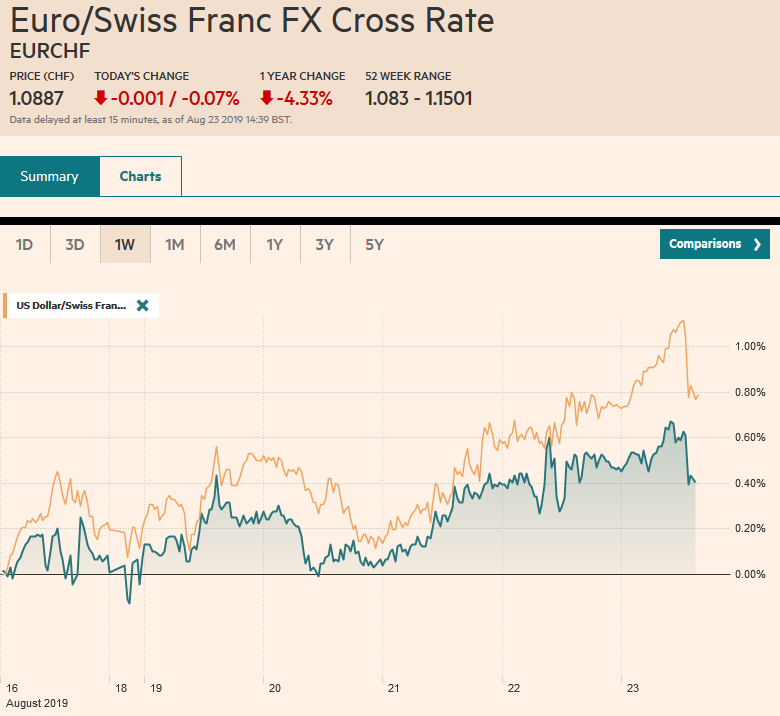

Swiss Franc The Euro has fallen by 0.07% to 1.0887 EUR/CHF and USD/CHF, August 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Powell speech at Jackson Hole stands before the weekend. Equities in Asia and Europe are finishing the week on a firm tone. Most markets in the Asia Pacific region closed higher today, and the MSCI Asia Pacific Index snapped a four-week slide. European bourses are edging higher, and the Dow Jones Stoxx 600 is poised to end its three-week air pocket. US shares are higher in European trading and barring a reversal in the North American session, the S&P 500 will finish stronger for the first time in four weeks. Benchmark 10-year yields are higher, and some suspect the poor reception

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, Currency Movements, Featured, Federal Reserve, Italy, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.07% to 1.0887 |

EUR/CHF and USD/CHF, August 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Powell speech at Jackson Hole stands before the weekend. Equities in Asia and Europe are finishing the week on a firm tone. Most markets in the Asia Pacific region closed higher today, and the MSCI Asia Pacific Index snapped a four-week slide. European bourses are edging higher, and the Dow Jones Stoxx 600 is poised to end its three-week air pocket. US shares are higher in European trading and barring a reversal in the North American session, the S&P 500 will finish stronger for the first time in four weeks. Benchmark 10-year yields are higher, and some suspect the poor reception of Germany’s 30-year zero-coupon bond earlier this week marked at least a temporary extreme. The US 10-year yield has risen nine basis points this week, which if sustained, would be the largest weekly gain since March. The US dollar is mostly firmer against the major currencies, though the Scandis and Antipodeans are resisting the pull. Sterling, which shot up yesterday on what we suspect is misplaced optimism regarding Brexit and reached its best level since late July (~$1.2275), is paring those gains today. It is finding support near the top of its previous range (~$1.22). Among emerging markets, Egypt and Sri Lanka joined the rate-cutting party with 125 bp cut (to 14.25%) and a 50 bp cut (to 8%) respectively. |

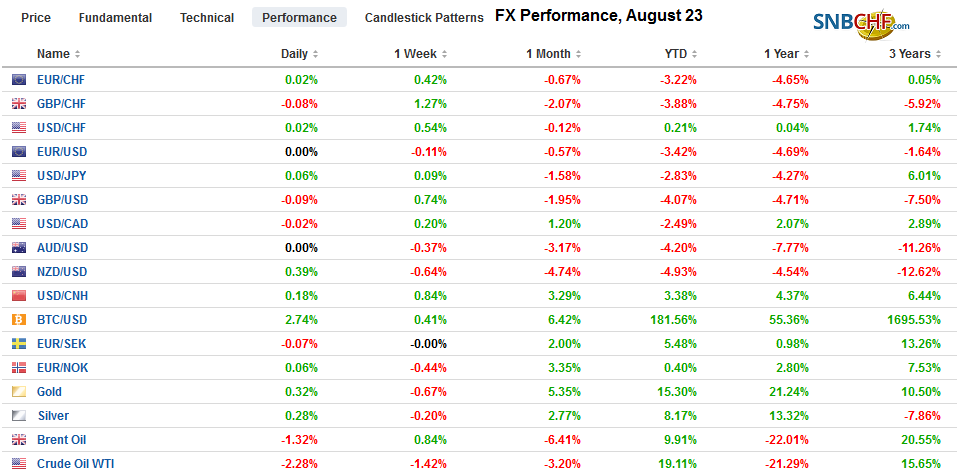

FX Performance, August 23 - Click to enlarge |

Asia Pacific

The PBOC continues to set the dollar reference rate lower than the models suggest. It has slowed by not reversed the yuan’s weakness. The onshore yuan (CNY) fell for six consecutive sessions coming into today. The dollar made a new high just shy of CNY7.10 before reversing lower. Many, including ourselves, suggest CNY7.10 was around the magnitude of the adjustment anticipated. There is a medium-term lending operation that matures Saturday, and this would give the PBOC an opportunity to cut rates. However, officials do not seem to be in much of a hurry. Elsewhere, a cut in subsidies for the alternative energy vehicles is seen cutting into lithium demand and another disruption to the auto sector. The knock-on effect of new emission standards is one of the factors that have weighed on the German auto industry.

Japan reported July CPI figures. Price pressures are stable, but well below the 2% target the BOJ has dramatically expanded its balance sheet in trying to achieve. The headline rate eased to 0.5% from 0.7%, but the core rate, for which only fresh food prices are excluded, and is the measure the BOJ targets, was stable at 0.6%. Excluding both fresh food and energy, Japan’s CPI was steady at 0.6%. Under the yield curve control policy, the 10-year yield should not fall beyond minus 20 bp, but the yield has been less than that for the second consecutive week.

The dollar has been trapped in a about a 15 tick range on either side of JPY106.55. It has not traded above JPY106.70 this week or below about JPY106.15. There is a $765 mln option at JPY106.25 (yesterday’s low) that will be cut today. If the greenback finishes today above JPY106.40 (roughly last week’s close), it will be the first back-to-back weekly gain since April. Thin markets seemed to have allowed the Australian dollar to briefly slip to a marginal new low for the week (~$0.6745) before recovering to little changed but higher on the day levels. Still, the Aussie closed near $0.6770 last week, and unless this area is re-taken, it will record its sixth consecutive weekly decline. The New Zealand dollar fell to new three-year lows yesterday (~$0.6360) but is coming back a little firmer following comments by the Reserve Bank of New Zealand Governor Orr who suggested that after the surprise 50 bp rate cut, the central bank can be patient. The market continues to lean toward another cut not at the September 25 meeting but the one after than November 13, which is also the last one until February 2020.

Europe

Market participants heard what they wanted to yesterday regarding Brexit. UK Prime Minister Johnson visited Germany and France in recent days. He came bearing no new ideas besides rejecting the backstop for the Irish border. Merkel and Macron were good hosts. In essence, they said fine, you don’t like the backstop. Give us a realistic alternative. Meanwhile, some of the Tory’s who support the idea that no deal is better than the Withdrawal Agreement that had been negotiated for 18 months, warned that Johnson has to do more than simply jettison or modify the backstop to secure their support. At the end of the day, the risks of a no-deal Brexit remain elevated, and apparently the base case for many. Separately Trump and Johnson will reportedly breakfast together at the G7 meeting this weekend.

Macron expressed concern about the fires in the Amazon and got a sharp response by Brazil’s President Bolsonaro. However, the fires putting the EU-Mercosur trade agreement in jeopardy, with Ireland threatening to veto the agreement unless the Amazon is protected better.

Italy’s President Mattarella has given the political parties until Tuesday to put together a new government from the existing parliament. It still looks like an uphill struggle. The PD (center-left) demands to the Five Star Movement (MS5) may make it difficult to form a coalition. Meanwhile, perhaps chastened by the latest polls that show the League’s support has slipped to 31% from 40%, which means a majority may be elusive after all, Salvini suggested he could be persuaded to renew the pact with the MS5 if it supported more of its policy proposals.

The euro slipped to about $1.1055 in Asia, which is the lowest since August 1 push to almost $1.1025 and its lowest level since May 2017. A 760 mln euro option at $1.1030 will expire just as Powell prepares to speak at Jackson Hole. The euro rose in one session last week and one session this week. It rose one week in July and one week in August. It was three cents higher at the end of June. Resistance is seen in the $1.1100-$1.1115 area. Sterling spiked to almost $1.2275 yesterday and what we suspect is a misunderstanding of the signals from Merkel and Macron. It found support just below $1.22, previous resistance, in the European morning. It sterling closes above $1.2150, it would be the second consecutive weekly advance for the first time in four months. After falling for 14 straight weeks against the euro, sterling is set to finish higher also for the second consecutive week.

America

Powell’s prepared remarks are expected to be released just before he speaks at the Jackson Hole confab at 10:00 am ET. Although initially praised for his communication style, sentiment has turned and a recent survey showed many primary dealers frustrated by the Chair’s communication. Part of the problem though is substance. For years, the argument was that the Fed was too easy, and now, the knock is it is too tight. Powell framed last month’s rate cut as a midcourse correction and the minutes from the meeting seemed to show that this was a consensus understanding. The market wants the Fed to acknowledge that it is a genuine easing cycle, and it needs to get ahead of the coming recession. Although yesterday’s disappointing flash PMI, with manufacturing slipping below the 50 boom/bust level seemed to support the recession call, the index of Leading Economic Indicators jumped 0.5, well above expectations and the June series was revised to show only a 0.1 decline rather than a 0.3 fall. Initial jobless claims also fell more than expected, and it covered the week in which the non-farm payroll survey is conducted.

The January 2020 fed funds futures contract implies a 1.575% average effective funds rate at the end of the year and is now at 2.12%. The market still has two more 25 bp rate cuts discounted this year. Its the third one that remains in dispute. The implied yield of the January contract has risen by about 20 bp since the trough on August 7 (~1.37%). We remind that the midcourse correction language harkens back to Greenspan in the 1990s, and the two uses, in hindsight, signaled three rates cuts. The first was delivered last month.

Canada is expected to report the second consecutive decline in retail sales. The June headline is likely dragged down by weak auto sales. The 0.1% decline in May was a function of weaker food and alcohol sales. Canada will report Q2 GDP next week, and the economy strengthened after a poor Q1 that saw it nearly stagnate. The economy is expected to have grown at an annualized rate of almost 3% after a 0.4% pace in Q1. Mexico may not be as fortunate. It reports revisions to its Q2 GDP estimate today. The preliminary estimate was for a 0.1% quarterly expansion, which resulted from rounding up a 0.05% pace. A slight downward revision could push it below zero and would follow a -0.17% contraction in Q1.

Barring a sharp sell-off today, the US dollar will close higher against the Canadian dollar for the sixth consecutive week. It began the streak near CAD1.3030 and saw almost CAD1.3350 this week. Initial resistance is seen extending to CAD1.3360, but the next technical target is near CAD1.3430.Similarly, the dollar has appreciated against the Mexican peso for six consecutive weeks. It began the campaign below MXN19.00 and is now testing almost MXN19.90 this week. Initial support now is seen around MXN19.75.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,Currency Movements,Featured,Federal Reserve,Italy,newsletter