The ECB has hinted it intends to remain flexible when it comes to the composition of future asset purchases, with a chance that corporate bonds will play a bigger role.Arguably, the most important aspect of last week’s ECB quantitative easing (QE) announcement was that the programme will remain open-ended. As we have long suggested, the pledge to extend asset purchases beyond September 2018 can only be credible if there are enough German Bunds for the ECB to buy. Bund scarcity could be addressed through a flexible approach to corporate bond purchases.Officially, the ECB did not discuss any change to QE composition or modalities. ECB President Mario Draghi said that changes in QE composition or modalities were not even discussed, because none was necessary to ensure smooth implementation

Topics:

Frederik Ducrozet considers the following as important: ECB asset purchase programme, ECB exit strategy, ECB quantitative easing, Macroview, QE composition

This could be interesting, too:

Cesar Perez Ruiz writes Weekly View – Big Splits

Cesar Perez Ruiz writes Weekly View – Central Bank Halloween

Cesar Perez Ruiz writes Weekly View – Widening bottlenecks

Cesar Perez Ruiz writes Weekly View – Debt ceiling deadline postponed

The ECB has hinted it intends to remain flexible when it comes to the composition of future asset purchases, with a chance that corporate bonds will play a bigger role.

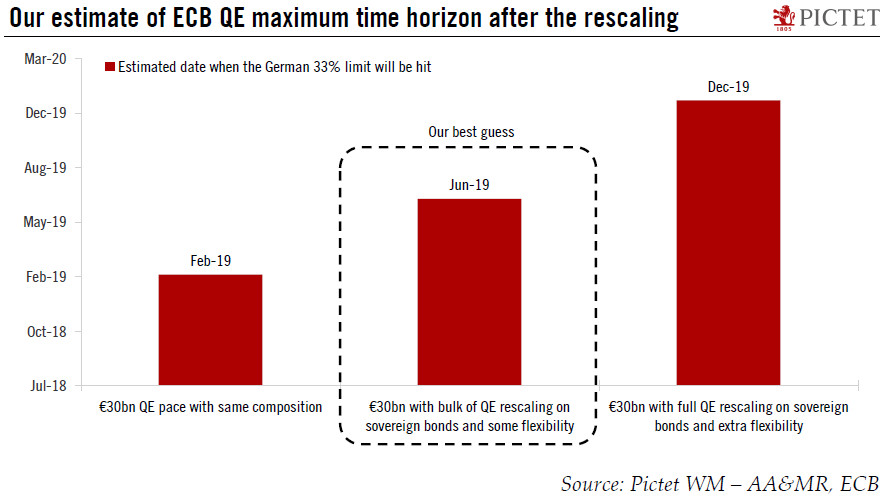

Arguably, the most important aspect of last week’s ECB quantitative easing (QE) announcement was that the programme will remain open-ended. As we have long suggested, the pledge to extend asset purchases beyond September 2018 can only be credible if there are enough German Bunds for the ECB to buy. Bund scarcity could be addressed through a flexible approach to corporate bond purchases.

Officially, the ECB did not discuss any change to QE composition or modalities. ECB President Mario Draghi said that changes in QE composition or modalities were not even discussed, because none was necessary to ensure smooth implementation of the programme. However, the ECB anticipates that private debt purchases will remain “sizeable”. This suggests to us that corporate debt purchases, in particular, will play a greater role going forward as they are unlikely to be scaled down to the same extent as public debt.

If the ECB decided to scale down QE at the full expense of sovereign debt purchases, with maximum flexibility in other parameters, then we estimate that QE could continue until the end of 2019 at a pace of EUR30bn per month. But experience from the April 2017 reduction points to an intermediate outcome.

In the end, we expect the ECB to maintain flexibility via some constructive ambiguity in terms of the composition of its asset purchases, but we lean towards a greater reduction of public bonds compared with corporate bonds. Our best guess is that the bulk of QE rescaling will fall on sovereign bond purchases, delaying the potential end-date for QE to mid-2019.

The bottom line is that while private debt purchases are unlikely to provide the ECB with a silver bullet, in an adverse scenario where QE has to be extended further, they could help mitigate scarcity constraints should QE be gradually terminated by early 2019, as per our baseline scenario.