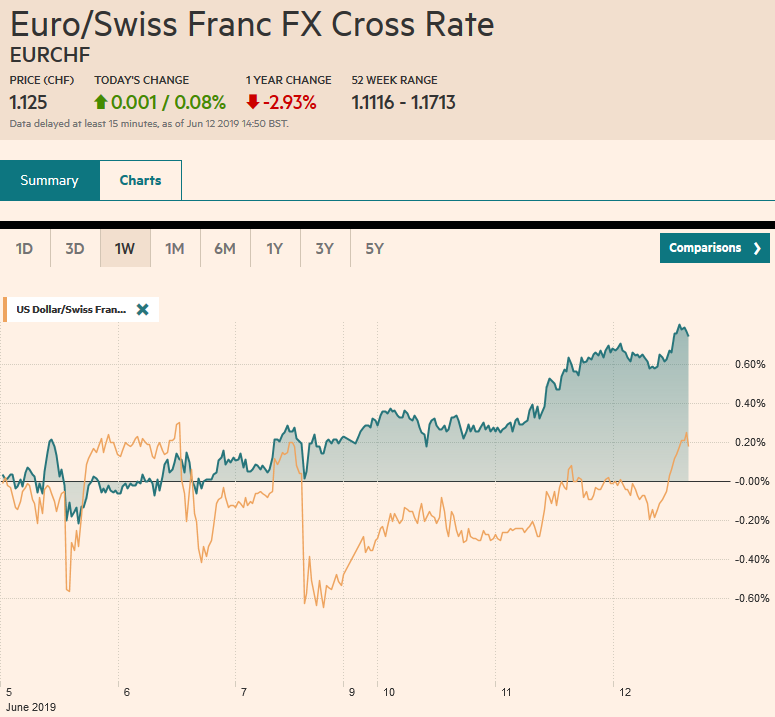

Swiss Franc The Euro has risen by 0.08% at 1.125 EUR/CHF and USD/CHF, June 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The S&P 500 snapped a five-day advance yesterday and set the heavier tone for equities today. Continued protests in Hong Kong were not shrugged off as they have been in the last couple of sessions. The Hang Seng’s nearly 1.9% decline was the largest in a month and led the region lower. European shares are falling in sympathy, and the Dow Jones Stoxx 600 is off about 0.3% in late morning turnover. US shares are trading lower in Europe, and the S&P 500 is about 0.25% lower. Benchmark 10-year yields are mostly a little lower, leaving the US

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, China, China Consumer Price Index, China Producer Price Index, Featured, Italy, Japan Producer Price Index, newsletter, trade, U.S. Core Consumer Price Index, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.08% at 1.125 |

EUR/CHF and USD/CHF, June 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

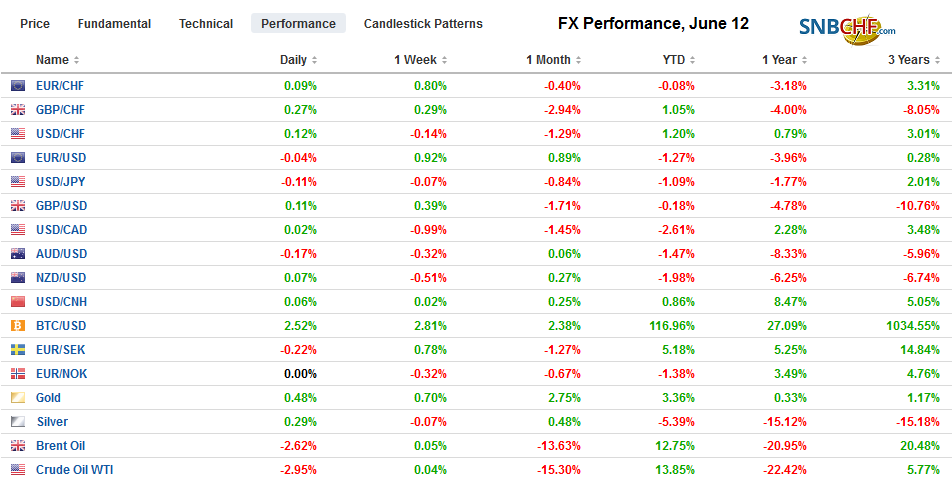

FX RatesOverview: The S&P 500 snapped a five-day advance yesterday and set the heavier tone for equities today. Continued protests in Hong Kong were not shrugged off as they have been in the last couple of sessions. The Hang Seng’s nearly 1.9% decline was the largest in a month and led the region lower. European shares are falling in sympathy, and the Dow Jones Stoxx 600 is off about 0.3% in late morning turnover. US shares are trading lower in Europe, and the S&P 500 is about 0.25% lower. Benchmark 10-year yields are mostly a little lower, leaving the US 10-year yield near 2.11%, with the 10-year Bund at minus 23 bp and Japan at minus 12 bp. The dollar is narrowly mixed. The Australian dollar is the weakest of the majors, off about 0.2% at $0.6945, while the yen is the strongest with its 0.25% gain, pushing the dollar to JPY108.30. The South African rand and Turkish lira are leading most of the emerging market currencies lower. The Mexican peso and Chinese yuan are slightly lower on the day. |

FX Performance, June 12 - Click to enlarge |

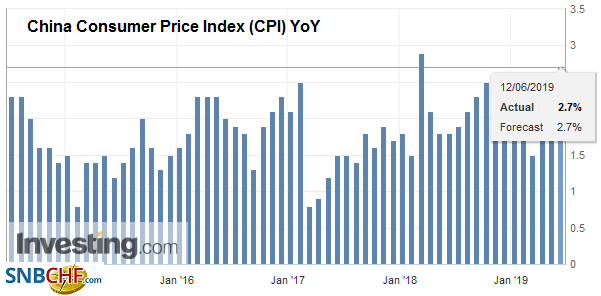

Asia PacificBloomberg estimates that today was the tenth session that the PBOC set the reference rate for the yuan stronger than the models would suggest. This provides a prima facie case that Chinese officials are not driving the yuan lower even if it could ratchet up its defense of the currency. The G20 meeting later this month is shaping up to be a key event for the yuan. Implied volatility for three-week options on the offshore yuan (CNH), which cover through the G20 meeting, jumped yesterday and edged higher today to around 5.3%. China reported inflation and lending data today. The CPI edged higher to 2.7% from 2.5%. The driver appears to be a surge in pork prices (~20%) due to the African swine flu. Food prices jumped 7.17% while non-food prices rose 1.6%. Producer prices were subdued. |

China Consumer Price Index (CPI) YoY, May 2019(see more posts on China Consumer Price Index, ) Source: investing.com - Click to enlarge |

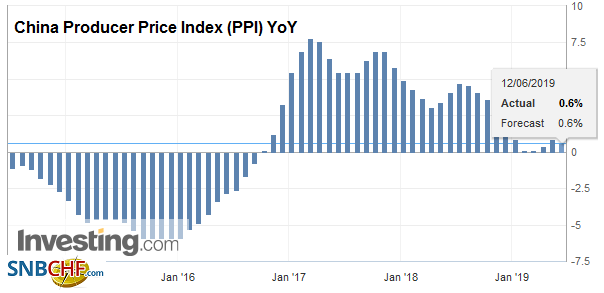

| May factory prices were 0.6% above a year ago, down from 0.9% in April. The average through April was 0.5%. Separately, China reported lending figures that were in line with expectations. Aggregate financing was estimated at CNY1.4 trillion, and banks drove this, accounting for CNY1.18 trillion. |

China Producer Price Index (PPI) YoY, May 2019(see more posts on China Producer Price Index, ) Source: investing.com - Click to enlarge |

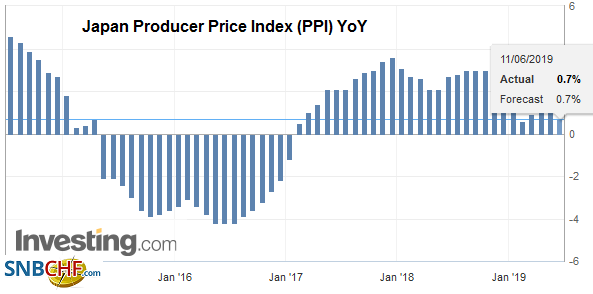

| Japan’s capital spending appears to have begun Q2 on a strong note. Core machinery orders rose 5.2%. Economists had forecast a decline. Moreover, the increase was sufficient to lift the year-over-year pace into positive territory (2.5%) for the first time here in 2019 and is the most since last August. Meanwhile, there are clearer indications that Prime Minister Abe will not seek a joint election next month and that he remains determined to increase the sales tax, after a couple of delays, to 10% from 8% in October, barring a new crisis. |

Japan Producer Price Index (PPI) YoY, May 2019(see more posts on Japan Producer Price Index, ) Source: investing.com - Click to enlarge |

The dollar rose to a seven-day high yesterday near JPY108.80 but is back near JPY108.25 in late-morning turnover in Europe. While the JPY108.00 area, which holds a billion-dollar option that expires today, may hold for the time being, we look for a test on last week’s lows near JPY107.80 in the near-term and JPY107, a technical objective (of a possible double top). The Australian dollar slipped to a marginal new seven-day low today just below $0.6945. This area corresponds to a (50%) retracement of the bounce since the low was recorded on May 17. A break of it targets $0.6925-$0.6930. The A$1.2 bln option struck at $0.7000 looks to expire worthless today. The dollar rose a little against the yuan. It closed the mainland session near CNY6.92 after finishing last week just below CNY6.91. The PBOC may not be defending any particular level, but its attempt to ward off one-way moves means that the CNY7.0 level remains important because it is perceived to be a potential inflection point.

Europe

Just as controversial as Japan’s sales tax increase is Italy’s. Italy has committed to raising the VAT to close the fiscal gap, but it is not clear that it has the political will to do so. Indeed, that seems to be the EC’s position. The VAT increase would be projected to raise about 0.7% of GDP. The reluctance of the government to support the tax increase could precipitate a political crisis after the summer. We have argued, and feel more confident post-EU Parliament vote that the Di Maio and the Five Star Movement is the chief obstacle to Salvini becoming Prime Minister. A political crisis over refusing to raise the VAT could bolster his support.

Many economists frame the issue in terms of the output gap, or how much Italy could be producing if it were operating at capacity. Brussels says it is very small. Italy’s Treasury and many economists say it’s 1.5%-2.0%. Italy’s official unemployment rate is 10.2%, and for young adults, it is twice as high, which why many economists see plenty of spare capacity. However, there are barriers to entry and skills mismatch for long periods of unemployment. The same is true of the capital equipment. It is as if many economists and accountants will count as a factory a building even if the machines no longer work and operate on older technology. However, the real problem is that those who see a large output gap would imply scope for stimulative policies. Italy has little influence on monetary policy, so fiscal policy would be the primary tool. More spending and/or a larger deficit that would attempt to stimulate growth risks being offset in full, if not more, by higher interest rates.

The euro made a marginal new high for the week and moved within five-hundredths of a cent of the post-US jobs disappointment high. The high from the end of last week as just shy of $1.1350, where a 1.2 bln euro is set to expire today. The $1.1325 strike that holds a little more than 720 mln euros may also be in play. There are also nearly 820 mln euro in a $1.1300 option that too will be cut today. It is difficult to see a near-term catalyst to propel the euro higher, which suggests, that gains might need to be more a weak dollar story. Sterling is trading firmly, but going nowhere quickly. It may be hemmed in by two sets of options that are set to expire today ($1.2700-$1.2720 and $1.2760). It is not so much the size (~GBP690 mln and ~GBP205 mln respectively) but reflective of the sideways movement over the past five or six sessions.

America

Seemingly without much provocation from China, Trump has escalated his rhetoric. The US has repeatedly made reference to the two presidents meeting at the G20 later this month. Publically, China has neither confirmed nor denied a meeting. Chinese officials, recognizing that a grand agreement is unlikely, may have been probing to see the interest in a simple trade agreement.

Trump has now threatened China that he would follow through with the tariff on the remaining imports, and it could be more than the 25% that had been threatened. Moreover, Trump insists that China must return to the positions he says it had before retreating or he has no interest in a deal. If Xi were going to meet with Trump, the new threat would make it appear he was capitulating to US demands. Alternatively, Trump may have learned, as we suggested, that Xi was inclined not to meet. There is little to gain from the meeting and much to lose. Imagine they meet, and Xi does not alter his position, Trump would levy the tariffs, or Xi compromises and later, as Trump did with Mexico, and threaten tariffs in another dispute. Tariffs seem a bit like duration the bond market. Duration refers to how long for the coupon to return the principle to the lender. There is not much a difference in terms of duration between a 10-year and 30-year bond. Similarly, for most goods, there might not be a significant difference between a 25% tariff and a 50% tariff.

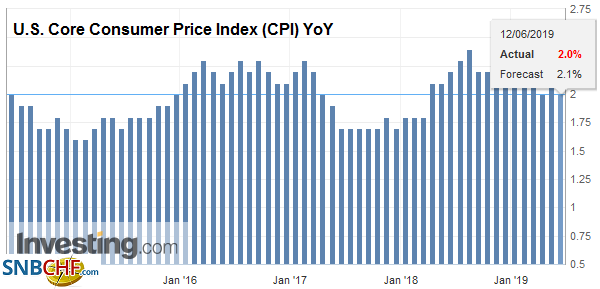

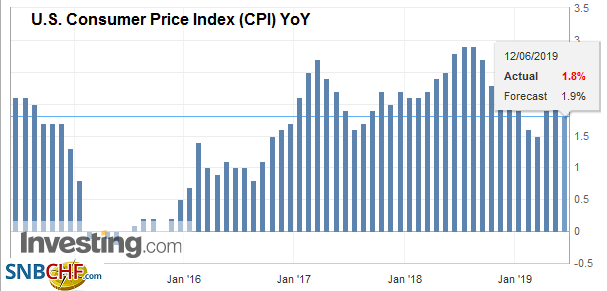

| The US reports May consumer prices today. A small increase in the headline rate will not be enough to prevent the year-over-year rate from slipping to 1.9% from 2.0%. However, the midwest floods and some of the retaliatory tariffs may begin showing up in food prices. Excluding food and energy, April’s 2.1% year-over-year pace may be sustained. |

U.S. Core Consumer Price Index (CPI) YoY, May 2019(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

| Many journalists and analysts claim that the Fed targets the core deflator for personal consumption expenditures. Frankly, it just ain’t so. This is a factual question, not a matter of opinion. It sees the 2% annual pace of the headline PCE deflator as consistent with its mandate for price stability (here is the Fed document that is explicit). |

U.S. Consumer Price Index (CPI) YoY, May 2019(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

The US dollar has traded firmly against the Canadian dollar since hitting a three-month low near CAD1.3225 to start the week. It poked through CAD1.3300 yesterday but failed to close above it. The market has not given up. To really get the ball rolling it needs to push the greenback above CAD1.3335 where a roughly $535 mln option is placed that expires later today. The downside is also protected with a $1.1 bln option at CAD1.3275. The US dollar is also trading firmly against the Mexican peso after dipping below MXN19.10 yesterday. Initial resistance is seen near MXN19.25-MXN19.30. Note that oil prices are breaking down today, with WTI off about 1.5% and Brent down around 2.5%. The large build in US inventories (API estimate) and concerns about demand weigh on sentiment after yesterday’s quiet consolidative session. The government’s estimate (EIA) is expected to report a one million barrel draw. Yesterday the EIA shaved its production forecasts for this year and next. Output next year is expected to rise to 13.26 mln barrels a day from an estimated 12.32 mln barrels a day this year.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$CNY,China,China Consumer Price Index,China Producer Price Index,Featured,Italy,Japan Producer Price Index,newsletter,Trade,U.S. Core Consumer Price Index