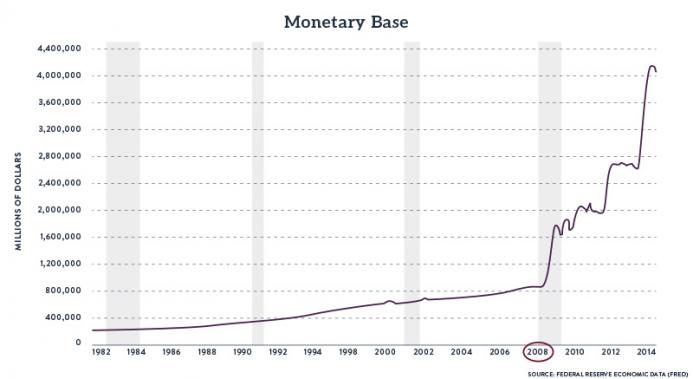

Remember that the original Friedman and Schwartz revisionism concerning the causes of the Great Depression was their observation that the Fed, though it expanded the monetary base after the 1929 stock market crash, didn’t inflate enough to offset the bank runs. According to them, the Fed’s blunder was allowing M2 to collapse by a third from 1929–32. But there is no analogy between this critique of the Fed’s behavior regarding the 2008 crisis, and the ensuing Great Recession. First, let’s document just how aggressively the Fed expanded the monetary base when the crisis struck in the fall of 2008: |

Monetary Base, 1982-2014 - Click to enlarge |

| Not only did Bernanke’s Fed engage in a jaw-dropping injection of base money in response to the panic, but the admittedly tepid base growth in 2007 is not something that most observers would have predicted would lead to a global financial panic. (Although not shown on this chart, the monetary base actually shrank in the early 1960s—in contrast, its twelve-month growth never went negative in 2007 or 2008—and yet this didn’t lead to the worst crisis since the Great Depression during the 1960s.)

Notwithstanding the Fed’s handling of the monetary base, one might suppose that M1 and M2 collapsed on Bernanke’s watch—just as Friedman and Schwartz pointed out happened in the early 1930s. Yet on the contrary, both the M1 and M2 measures of the money stock continued to grow after the crisis struck, particularly M1: |

M1 Money Stock, 1980-2020 - Click to enlarge |

| Finally, let us chart the precise metric that Friedman and Schwartz used when giving their “monetarist” explanation of the Great Depression—that the growth in M2 collapsed, and in fact went sharply negative. Do we see anything comparable with the financial crisis of 2008?

The chart above shows the twelve-month percentage change in the M2 monetary aggregate. It clearly shows that there was nothing unusual about the “growth rate of money in the hands of the public” before or during the crisis, with the M2 growth rate only dropping sharply after the Great Recession had officially ended (i.e., to the right of the gray bar). Furthermore, the above chart shows that the M2 growth rate really did fall substantially in the early 1990s. If one were to adopt the Friedman and Schwartz framework—which explained the Great Depression as a collapse in M2 growth—then this modern chart would lead to the “obvious” conclusion that the financial crisis and ensuing Great Recession began in 1995. And yet, that obviously didn’t happen. |

M2 Money Stock, 1985-2020 - Click to enlarge |

| As the above charts indicate, Scott Sumner’s explanation for the financial crisis and Great Recession shouldn’t be labeled “monetarist” at all. There is no sense in which these events can be blamed on Bernanke’s unwillingness to boost the money stock, however measured. (And for what it’s worth, in 2008 Anna Schwartz herself blamed the financial crisis on the Fed for blowing up the housing bubble!8)

Problem No. 2: Sumner’s “NGDP Growth” Criterion Is Vacuous and (Almost) Nonfalsifiable Of course, Sumner and other market monetarists would object to the discussion in the previous section by explaining that their preferred criterion for assessing the Fed’s “tightness” or “looseness” is not any particular monetary aggregate, but instead the growth rate of nominal GDP. Since the Fed allowed NGDP growth to (eventually) collapse, Sumner argues that by definition this is a “tight” central bank policy. |

One-Year Growth Rate in M2, 1985-2020 - Click to enlarge |

The fundamental problem with this definition is that it assumes Sumner’s conclusion. One of the very issues under dispute is whether aggressive monetary expansion by the central bank is medicine or poison for an economy entering recession. If the Austrian analysis of boom-bust cycles (given in chapter 8) is correct, then the Fed’s actions from 2008 onward only generated another unsustainable boom. Sumner’s rhetorical device of framing inadequate NGDP growth as “tight money” by definition would make it impossible to learn whether his policy advice is simply wrong.

Consider a medical analogy: suppose a patient is suffering from fever, running a temperature of 103 degrees. One group of doctors recommends injecting the patient with substance M, in order to cure the fever. Yet another group of doctors argues that past injections of substance M are what made the patient sick in the first place.

Now, if they are to have any hope of resolving this dispute, how should the doctors measure the amount of substance M being injected into the patient? Most people would argue that the doctors should look at absolute physical measurements, involving the volume and/or rate of injection. And so, for example, if they injected the patient with more M than had ever been administered to any patient in the history of that hospital, it would be odd if the patient’s chart read, “Received a very restrictive treatment of M.”

Indeed, imagine if the doctors who think that substance M is a helpful medicine wanted to define the M treatment in terms of the fever. That is, if after they had injected the patient with unprecedented amounts of M, whether the fever stayed the same or went up, the doctors were to declare, “We just made the patient sicker with our shift to restrict the M treatment.” This would be Orwellian and obviously would make it virtually impossible to figure out whether more or less M was what the patient needed.

As a final demonstration of how Sumner’s framework is (virtually) nonfalsifiable, consider his January 20209 declaration in a blog post:

We are entering a golden age of central banking, where the Fed will become more effective and come closer to hitting its targets than at any other time in history. Over the next few decades, inflation will stay close to 2% and the unemployment rate will generally be relatively low and stable….

In fact, Fed policy is becoming more effective because it is edging gradually in a market monetarist direction…

If they continue moving in this direction, then NGDP growth will continue to become more stable, the business cycle will continue to moderate, inflation will stay in the low single digits, and unemployment will stay relatively low and stable….

As an analogy, when I was young I would frequently read about airliners crashing in the US…After each crash, problems were fixed and planes got a bit safer.

Recessions and airline crashes: They are getting less frequent, and for the exact same reason. [Sumner 2020, bold added.]

Most Austrian readers would view Sumner’s predictions as incredibly off the mark. And yet, it will be hard for Sumner’s rosy compliments for the Fed to be falsified.

For example, suppose that at some point the economy crashes and the unemployment rate surges while the Fed engages in continued rounds of QE to “fix it.” In particular, suppose that in an especially terrible year unemployment jumps to 20 percent, real (i.e., inflation-adjusted) GDP drops by 15 percent, and the official Consumer Price Index (CPI) surges by 10 percent. In the midst of such terrible “stagflation,” the Austrians run victory laps, arguing that underlying “structural” malinvestments can’t be fixed by the printing press. The combination of high unemployment and high consumer price inflation shows—so our Austrians would claim—that loose money sinks economies.

Yet in our hypothetical scenario, Sumner would also claim victory. He would point out that when real GDP drops 15 percent while the price level only rises by 10 percent, nominal GDP falls by (roughly) 5 percent. Since Sumner recommended that the Fed keep NGDP growing at 5 percent, this horrible fall in NGDP—so Sumner would claim—was the culprit. Once again, the Fed’s “tight money” has caused another economic disaster.

Problem No. 3: Market Monetarists Take Their (Simplistic) Model Too Seriously

One illustration of this problem is the tendency for market monetarists to conflate “NGDP” with “total spending.”10 Yet there is much more “total spending” in the economy than what is spent on final goods and services. Even if we put aside the entire financial sector—and note that the standard Sumnerian model doesn’t have a stock market or even banks, with Sumner actually arguing that putting banks in a model of the business cycle will only confuse matters11—the bulk of “total spending” in the economy is actually on intermediate purchases of goods, which are ignored in calculations of GDP in order to avoid “double counting.”

Normally, the conflation of “total spending” with “spending on final goods and services” might not be a huge problem in terms of policy advice, though it’s conceivable that a change in economic organization (perhaps with industries becoming more or less “vertically integrated”) could render the Fed’s stance “tight” according to one metric but “easy” according to the other. The more fundamental problem is that Sumner’s model ignores the entire capital structure of the economy, which blinds him to the very possibility of the Austrians being right.

Another illustration of the market monetarists taking their models too seriously is Sumner’s continued claims that participants in the market had expectations about NGDP growth. For example, when explaining why the Fed’s (allegedly) tight policy in 2008 caused the crisis, he argues that “as of early 2008 the U.S. economy featured many wage and debt contracts negotiated under the expectation that NGDP would keep growing at about five percent per year.”

This is obviously a false claim. Barely anybody in the US knew what NGDP was in early 2008; they certainly didn’t accept job offers or take out mortgages with expectations of NGDP growth in mind. To be sure, Sumner could rehabilitate his claim in terms of individual expectations of personal income growth, but the point still stands that Sumner has an unfortunate habit of confusing his (simplistic) model of the economy for the real world. This makes it difficult for him to even see contrary evidence.

Problem No. 4: Central Bank Actions Distort Relative Prices and Have “Real” Impacts

From an Austrian perspective, the previous objections are mere quibbles; the fundamental problem with the market monetarist approach is that its policy recommendations would simply perpetuate the boom-bust cycle.

Sumner quite consciously eschews analysis of interest rates, viewing them as “misleading” indicators of the stance of monetary policy. Yet if the Austrians are correct, then if the Fed reacts to a downturn (which normally would go hand-in-hand with a fall in NGDP growth) with monetary expansion, then, besides the impact on aggregate nominal variables, this action will also distort relative prices. In particular, short-term interest rates will typically be pushed below their “natural” levels, giving the wrong signal to entrepreneurs and setting in motion another unsustainable boom.

Even on Sumner’s own terms, it is unclear how his recommended policies are supposed to fix the alleged problem. For example, Sumner claims that in late 2008, the collapse in nominal income growth meant that millions of workers—stuck in employment contracts and mortgages with “sticky” numbers in them—no longer had enough money coming in each month to pay their bills. So if in response the Fed creates trillions of new dollars in base money by buying government bonds and other financial assets, how exactly does this help those millions of wage earners? Injecting new money into the hands of the financially savvy and politically connected, if anything, makes those humble wage earners even worse off, as commodity prices instantly respond to the rounds of QE while the workers’ “sticky” hourly wages do not rise nearly as quickly.

Indeed, the entire “sticky prices” boogeyman is a red herring. During the 1920–21 depression, consumer prices collapsed more rapidly than in any twelve-month stretch during the Great Depression.12 Yet the 1920s were not a decade of economic stagnation. Blaming the worst economic crises in US history on “deflation” and “sticky prices” doesn’t fit the facts.

- 1. See, for example, David Beckworth, “Facts, Fears, and Functionality of NGDP Level Targeting: A Guide to a Popular Framework for Monetary Policy” (Mercatus Special Study, Mercatus Center at George Mason University, Arlington, VA, September 2019), https://www.mercatus.org/publications/monetary-policy/facts-fears-and-functionality-ngdp-level-targeting.

- 2. See Bennett T. McCallum, “Monetarism,” Library of Economics and Liberty, Liberty Fund, Inc., accessed Mar. 9, 2020, https://www.econlib.org/library/Enc/Monetarism.html.

- 3. See Sumner’s summary of Friedman and Schwartz’s view of the Great Contraction: Scott Sumner, “Milton Friedman Argued That the Great Depression Occurred Despite Massive QE,” EconLog (blog), Library of Economics and Liberty, Apr. 3, 2015, https://www.econlib.org/archives/2015/04/milton_friedman_15.html.

- 4. Milton Friedman, “Rx for Japan: Back to the Future,” Wall Street Journal, Dec. 17, 1997, available at https://miltonfriedman.hoover.org/friedman_images/Collections/2016c21/WSJ_12_17_1997.pdf.

- 5. Sumner lays out his position in a 2009 Cato Unbound series of essays: “The Real Problem Was Nominal,” “Almost on the Money: Replies to Hamilton, Selgin, and Hummel,” “From Discretion to Futures Targeting, One Step at a Time,” “Score-Keeping with Selgin,” “Clearing Up Some Miscommunication,” “Defining the Stance of Monetary Policy Is Harder Than It Looks,” “We Can’t Agree on Everything, George [Selgin]…,” and “Final Thoughts and Thanks,” all in Cato Unbound, September 2009, https://www.cato-unbound.org/issues/september-2009/monetary-lessons-not-so-great-depression.

- 6. The Sumner quotation is from the 2009 Cato Unbound opening essay: “The Real Problem Was Nominal,” Cato Unbound, September 2009, https://www.cato-unbound.org/2009/09/14/scott-sumner/real-problem-was-nominal.

- 7. Tyler Cowen, “It’s Not Just Monetary Policy, It’s Scott Sumner Day,” Marginal Revolution (blog), Sept. 13, 2012, https://marginalrevolution.com/marginalrevolution/2012/09/its-not-just-monetary-policy-its-scott-sumner-day.html.

- 8. Sumner acknowledges Schwartz’s apparent about-face and late found agreement with the Austrians: “Friedman and Schwartz vs. the Austrians,” The Money Illusion (blog), Jan. 16, 2020, https://www.themoneyillusion.com/friedman-and-schwartz-vs-the-austrians/#more-203.

- 9. See Sumner, “Fed Policy: The Golden Age Begins,” The Money Illusion (blog), Feb. 17, 2009, https://www.themoneyillusion.com/fed-policy-the-golden-age-begins/.

- 10. For example, Sumner himself refers to “nominal spending” as the item that the Fed allowed to collapse in his original Cato Unbound essay, while George Selgin in his initial response essay writes, “Like [Sumner], I believe that monetary policy should strive, not to achieve any particular values of interest rates, employment, or inflation, but simply to maintain a steady growth rate of overall nominal spending.” See Sumner, “The Real Problem Was Nominal,” and George Selgin, “Between Fulsomeness and Pettifoggery: A Reply to Sumner,” Cato Unbound, September 2009, https://www.cato-unbound.org/2009/09/18/george-selgin/between-fulsomeness-pettifoggery-reply-sumner.

- 11. Sumner literally titled a blog post, “Keep banks out of macro.” See “Keep Banks out of Macro,” The Money Illusion (blog), Jan. 22, 2013, https://www.themoneyillusion.com/keep-banks-out-of-macro/.

- 12. For more on the 1920–21 depression and how it explodes the monetarist explanation of the Great Depression, see: Robert P. Murphy, “The Depression You’ve Never Heard of: 1920–1921,” Foundation for Economic Education, Nov. 18, 2009, https://fee.org/articles/the-depression-youve-never-heard-of-1920-1921/.

Tags: Featured,newsletter