China’s high-yield bond crisis continued last week, with yields on the ICE BofA index of Chinese high-yield US dollar bonds moving above 18% at one stage last week, the highest level in a decade. Further nervousness was caused by one real-estate issuer’s decision not to reimburse USD200 mn of offshore bonds–despite having USD4 bn in cash on its balance sheet. This suggests the company in question favours domestic investors and its own cash needs over its offshore creditors. Investors are now scrutinising other Chinese issuers with special attention to Evergrande, which is well through a 30-day grace period before its offshore investors can declare a default. Elsewhere in Asia, although subsequently batted away, hints from Japan’s new prime minister of a rise in

Topics:

Cesar Perez Ruiz considers the following as important: 2.) Pictet Macro Analysis, 2) Swiss and European Macro, Featured, Investment review, Macroview, market outlook, Market review, newsletter, Pictet, Weekly View

This could be interesting, too:

investrends.ch writes Pictet als Bester Schweizer Asset Manager im Bereich Nachhaltigkeit und Markenführung ausgezeichnet

investrends.ch writes Vom Ölschock zum Stromsuperzyklus

investrends.ch writes Pictet steigt in den Schweizer Treuhandmarkt ein – Partnerschaft mit Tretor

investrends.ch writes Die Schweiz an der Schwelle zur digitalen Transformation der Fondsindustrie

China’s high-yield bond crisis continued last week, with yields on the ICE BofA index of Chinese high-yield US dollar bonds moving above 18% at one stage last week, the highest level in a decade. Further nervousness was caused by one real-estate issuer’s decision not to reimburse USD200 mn of offshore bonds–despite having USD4 bn in cash on its balance sheet. This suggests the company in question favours domestic investors and its own cash needs over its offshore creditors. Investors are now scrutinising other Chinese issuers with special attention to Evergrande, which is well through a 30-day grace period before its offshore investors can declare a default. Elsewhere in Asia, although subsequently batted away, hints from Japan’s new prime minister of a rise in capital-gains taxes rattled Japanese equities. Ratings agency Moody’s raised India’s credit rating from negative to stable, while the Polish, and Peruvian (as well as New Zealand) central banks joined a growing number of their peers that are raising interest rates. Rate tightening to fight inflation and protect their currencies together with higher yields mean we are positive on emerging-market currencies.

The US Senate voted last week to temporarily raise the federal debt limit until the beginning of December, thereby avoiding a government shutdown, to investors’ relief. Although the debt-ceiling issue could flare up again and although Friday’s US jobs report contained plenty of food for thought (job growth was weak for the second consecutive month and wage pressure grew), we do not expect the Federal Reserve to change its plans for tapering, which we believe will be formally announced in November. Meanwhile, freight costs from China to the US are finally showing signs of easing, with a halving of the spot rate between September and October. This holds out the hope that we have seen the peak in global transportation prices, helping to relieve some current global supply issues.

Nevertheless, energy supply problems, particularly supplies of natural gas, continue to fester. But here too, there were inklings of positive news. Comments from Vladimir Putin that Russia could boost its gas supplies in order to avoid an energy crisis (while at the same time putting Russia back at the centre of European geopolitics) helped relieve some pressure on European gas prices, while the Chinese authorities’ move to order more coal production could help deal with the energy rationing that has been affecting factories in the world’s second-biggest economy. Nevertheless, it may take time for the latest announcements to have an effect. The Q3 reporting season about to start will show how rising input prices and bottlenecks are impacting companies’ margins. While constructive in the medium term, we remain neutral on global equities as we wait for more clarity on the road ahead.

You Might Also Like

House View, October 2021

House View, October 2021

2021-10-05

We maintain our tactically neutral position on equities, with the notable exception of Japan, where we see scope for a re-start to Abenomics and for Japanese stocks to continue to close their performance gap with their peers in other developed markets.

Weekly View – “The lady is not tapering”

Weekly View – “The lady is not tapering”

2021-09-14

As expected, last week the European Central Bank hinted at a “moderate” reduction of the bond buying it undertakes as part of its Pandemic Emergency Purchase Programme (PEPP). But ECB president Christine Lagarde refrained from providing a precise timeline and she was adamant that a reduction in PEPP purchases did not mean the ECB would tighten financing conditions.

Weekly View – 50 years later

Weekly View – 50 years later

2021-08-17

The rosy US employment picture helped push equities to a new high as US inflation moderated in July. Those looking to fill roles now exceed those looking for work, compelling some small and mid-sized companies to raise wages. Higher prices seem to be keeping the US consumer in check, however, with consumer sentiment hitting its lowest level in a decade.

Weekly View – Staying on script

Weekly View – Staying on script

2021-07-20

Big US banks released their 2Q earnings last week. The figures were good thanks to robust growth in investment-banking income as well as a drop in loan-loss provisions. But banks also reported that wage costs were beginning to rise, and while a booming housing market has boosted mortgage-loan business, the renewed retreat in long-term yields has been a drag on interest income.

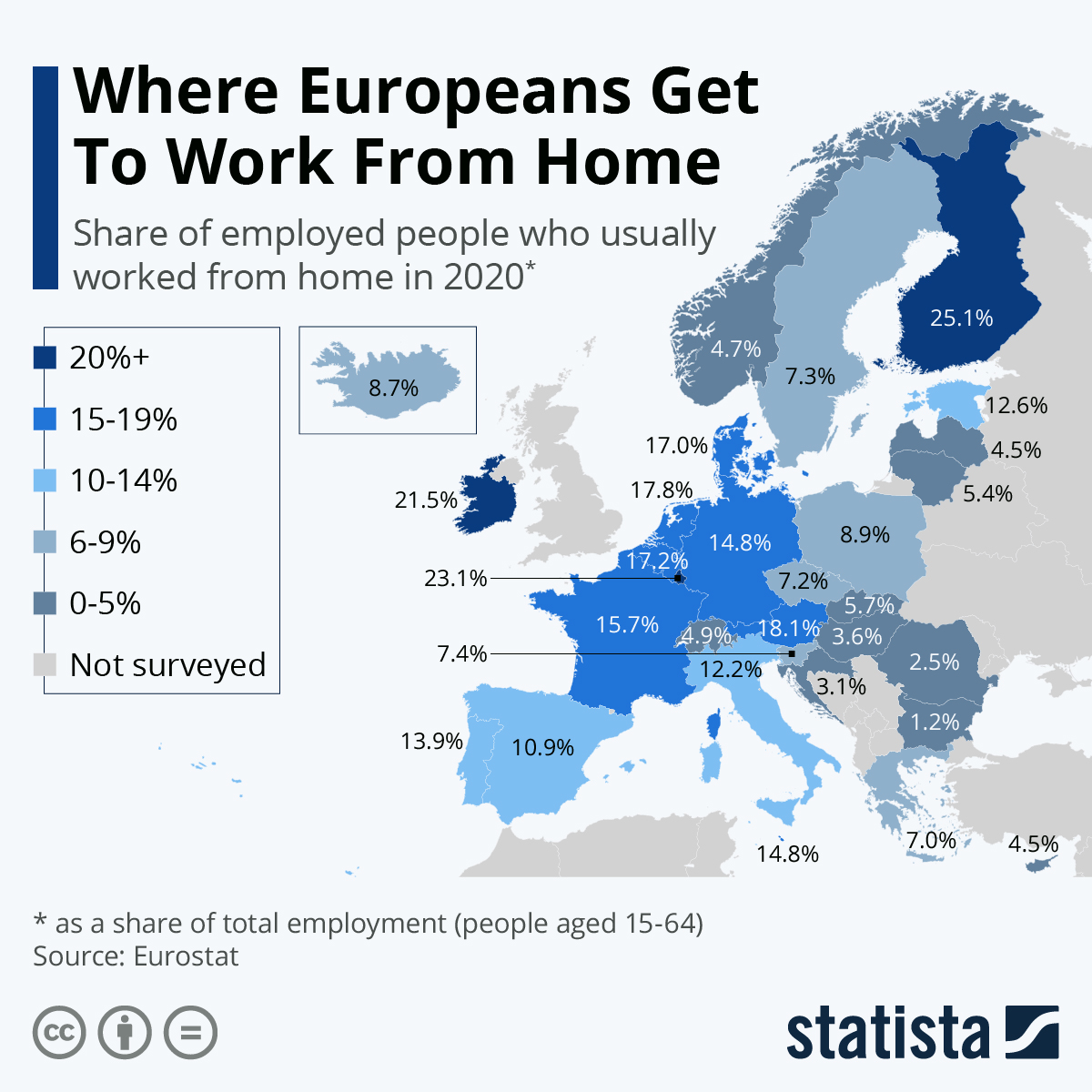

Where Europeans Get To Work From Home

Where Europeans Get To Work From Home

2021-05-20

The social distancing measures introduced in response to the Covid-19 pandemic has forced many people to work from home and accelerated the trend of remote working. Eurostat have released some interesting new data showing the share of employed people aged between 15 and 64 in Europe who usually do home office.

Swiss Consumer Price Index in April 2021: -0.3 percent YoY, +0.2 percent MoM

Swiss Consumer Price Index in April 2021: -0.3 percent YoY, +0.2 percent MoM

2021-05-10

The consumer price index (CPI) increased by 0.2% in April 2021 compared with the previous month, reaching 100.8 points (December 2020 = 100). Inflation was +0.3% compared with the same month of the previous year.

The number of MRI devices in hospitals has increased by 25 percent in 5 years

The number of MRI devices in hospitals has increased by 25 percent in 5 years

2021-04-25

23.04.2021 – In 2019, hospitals in Switzerland were equipped with 215 MRI devices, representing an increase of 25% in five years. They also had 219 scanners (+9% in five years). In total, almost 1.18 million scans and 1.06 million MRI screenings were carried out in Switzerland in 2019.

Three-quarters of employees in Switzerland record their working hours

Three-quarters of employees in Switzerland record their working hours

2021-04-19

19.04.2021 – In 2019, 73.9% of employees in Switzerland registered their working hours, whereas in the European Union (EU) only 58.1% did so. In European comparison, fixed working hours were less common in Switzerland (49.2%; EU: 60.1%) and more employed persons enjoyed a high level of job autonomy (60.4%; EU: 50.6%).

Tags: Featured,Investment review,Macroview,market outlook,Market review,newsletter,Pictet,Weekly view