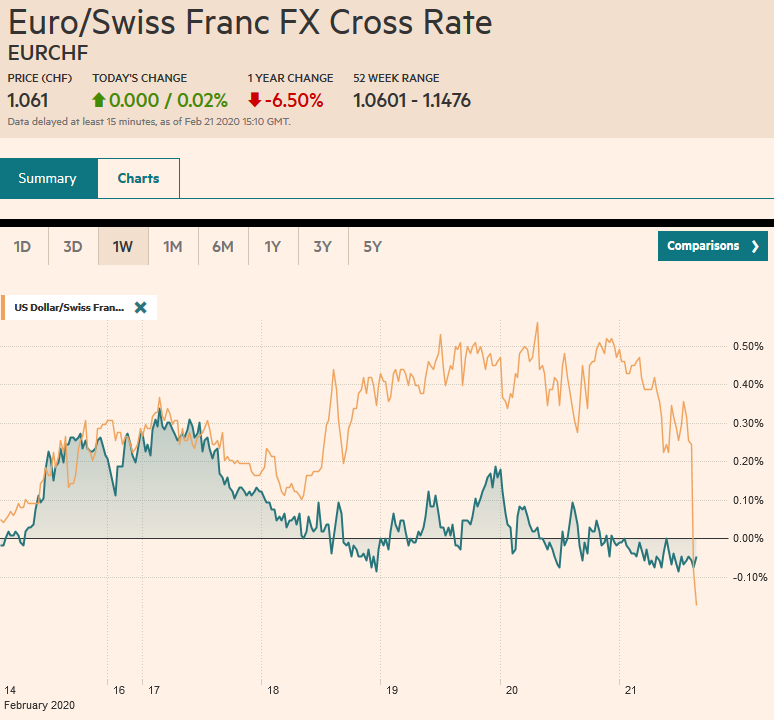

Swiss Franc The Euro has risen by 0.02% to 1.061 EUR/CHF and USD/CHF, February 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft..com - Click to enlarge FX Rates Overview: The spread of Covid-19 outside of China and early signs of the economic consequences again emerged to weigh on investor sentiment. Poor Japanese and Australian preliminary February PMI reports and some trade indications from South Korea saw most Asia Pacific equities sell-off. China was an exception. The small gain (0.3%), lifted the Shanghai Composite 4.2% on the week. Australia’s benchmark also managed to eke out a minor gain (~0.12%) for the week after absorbing today’s (0.33%) loss. Europe’s Dow Jones Stoxx 600 was nearly flat for the week coming into today’s session, and

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movement, EMU, Featured, Japan, Korea, Mexico, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.02% to 1.061 |

EUR/CHF and USD/CHF, February 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft..com - Click to enlarge |

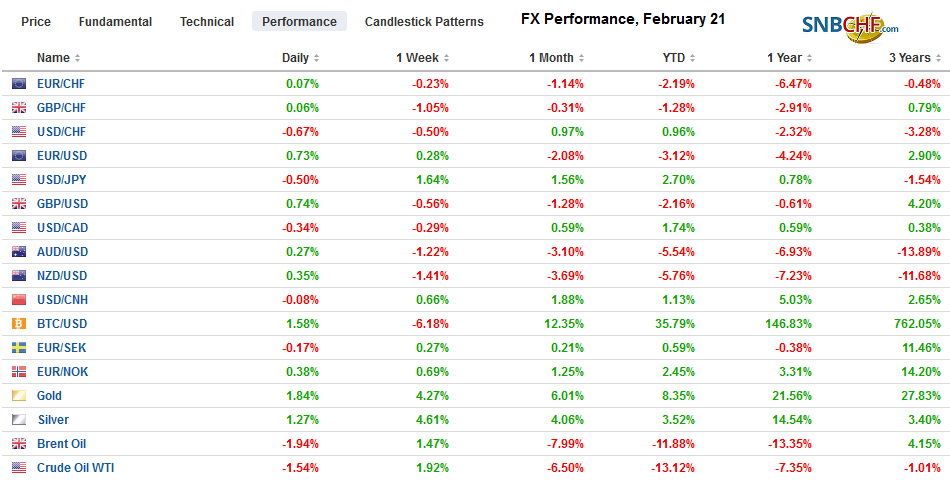

FX RatesOverview: The spread of Covid-19 outside of China and early signs of the economic consequences again emerged to weigh on investor sentiment. Poor Japanese and Australian preliminary February PMI reports and some trade indications from South Korea saw most Asia Pacific equities sell-off. China was an exception. The small gain (0.3%), lifted the Shanghai Composite 4.2% on the week. Australia’s benchmark also managed to eke out a minor gain (~0.12%) for the week after absorbing today’s (0.33%) loss. Europe’s Dow Jones Stoxx 600 was nearly flat for the week coming into today’s session, and despite better than expected PMI news, it is off about 0.35% in late morning turnover. It had gained about 4.8% in the previous two weeks. The S&P 500 staged an impressive rally as once again, the pullback was bought. However, US shares are trading lower, with the S&P 500 trading near yesterday’s lows. Asia Pacific bond yields tumbled, partly as catch-up, and partly driven by local data. European bond yields are a little lower, and the 10-year US Treasury yield has fallen below 1.50% for the first time since last September. The US dollar is mostly softer, with the Australian and New Zealand dollars are main exceptions, nursing about a 0.3% loss. Although the yen’s typically drivers appeared to breakdown earlier this week, relationships appeared to return to status quo ante with lower US Treasury yields and weakness in equities underpinning the yen, whose roughly 0.3% gain is leading the majors. Gold is on fire. It is at new 7-year highs near $1635 to bring this week’s gain to about $50 a little more than 3%. Oil prices lower, and the WTI for April delivery is halving this week’s gains to about 1.4%. |

FX Performance, February 21 - Click to enlarge |

Asia Pacific

The steepness of Japan’s Q4 contraction, 1.6% quarter-over-quarter, and the disruption of supply chains of people (Chinese tourists) and goods (supply chains) has fanned fears that the recovery is put off until Q2. The preliminary PMI, though it does not have a long history, has a somber message. Manufacturing stands at 47.6 down from 48.8. Here the weakness was exacerbated. Mild strength in services (51.0) turned south in a big way (46.7). The composite reading fell to 47.0 from 50.1. The fragile recovery from Q4 shattered. BOJ Governor Kuroda quickly said it was not time to think of additional stimulus. Separately, Japan’s January CPI figures were little changed. The headline year-over-year rate slipped to 0.7% from 0.8%, while the core rate (excludes fresh food) did just the opposite.

The Australian dollar has been sold aggressively as growth concerns escalated given the wildfires and the disruption caused by the coronavirus. The February PMI confirmed these investor fears. Even though the manufacturing PMI actually rose (49.8 vs. 49.6), the decline in the services PMI (48.4 vs. 50.6) more than offset it. The composite fell to 48.3 from 50.2. Last year it averaged 50.5, though it was below the 50 boom/bust level in November and December.

South Korea’s trade figures for the first 20-days of February give a sense of the dramatic disruption taking place. South Korea’s average daily shipments during the period were 9.3% lower than a year ago. Overall, exports to China were off 3.7%, even though there were more working days. Imports from China dropped by 19%. Overall, South Korean exports rose 12% year-over-year, but this figure is distorted by the calendar effect, which added three working days compared to a year ago.

The dollar tested JPY112.20 yesterday and pulled back to around JPY111.50 today. The JPY111.30 area corresponds with a (38.2%) retracement objective of this week’s surge. However, the intraday technicals warn that the washout may not be completed and that the North American market may retest the JPY112.00 area. There is a $625 mln option struck there that expires today. It is the third consecutive weekly advance for the dollar, the longest since October. The Australian dollar is down for the fourth straight session. The last time it finished the North American session with a gain was on February 12. It has been sold below $0.6600 today to fresh ten-year lows. The Chinese yuan has also weakened for a fourth consecutive session today, and today’s loss brings the week’s decline to about 0.65%. The greenback briefly traded above CNY7.04 for the first time since mid-December.

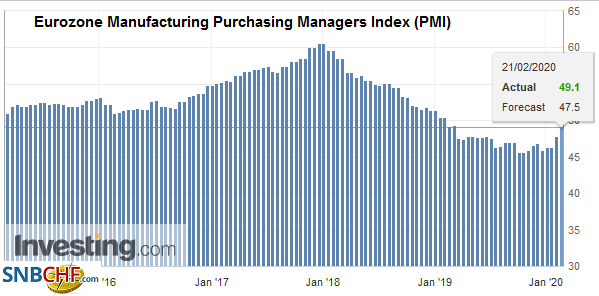

EuropeThe eurozone flash PMI was better than expected. Still, the soft data can only dop so much for the sentiment after the large collapse in the real sector (industrial output) in December. German manufacturing contraction slowed, and the February PMI manufacturing PMI rose to 47.8 from 45.3. The service PMI softened to 53.3 from 54.2. |

Eurozone Manufacturing Purchasing Managers Index (PMI), February 2020(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The compositing reading ticked to 51.1 from 51.2, which was still better than decline economists had forecast. In France, the manufacturing PMI disappointed, falling to 49.7 from 51.1. The services PMI was resilient, rising to 52.6 from 51.0. This resulted in the composite improving to 51.9 from 51.1. |

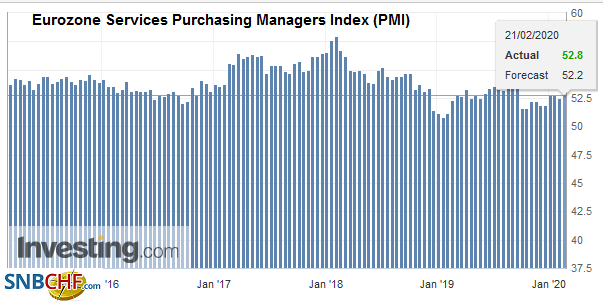

Eurozone Services Purchasing Managers Index (PMI), February 2020(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

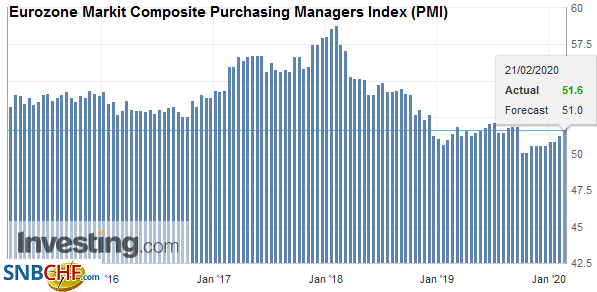

| The aggregate figures for the eurozone were better than expected, and new orders edged higher, despite softer foreign demand. The resilience of the labor market is also a constructive sign. The manufacturing PMI was at 47.9 in January and is now at 49.1. A year ago, it was at 49.3. The services PMI rose to 52.8 from 52.5 and matches the year-ago level. The composite was expected to slip to 51.0 from 51.3 in January but instead rose to 51.6. In February 2019, it was at 51.9. |

Eurozone Markit Composite Purchasing Managers Index (PMI), February 2020(see more posts on Eurozone Markit Composite PMI, ) Source: investing.com - Click to enlarge |

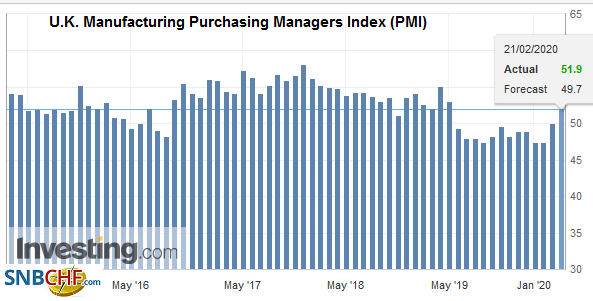

| The UK preliminary February PMI is consistent with recent data suggesting that after stagnating in Q4, the British economy is faring better at the start of 2020. The manufacturing PMI moved back above the 50 boom/bust level to 51.9, which was better than expected. The service PMI slipped to 53.3 from 53.9. The net effect was to leave the composite unchanged at 53.3. Economists had forecast a decline. |

U.K. Manufacturing Purchasing Managers Index (PMI), February 2020(see more posts on U.K. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The euro is trading just inside yesterday’s range. Just above $1.08, the euro is off about 0.25% for the week. It has risen in only one week so far this year, and that was the last week of January. It is carved out a range this week of roughly $1.0780 to $1.0850. A meaningful low does not seem to be in place. Sterling is also trading inside yesterday’s ranges. It has met offers in front of $1.2930, and the intraday technicals warn of downside risk in the North American session. Initial support may be near $1.2880.

America:

It is not simply that Asia and Europe have been hit by adverse developments, but the US data has generally surprised on the upside. The contrast (divergence) helps explain the dollar’s strength, and the Dollar Index is approached 100, which it has not traded above since April 2017. On tap today is the PMI and existing home sales. Two Fed governors (Clarida and Brainard) and two regional presidents (Kaplan and Mester) speak. Canada reports December retail sales, and they are likely too old to have much impact. That said, a small gain is expected at the headline level, dragged down a bit by flagging auto sales.

The US dollar briefly dipped below CAD1.3215 yesterday to make a new low for the month before reversing higher to reach almost CAD1.3270. It is consolidating in a narrow range down to roughly CAD1.3245. On the week, the Canadian dollar has outperformed the other majors, but the Swiss franc and is down less than 0.1% against the greenback. US dollar gains above the CAD1.3280 area would improve its technical tone. The Mexican peso is extended yesterday’s nearly 1.5% decline. The US dollar has poked above MXN19.00 for after traded near MXN18.55 yesterday. It has traded above MXN19.00 a few times this year but has not closed above it since the first half of last December. We do not think that the underlying dynamics have changed and that the setback in the peso will offer new opportunities for the carry plays. However, given the increased volatility, participants will likely wait for next week.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Currency Movement,EMU,Featured,Japan,Korea,Mexico,newsletter