The chief uncertainty has shifted from monetary policy and macroeconomics to the increase of volatility in the stock markets and the prospects of a trade war. Some of the major benchmarks, including the S&P 500, the MSCI Asia Pacific Index, the MSCI Emerging Markets Index, and Shanghai Composite held above the February lows in the retreat during the second half of March. Other bourses did not. These include the DAX, the FTSE 100 and 250, the CAC40, and the Nikkei. However, even for those markets that made new lows, they were often marginal and ahead of the quarter-end, stabilized. Technical indicators suggest that a low may have been recorded. While some investors are positioned for Q2, it appears that cash levels

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, EUR, Featured, JPY, newsletter, TLT, trade, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The chief uncertainty has shifted from monetary policy and macroeconomics to the increase of volatility in the stock markets and the prospects of a trade war.

Some of the major benchmarks, including the S&P 500, the MSCI Asia Pacific Index, the MSCI Emerging Markets Index, and Shanghai Composite held above the February lows in the retreat during the second half of March. Other bourses did not. These include the DAX, the FTSE 100 and 250, the CAC40, and the Nikkei.

However, even for those markets that made new lows, they were often marginal and ahead of the quarter-end, stabilized. Technical indicators suggest that a low may have been recorded. While some investors are positioned for Q2, it appears that cash levels have been raised and many investors will wait to see what happens, perhaps until after the US jobs data at the end of the week.

FactSet reports that Q1 earnings expectations for the S&P 500 have risen by 5.4% on a bottom-up basis over the course of the quarter. This is highly unusual. Forecast generally fall. Over the past ten years, they have been reduced on average by 5.5%. It is the largest increase since the FactSet began tracking the data in Q2 02. Earnings expectations for the entire year have also been lifted. The 7% increase is the most since at least 1996.

One can be a realist and reject the militarization of the competition between countries. For years, we were told there was a currency war. Now it is a trade war. Tensions between countries are best thought of as an escalation ladder. War, as the father of military realism, Clausewitz, taught, is the continuation of politics by other means. There is nearly a constant low level of trade tensions even between the best of friends and allies (e.g., US-Canada, Germany-France).

Given the amount of trade that the US has impacted with its series of measures (solar panels, washing machines, steel, aluminum, and a range of Chinese produced goods) and the extent of the retaliatory measures, these are still the low rungs of the escalation ladder. At first there were going to be no exemptions, and now there are several. The WTO will be the most important challenge to US actions, and this may help strengthen the multilateral process, which so many seem to be prematurely eulogizing.

The US is pressing to get more of the distributional benefits from trade. Discussions with foreign officials confirm our suspicions that many are prepared to make small concessions to avoid moving higher on the escalation ladder. In Europe, Germany appears to be more willing to make some concession; France less so. The temporary exemptions from the tariffs currently have a May 1 deadline. That means there will be much jockeying for position, posturing and a little negotiating.

Oscar Wilde said that there were only two tragedies in life, not getting what one wants and getting it. It seems applicable to trade. The fiscal stimulus in the form of tax cuts and increased spending, while the economy is growing above trend, is likely to boost US imports, fueling a widening of the trade deficit.

Quotas will encourage foreign producers to change their product mix to higher profitable units, which opens a new front in the competition with domestic producers. Some foreign producers are likely to copy the strategy of Japanese companies when they were the target of US trade efforts and open production with the protectionist (real or threatened) walls.

Trade tensions are elevated, to be sure. However, they are still well below levels that can be fairly portrayed as a war. We find strong parallels between Trump’s trade personnel and policies and Reagan’s.

During the Reagan Administration, the economic competition between the US and military allies intensified. The US used “voluntary export restrictions” and “orderly market agreements” to try to arrest the deterioration of the US trade balance, which had begun driving the current account into deficit.

And it was not just Japan that saw US ire. Some observers link the 1987 equity market crash to James Baker’s threat to allow the dollar to fall if Germany did not do more to stimulate its economy.

It was not called a currency war at the time, but the coordination of G7 policy (from the Plaza Agreement to the Louvre Accord) masked the fact that the currency market was the terrain in which advanced capitalist countries fought for advantage. And to be sure, the advantage was not always a weak currency, as Europe and Japan as much as the US wanted to stop the dollar from rallying by the end of Q3 1985.

To summarize, we think there is a reasonable chance that the many of the major equity markets forged a low and that Q2 may begin on firmer footing. Investors should be prepared for a sustained period of elevated trade tensions, but not something that can be fairly called a trade war. Of course, the situation is evolving, and we will continue to monitor it.

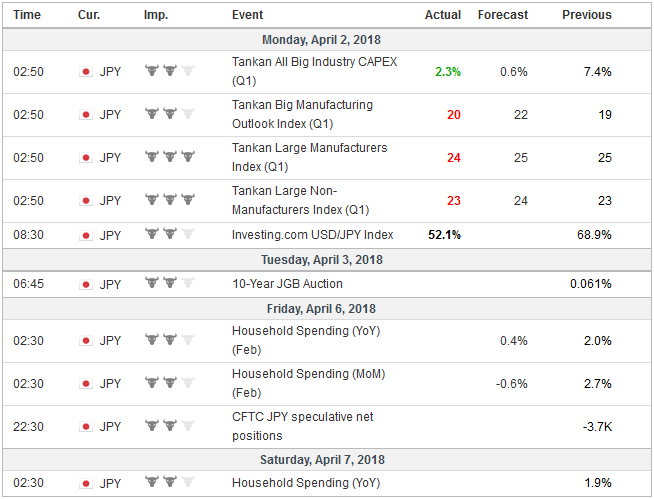

JapanThere are four events in the days ahead that are stakes in the macro picture. The week begins with Japan’s Tankan Survey. Sentiment is not expected to have changed much from the December readings. However, a sharp decline in capex plans (after 7.4% in the previous survey) would play on fears that the long Japanese expansion is passing into late stages. And note that plans of large businesses tend to exceed actual spending. Industrial output and construction remain strong, and this may speak to the export and government sectors, but services and consumption have disappointed. In December, the survey found a median forecast that the dollar-yen rate would average JPY110.18 in the fiscal year that just ended. Around the time of the December survey, the dollar had been averaging around JPY111.50 for first nine months of the fiscal year. It is ended up averaging JPY110.84. It has averaged about JPY108.35 in the last three months. We will watch the price action during Tokyo hours to see if the apparent dollar selling hedging has been completed. |

Economic Events: Japan, Week April 02 - Click to enlarge |

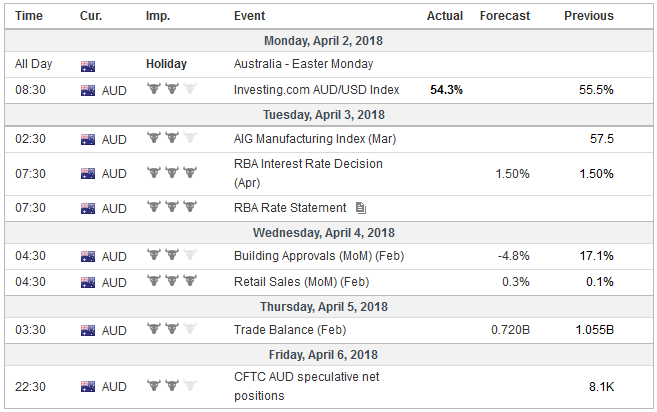

AustraliaThe Reserve Bank of Australia meets next week, and there is little doubt that will keep the cash rate at 1.5%. In fact, it is expected to remain on hold for the coming months, with about a one-in-three chance of a hike in Q4. Six months ago the market was pricing in two hikes for this year. We suspect that the RBA may be on hold longer. The economy is showing late-cycle symptoms. Labor market growth, housing, and credit extension are slowing. The Australian dollar has declined 5.5% against the US dollar and 5.9% on a trade-weighted basis over the past two months. Australia’s entire curve is now below the US. The two-year yields were 25 bp less than the US. It is the first time it is at a discount since 2000. It is the first time in 20 years that the US pays more to borrow 10-year money than Australia. News over the weekend that China’s official March PMI improved will be taken by the usual grand of salt with data around Lunar New Year. The improvement in manufacturing (51.5 from 50.3) was more impressive that the improvement in non-manufacturing (54.6 from 54.4), and this may be linked to some anti-pollution measures. The composite rose to 54.0 from 52.9, but the improvement should not be exaggerated. Recall that the composite averaged 54.4 in Q417. Still, although the Australian dollar finished the holiday-shortened week on soft footing, our reading of the technical condition suggests a low may be close. Industrial metal prices fell in March but may be bouncing, which could help facilitate a technical correction in the Aussie. However, the medium-term macro outlook is not particularly encouraging, and the privilege of owning Australian dollars (the interest rate discount) is likely to widen over the coming quarters. |

Economic Events: Australia, Week April 02 - Click to enlarge |

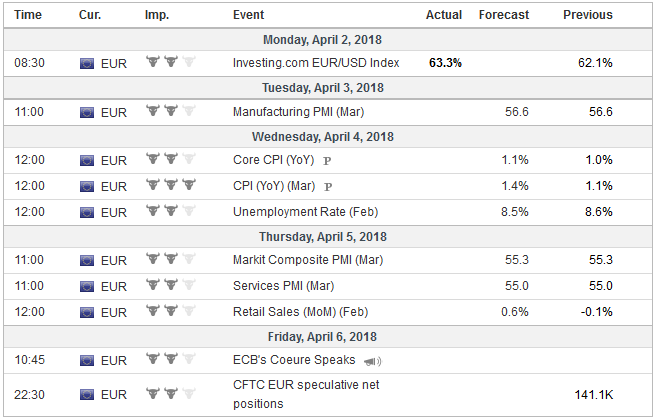

EurozoneThe third stake of the macro picture will be provided by a host of eurozone data. The most important is arguably the March CPI. At the end of last week, the largest four members reported a mixed bag, Germany and Spain were a little less than expected, while France and Italy were a bit more. Seasonal factors are also at work. The headline rate is expected to rise to 1.4% from 1.2%, while the core rate is tamer, pipping up to 1.1% from 1.0%. The start of a month would not be complete without the PMI surveys. The flash reading had confirmed the second month of moderation. It is the speed of the moderation that may have given investors pause. The composite peaked in January at 58.8, when everything looked swimmingly. The flash reading was 55.3 in March, which is lowest since January 2017. The risk is that the final reading is a bit lower if the political uncertainty in Italy, labor strife in France, or trade war talk take a toll. Speculation that the ECB’s forward guidance was going to evolve quickly this year may have helped lift the euro at the start of the year. ECB is moving slower, and expectations have adjusted. Here in Q2, the ECB meeting in late April and mid-June. The mid-June meeting, with new staff forecasts, forward guidance can be modified. A few days before the April 26 meeting, on April 23, Markit flash PMIs for April will be released. We are loath to put much weight on any one high-frequency economic report, but Draghi often cited the surveys, and this will be the first important check if the flagging momentum in Q1 is continuing. |

Economic Events: Eurozone, Week April 02 - Click to enlarge |

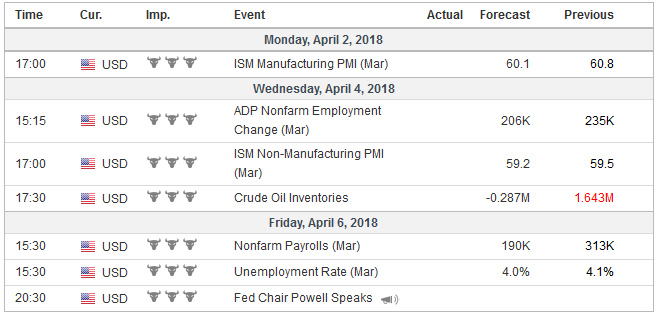

United StatesLastly, the week closes with the US employment report. It remains the single most important US economic report. It is most often reported on the first Friday of a new month, and it can be used as input for other economic forecasts, including industrial, manufacturing and construction, income and consumption. The focus has shifted from job growth per se to hourly earnings. Job growth remains robust, and the new cyclical low in the weekly jobless claims (week ending March 23) buoys sentiment. After an outsized 315k increase in February, the median forecast is for about 190k in March, which matches the 12-month average. Last year, non-farm payrolls grew 182k a month on average. The 12-month average peaked three years ago near 260k. Average hourly earnings are expected to have risen by 0.3%. On its own, it is a positive number. The longer-term monthly (12 and 24 months) average is 0.2%. The base effect limits the impact on the year-over-year rate, but a 0.3% increase would be sufficient to lift the yearly pace to 2.7%. The 12 and 24-month average is 2.6%. Little new impulses, therefore, will likely be seen in the jobs report. The labor market remains strong but with no compelling evidence of earnings acceleration. Other economic data, including factory goods orders, may fan hopes that the tax cuts will boost capital expenditure. On the other hand, auto sales appear to be returning to rates that were prevailing before the replacement surge after the devastating storms last September. US brands may pick up some market share. It seems clear that Fed officials are looking past whatever slowdown we are experiencing in Q1. In fact, the recent data suggest that loss of momentum may be less than it had appeared. The Atlanta Fed now see the economy tracking 2.4%, while the NY Fed’s model has it at 2.7%. While a June rate hike sees likely, we note that the Fed funds futures strip seems to imply about a 25% chance of a May hike. This seems more than a little stretch. |

Economic Events: United States, Week April 02 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week April 02 - Click to enlarge |

Tags: #USD,$AUD,$EUR,$JPY,$TLT,Featured,newsletter,Trade