Swiss Franc The Euro has risen by 0.12% at 1.1277 EUR/CHF and USD/CHF, December 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The 2% slide in the S&P 500 to new lows for the year yesterday hit Asian and European equities today. Bond yields are lower, and the dollar is softer against most major currencies. The dramatic equity losses and some disappointing data sparked doubts about the ability of the Fed to raise rates tomorrow at the conclusion of its last meeting of the year. India shares continue to buck the trend and advanced for the sixth sessions. The Nikkei lost 1.8% but held above the key 21000. European bourses are lower, and the Dow Jones Stoxx 600

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, Featured, GBP, JPY, newsletter, SPX, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.12% at 1.1277 |

EUR/CHF and USD/CHF, December 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The 2% slide in the S&P 500 to new lows for the year yesterday hit Asian and European equities today. Bond yields are lower, and the dollar is softer against most major currencies. The dramatic equity losses and some disappointing data sparked doubts about the ability of the Fed to raise rates tomorrow at the conclusion of its last meeting of the year. India shares continue to buck the trend and advanced for the sixth sessions. The Nikkei lost 1.8% but held above the key 21000. European bourses are lower, and the Dow Jones Stoxx 600 is off for the fourth consecutive session and is back near year’s lows set last week. Fixed income draws savings. Core benchmark 10-year yields are off two-three basis points, while peripheral yields are down a little less. The 10-year German Bund was yielding almost 60 bp in early October. Today it is near 23 bp. The low for the year was set in May near 18 bp. It finished last year a little more than 40 bp. Oil prices continue to plunge. January WTI is off more than a dollar a barrel for the third consecutive session. It broke below $50 a barrel yesterday and today, briefly traded below $48. |

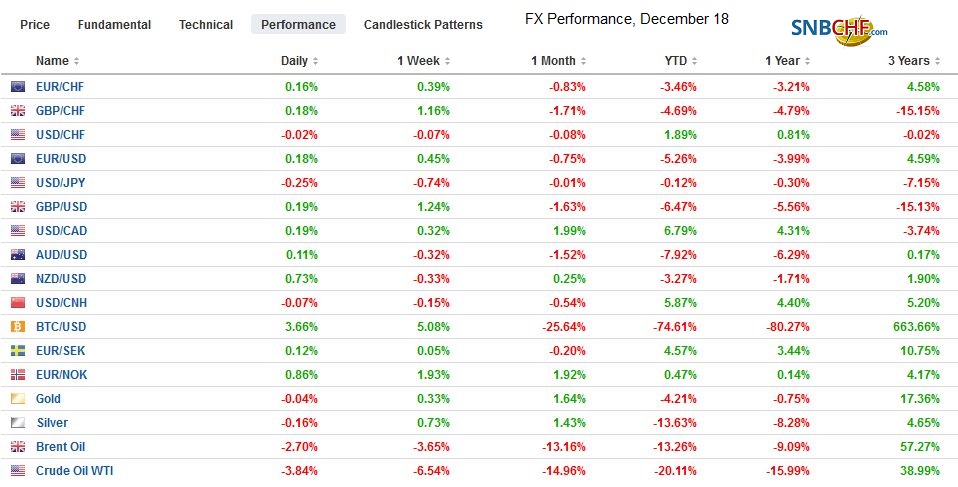

FX Performance, December 18 - Click to enlarge |

Asia Pacific

There had been a big build-up for Chinese President Xi’s speech today to celebrate the 40th anniversary of the reforms that led the modernization of China’s economy. Investors were disappointed. There were no concrete proposals of stimulus or reform. Many in the West see a contradiction between the modernizing economy and rigid political structure. Indeed, despite ongoing economic changes, many see Xi as reluctant to build on past reform momentum.

The US Treasury data suggests the two largest foreign holders of US Treasuries, China and Japan reduced their stakes by about $10 bln each to $1.14 trillion and $1.02 trillion respectively. Both have reduced their investment in Treasuries for the third consecutive month and the seventh time in the first ten months of 2018. We would downplay the significance. First, their sales are minor and have not prevented the rally in Treasury prices. Second, the TIC data is not precise, and decline is little more than a rounding error. Third, to the extent there have been real sales, it appears to be driven by economic considerations, not politics. Fourth, the US is often ambivalent about foreign holdings of Treasuries. On the one hand, given the current account and budget deficit, foreign savings is needed. On the other hand, in recent years, US officials have urged foreign officials not to intervene in the foreign exchange market, which is a significant way dollars are acquired that are reinvested in US Treasuries. Buy US goods, they would say, rather than paper, and allow the foreign exchange market to make the adjustment.

The dollar-yen exchange rate had been fairly resilient until yesterday in the face of the drop in yields and equities. The dollar broke JPY113 yesterday, and the losses were extended today to about JPY112.30, holding a little above the lows seen last week and the previous week near JPY112.20. There is some congestion near JPY112 going back to mid-October, and a break targets JPY111.35. There are two expiring options (JPY111.90 for ~$400 mln and JPY112.55 for ~$470 mln) that could be in play today. The minutes from the Reserve Bank of Australia seemed reluctant to accept the logical conclusion of high household debt and falling property prices, which would seem to point to significant economic headwinds on consumption. The Australian dollar had been flirting with $0.7400 at the start of the month and had fallen to around $0.7150 at the end of last week. It consolidated yesterday and today and is struggling to re-establish a foothold above $0.7200. On a purely directional basis, the price of Brent oil and the Indian rupee are highly correlated (~0.85 over the past 60 days). The rupee is the strongest of the emerging market currencies today, extending yesterday’s recovery.

Europe

There is no end to the Brexit drama. Labour is pushing for a vote of confidence in the government, which is different than last week’s confidence vote within the Conservative Party. No date has been set. Today, the UK cabinet will decide how to proceed with preparations. The choices are pretty stark. Stop preparing for no agreement. Maintain current pace and arrangments. Boost efforts and centralize preparations. The government resists what appears to be growing pressures for a second referendum, but according to a local press report, the legal advice the government was given, rules it out.

The German IFO makes for sober reading. The overall assessment of the business climate fell for the fourth consecutive month, and 101.0 it is at new lows for the year. Indeed, it is the lowest since December 2016. The components were equally dismal. The assessment of the current situation fell to 104.7 from 105.5. It is the lowest since June 2017. The expectations index fell to 97.3 from 98.7. This is a four-year low. The IFO like the ZEW survey seems sensitive to the performance of the DAX. The German stock market fell for the fourth consecutive month in November and has only risen in the three of the first 11 months of the year. December is shaping up to be true to trend.

Macron’s agenda is in disrepair. Although the Yellow Vests protests may have lost some momentum as the approaching holidays would have done in any event, the impact on the French government will likely be more durable. With Italy making overtures to the EC and is not only revising its projected 2019 deficit but is also making its assumptions more acceptable, the French challenge is threatening to eclipse it. Reports indicate that the government will bring its 2019 growth forecast more in line with others at 1% rather than 1.5%. This may still be a stretch. With the economy having contracted in Q3, the recession-watch (as in back-to-back declines in GDP) is on high alert. Macron is to meet with union officials today, but his intended overhaul of unemployment benefits (which for some could be five times the minimum wage) is likely to face strong resistance.

The euro is continuing to recover from the slide that took it to around $1.1270 before the weekend. It has moved toward $1.1390. Last week’s high was seen near $1.1445. There is a nearly 900 mln euro option at $1.1402 that expires today, and another roughly 720 mln euro-option at $1.1430 that will be cut today. Since November 27, the euro has closed consistently with a $1.13-handle. Sterling is also trading firmer. Initial resistance is seen near $1.2660, but the high from the second half of last week around $1.2685 is coming into view. The UK reports November CPI tomorrow, and it is expected to have slipped a little. Thursday sees November retail sales and a modest recovery is expected after declines in October.

North America

The US reports November housing starts and permits. The risk is on the downside. However, the market is going to take its cues from the stock market. US shares are trading higher in Europe, and the S&P 500 is trading about 0.4% higher. The pace of the equity market drop is scaring investors and is making some have second thoughts about the Fed raises rates tomorrow at the end of its two=-day meeting. The implied yield of the January Fed Funds futures contract is 2.365%. The current effective Fed funds rate is 2.20%. We are not convinced. Surely, the fact that officials recognized that valuations were at the upper end of historical relations ought to be a mitigating factor. Also, if officials want to diminish the moral hazard of investors thinking there is a Fed put, raising rates would drive home that point, like little else. On the downside, the 2509 area in the S&P 500 corresponds to a 38.2% retracement of the rally since March 2016, and 2517 is the same retracement since the November 2016 election. Meanwhile, a partial government shutdown at the end of the week is looking increasingly likely. The key stumbling block is funding for a border wall with Mexico. Ironically, the Department of Homeland Security is one of the parts of the government that has not already been funded for next year.

The drop in oil prices and concerns about the weakness of the US economy may be taking a toll on the Canadian dollar. It is struggling to benefit from the softer US dollar tone. The US dollar continues to straddle the CAD1.34 area. Norway, the other major oil producer among the major economies, is also seeing the krone weaken. The Dollar Index recorded the year’s high before the weekend near 97.70. It is being pushed back below 97.00 today. The next level of chart support is seen near 96.35.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,Featured,newsletter,SPX