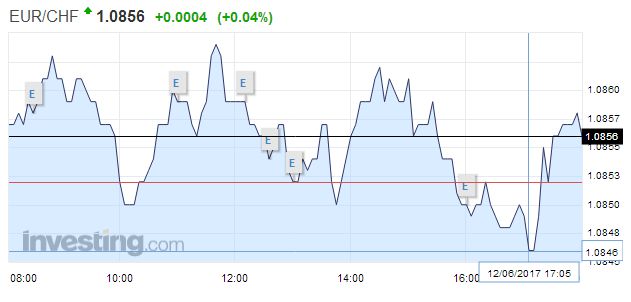

Swiss Franc The Euro has risen by 0.04% to 1.0856 CHF. EUR/CHF - Euro Swiss Franc, June 12(see more posts on EUR/CHF, ) - Click to enlarge FX Rates The US dollar is trading within its pre-weekend range against the major currencies as participants await the central bank meeting starting in the middle of the week. The Federal Reserve, Bank of England, and the Bank of Japan meet. Only the Fed is expected to hike rates, but given the disappointing growth and softening of the preferred core PCE deflator (February through April), there is talk of a dovish hike. Meanwhile, politics is front and central. UK Prime Minister May announced a cabinet reshuffle over the weekend that gave two of her former rivals (Gove and

Topics:

Marc Chandler considers the following as important: EUR, EUR/CHF, Featured, FX Daily, FX Trends, Italy Industrial Production, Japan Core Machinery Orders, Japan Producer Price Index, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.04% to 1.0856 CHF. |

EUR/CHF - Euro Swiss Franc, June 12(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesThe US dollar is trading within its pre-weekend range against the major currencies as participants await the central bank meeting starting in the middle of the week. The Federal Reserve, Bank of England, and the Bank of Japan meet. Only the Fed is expected to hike rates, but given the disappointing growth and softening of the preferred core PCE deflator (February through April), there is talk of a dovish hike. Meanwhile, politics is front and central. UK Prime Minister May announced a cabinet reshuffle over the weekend that gave two of her former rivals (Gove and Leadsom) join the cabinet, while she lost two of her close advisers. She faces the backbenchers in Parliament today. There is great uncertainty whether May survives as Prime Minister, but it is not clear either who would replace her and if they have greater support about the Tory base. Brexit negotiation was to begin shortly, and it is not clear if they will go forward and if and how the newly chastened government’s position will be modified. There were two political surprises over the weekend. First, Italy had local elections in around 1000 cities in the last flurry ahead of the national elections, which must be held by next spring. There had been some movement toward elections later this year, but the political compromise between the four largest parties unraveled last week. Hobbled by internal strife, the Five Start Movement (M5S) did particularly poorly, leaving it in a weak position to compete in the second round on June 25. Investors responded positively to the electoral developments. Italy’s 10-year bond yield is off six-seven basis points to bring the one week decline to 25 bp, and near 2%, it is near the lows for the year. Its premium over Germany has narrowed 20 bp over the past week. The premium over Spain has narrowed 10 bp at the same time. |

FX Daily Rates, June 12 - Click to enlarge |

| In France, Macron’s new party (Republic on the Move) appears to have won a little more than 31% of the vote, suggesting that in the second round it can secure 415-455 seats in the 577-seat parliament. It polled about 10% more than the center-right Republicans, the party from which the Prime Minister hails. The Socialists were decimated. It will likely see the number of seats it controls fall to 20-30 from 331. Marring the results a little was the extremely low turnout. Nevertheless, Macron efforts to reshape French politics and economics took a step forward. His signature program is labor market reforms, which seek to break the tradition of industry-wide settlements, will go full steam ahead. Macron wants the measures ready before the end of the quarter.

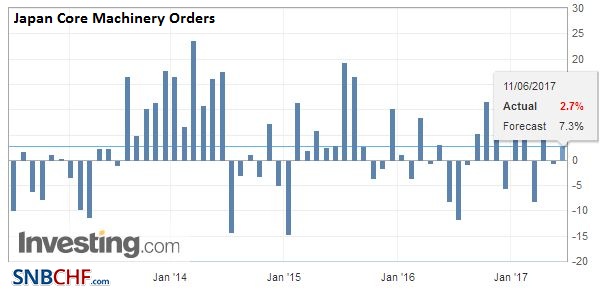

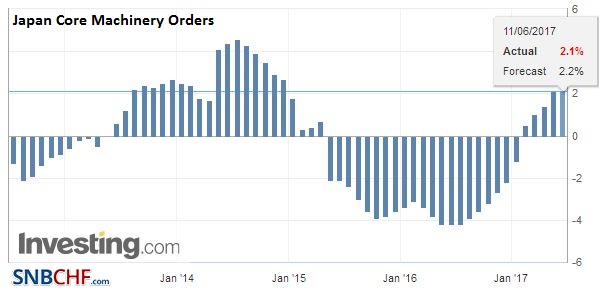

The euro extended the late recovery in the North America before the weekend into Asia and European activity today. New bids seemed to dry up as the euro approached $1.1230. Recently, it was turned lower after testing the $1.1285 area (ahead of $1.13) repeatedly. Still, despite the setback, it has not closed below the 20-day moving average (now ~$1.1205) since April 17. Sterling traded near $1.2770 in late Asia but found sellers in early European hours, pushing it back toward the lows, a little above $1.2700. The pre-weekend lows near $1.2635 seem to be inviting a retest. Finland is also facing a political challenge. A new head of the Finn’s Party threatens to undermine the fragile coalition under Prime Minister Sipila. A more outspokenly, anti-immigration, anti-EU, socially conservative-wing of the party gained control. A cabinet meeting is to be held today to determine if the current coalition can continue or if a replacement is needed. Finland’s 10-year yield is up a little, despite the decline in the other benchmark bonds in Europe. Finnish equities are off around 1%. The MSCI Asia-Pacific Index also was dragged lower by the technology sector after the losses in the US before the weekend. It was off almost 0.3%, its third consecutive losing session, the longest losing streak in a month. Losses in the region were led by information technology and/or telecoms. Japan reported softer than expected April machine orders (-3.1% compared with median expectations for 0.5% gain). It not only snapped a two-month advance, but it offset it (February rose 1.5% and March 1.4%). Despite the softer Japanese data and steady-to-firmer US yields, the dollar continues to trade heavily against the yen, perhaps amid falling equity prices. It is straddling the JPY110 level after having run out of steam before the weekend near JPY110.80. |

FX Performance, June 12 - Click to enlarge |

ItalyItalian shares are off around 0.3% in late morning turnover in Milan. It is faring better than most European equity markets today. The Dow Jones Stoxx 600 is off twice as much, led by information technology sectors that were hard-hit in the US before the weekend. Italian bank shares, however, are off 0.8%, for the second consecutive declining session. Italian large banks are considering injecting cash into two troubled regional banks which would allow a precautionary recapitalization. This would prevent having to bail-in equity investors and junior creditors. A decision is seen necessary by the middle of next week when a subordinated credit of one of the troubled banks comes due. Separately, Italy’s economic news disappointed. April industrial output fell 0.4%, snapped a two-month advance, and defying expectations for a 0.2% increase. There was hope that the Italian economy was finally catching gaining some traction. Growth in Q1 was the best since Q4 2010, but it was flattered by inventory accumulation. Business and consumer confidence softened in May. |

Italy Industrial Production YoY, April 2017(see more posts on Italy Industrial Production, ) Source: Investing.com - Click to enlarge |

Japan |

Japan Core Machinery Orders YoY, April 2017(see more posts on Japan Core Machinery Orders, ) Source: Investing.com - Click to enlarge |

Japan Producer Price Index (PPI) YoY, April 2017(see more posts on Japan Producer Price Index, ) Source: Investing.com - Click to enlarge |

United States

What promises to be an important week for the US is beginning slowly. The highlight is the FOMC meeting where a rate hike is widely expected, and nearly fully discounted. The US also reports producer and consumer price inflation, industrial output and retail sales. The investigation into Russia’s attempt to influence the US election will hear from US Attorney General Sessions tomorrow.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: $EUR,EUR/CHF,Featured,FX Daily,Italy Industrial Production,Japan Core Machinery Orders,Japan Producer Price Index,newsletter