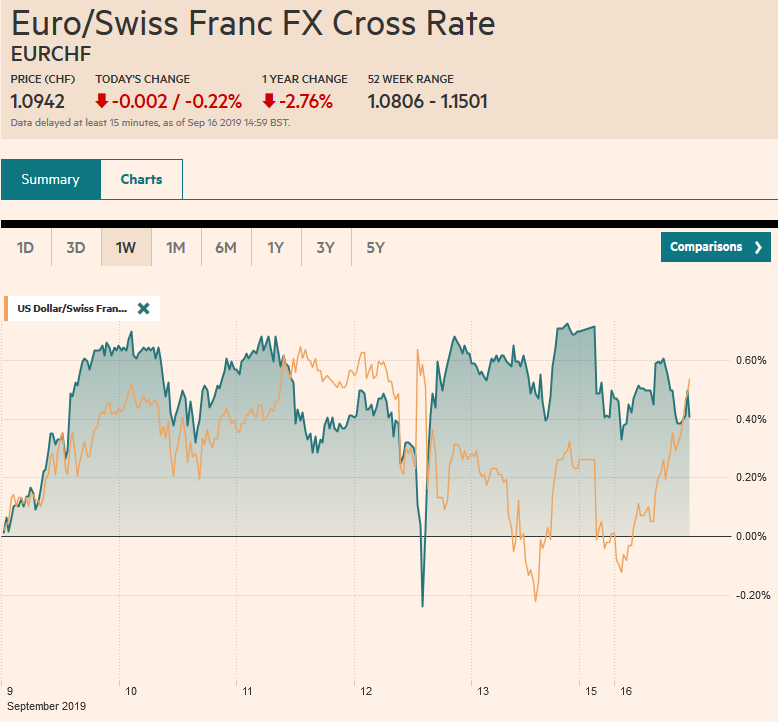

Swiss Franc The Euro has fallen by 0.22% to 1.0942 EUR/CHF and USD/CHF, September 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Oil prices surged in the initial reaction to the unprecedented drone attack on Saudi Arabia facilities. Saudi Arabia may be able to restore around half of the lost production in a few days. Saudi Arabia and other countries, including the US, prepared to tap strategic reserves, oil prices have seen the initial gains halved. Brent is trading near after finishing last week near . WTI is trading near , having been almost at from a little below before the weekend. Global equities are mixed. Hong Kong and Indian shares led the losses, while South Korea and Taiwan

Topics:

Marc Chandler considers the following as important: 4) FX Trends, 4.) Marc to Market, Brazil, Brexit, CAD, China Industrial Production, China Retail Sales, EUR/CHF, Featured, FX Daily, newsletter, Oil, USD, USD/CHF

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Swiss FrancThe Euro has fallen by 0.22% to 1.0942 |

EUR/CHF and USD/CHF, September 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Oil prices surged in the initial reaction to the unprecedented drone attack on Saudi Arabia facilities. Saudi Arabia may be able to restore around half of the lost production in a few days. Saudi Arabia and other countries, including the US, prepared to tap strategic reserves, oil prices have seen the initial gains halved. Brent is trading near $65 after finishing last week near $60. WTI is trading near $59, having been almost at $64 from a little below $55 before the weekend. Global equities are mixed. Hong Kong and Indian shares led the losses, while South Korea and Taiwan advanced. China was mixed, and Japanese markets were closed for a national holiday. European’s Dow Jones Stoxx 600’s four-day advance is at risk. Energy is the only sector that is gaining today, leaving the index off about 0.5% midday. US shares are trading with a downside bias. Asian yields adjusted higher, reflecting the pre-weekend US increase, while European benchmark 10-year yields slipped as mostly 2-4 bp lower. The main exceptions are UK Gilts, where the yield is five basis points lower, and Italian BTPs, where the yields have edged higher. The 10-year US yield pulled back from the 1.90% seen before the weekend. The US dollar is mixed. The yen was bought alongside the (sometimes) oil-sensitive Canadian dollar and Norwegian krone. All three have seen early gains trimmed. Sterling, which rallied strongly last week, is trading heavier ahead of Prime Minister Johnson’s meeting with outgoing EC President Juncker. The liquid, accessible emerging market currencies, including the South African rand, Turkish lira, Hungarian forint, and Mexican peso are all trading heavier. Gold is near $1500, the midpoint of the wide range seen already today. |

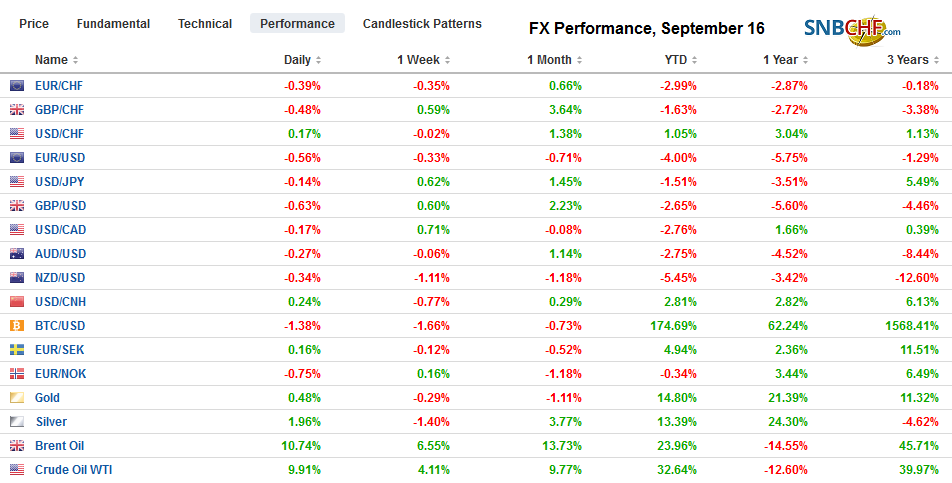

FX Performance, September 16 - Click to enlarge |

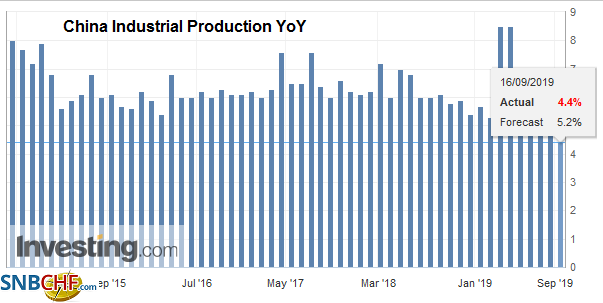

Asia PacificPoor Chinese data fans expectations that officials will provide more economic support. August data show the economy has weakened further. Investment in fixed assets slowed to 5.5% year-over-year, down from 5.7%. Economists hoped for an unchanged report. Industrial production eased to a 4.4% year-over-year pace, down from 4.8% in July. The median forecast in the Bloomberg survey was for a 5.2% increase. |

China Industrial Production YoY, August 2019(see more posts on China Industrial Production, ) Source: investing.com - Click to enlarge |

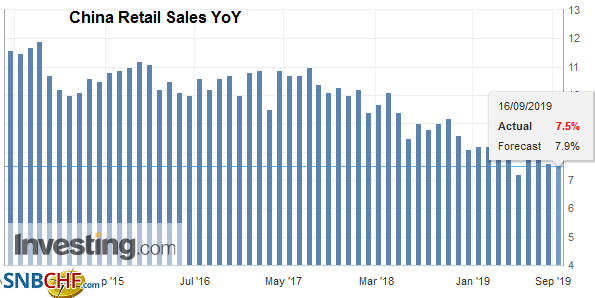

| The median estimates also expected retail sales to rise by 7.9% from 7.6%. Instead, it slowed to 7.5%. |

China Retail Sales YoY, August 2019(see more posts on China Retail Sales, ) Source: investing.com - Click to enlarge |

Reports indicate the US and Japan may sign a joint statement that will exempt Japan from any tariff or quotas the US levies on imported autos. Trump and Abe are still thought to be on track to sign the outline of a trade agreement next week on the sidelines of the UN General Assembly. Japan is expected to grant the US similar terms for its agriculture that Japan had extended to others via the Trans-Pacific Partnership and the free-trade agreement with the EU.

The dollar initially gapped lower against the yen in early Asian trade but has subsequently filled the gap. The low was just ahead of JPY107.45, where a $460 mln option is set to expire today. There is another option for roughly the same amount at JPY107.60 and an approximately $700 mln option at JPY108.15. The Australian dollar began off under pressure and slipped fractionally below the pre-weekend low before recovering in the European morning. The market does not appear to have given up on the $0.6900, which stymied it last week. The PBOC set the reference rate for the dollar at CNY7.0657. The previous fix was CNY7.0846. The yuan is one of the few emerging market currencies that gained against the dollar so far today. The Korean won increased by 0.6% to rival the Russian rouble as the strongest of the emerging market currencies today. Recall that South Korean markets were closed the last two sessions and there is a little catch-up today.

Europe

The pre-weekend hopes that a breakthrough on Brexit may be at hand faded over the weekend and sterling has pulled back from the $1.25. It is the weakest of the majors today, off about 0.6%. Johnson meets Juncker, but the issue remains the same. Does Johnson have a feasible and workable alternative to the backstop? There has been some suggestion that the UK leaves as scheduled on October 31, but there is a standstill agreement until 2022, which would allow more time to square the proverbial circle.

In Spain, King Felipe is meeting today with the main political parties and will decide tomorrow if any can form a new government with the existing Parliament. Sanchez has tried in vain. A new election, the fourth in around four years, looks nearly inevitable. It would likely be held in November and will delay the 2020 budget. Separately, Portuguese bonds are trading firmer, in line with Spain’s after S&P upgraded the sovereign outlook to positive from stable before the weekend.

Italy’s new Finance Minister, Gualtieri has rejected as unrealistic the sale of state assets worth 1% of GDP this year. The initial projections for 2020 budget envision a deficit in line with this year’s. France will project a slightly larger deficit in 2020 (2.1% vs. 2.0%) and shaved its growth forecast to 1.3% from 1.4%.

The euro briefly traded above $1.11 at the end of last week, but today has been held below it. It slipped below $1.1060 in the European morning. Chart-support may extend toward $1.1030-$1.1040 today. There is a one billion euro option at $1.1025 that expires today. The $1.25 area for sterling offers important technical resistance and houses a GBP1.2 bln option that will be cut today. Initial support now is seen near $1.24. Buying interest was seen ahead of $1.2425 in Europe today, through the $1.2440 option strike for GBP615 mln that will be cut today a well. Meanwhile, the euro is encountering resistance near GBP0.8900. Note that the 200-day moving average, which the euro has not traded below since May, has been approached (~GBP0.8840).

America

President Trump says the US is “locked and loaded depending on verification” to strike Iran for what it says was an Iranian attack on Saudi Arabia. Although many observers recognize the vulnerability of Saudi oil facilities, many are not taking the insight to the logical conclusion. Small unmanned drones are a challenge to the main warfare doctrines. It is not just Saudi facilities that are vulnerable, aircraft carriers, for example, also may be vulnerable to airborne and underwater drones.

Around 50k GM workers have struck. It is the first industrial action in the US auto sector in a dozen years. Some analysts estimate that it could cost the company as much as $50 mln a day. The union has recently increased its strike fund, and the company has around 80 days of inventory for its best selling high profit-market SUVs. Both sides seem prepared for a longer strike than the previous one that lasted a couple of days.

The IMF is considering delaying a $5.4 bln aid payment to Argentina until after next month’s election. The capital controls and intervention appear to have steadied the Argentine peso last week. The dollar rose against the Brazilian real for seven consecutive weeks through the end of August and then pushed back 2% in the first week of September before rising again (0.6%) last week. Shortly after the FOMC meeting on September 18, the central bank of Brazil is expected to announce a 50 bp cut in the Selic rate (to 5.5%). It would be the second 50 bp cut here in H2 and a new record low.

The highlight of the week is the FOMC meeting that concludes mid-week. The economic calendar is light today and features the September Empire State manufacturing survey. A small decline is expected. Canada reports its July international transactions (like the US TIC report that will be released tomorrow) and August existing home sales. Mexico has little on the diary ahead of next week’s (July) retail sales report.

The US dollar initially returned to the pre-weekend low against the Canadian dollar (~CAD1.3210) before recovering. It poked through CAD1.3260 in the European morning where fresh offers were uncovered. The intraday technical readings warn that the upside may be limited in North America today. Before the weekend, the dollar had spiked through MXN19.35 to its lowest level in a little more than a month. That looks like a near-term extreme, and the dollar can return toward last week’s high near MXN19.60. The Dollar Index is trading inside its pre-weekend range. Resistance is seen in the 98.40-98.50 area. Initial support is pegged near 98.00.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$CAD,Brazil,Brexit,China Industrial Production,China Retail Sales,EUR/CHF,Featured,FX Daily,newsletter,OIL,USD/CHF