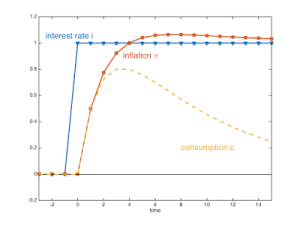

On his blog, John Cochrane offers a stripped down model and some intuition for why inflation would rise after an increase in the interest rate. The model features the usual Euler (IS) equation and a Mickey Mouse Phillips curve—inflation is proportional to consumption (or output). The intuition: During the time of high real interest rates — when the nominal rate has risen, but inflation has not yet caught up — consumption must grow faster [the Euler equation, DN]. … Since more consumption pushes up prices, giving more inflation, inflation must also rise during the period of high consumption growth. Also: I really like that the Phillips curve here is so completely old fashioned. This is Phillips’ Phillips curve, with a permanent inflation-output tradeoff. That fact shows squarely where the neo-Fisherian result comes from. The forward-looking intertemporal-substitution IS equation is the central ingredient. A slightly more plausible model with an accelerationist Phillips curve and very slowly adjusting adaptive expectations yields the following responses to an increase in the nominal interest rate: John writes: As you can see, we still have a completely positive response. Inflation ends up moving one for one with the rate change. Consumption booms and then slowly reverts to zero.

Topics:

Dirk Niepelt considers the following as important: *, Fisher equation, inflation, inflation expectations, Interest Rate, Learning, Notes, Real interest rate

This could be interesting, too:

Dirk Niepelt writes Does the US Administration Prohibit the Use of Reserves?

Dirk Niepelt writes “Report by the Parliamentary Investigation Committee on the Conduct of the Authorities in the Context of the Emergency Takeover of Credit Suisse”

Marc Chandler writes Yen Jumps on Rate Hike Speculation

Claudio Grass writes Gold climbing from record high to record high: why buy now?

On his blog, John Cochrane offers a stripped down model and some intuition for why inflation would rise after an increase in the interest rate. The model features the usual Euler (IS) equation and a Mickey Mouse Phillips curve—inflation is proportional to consumption (or output). The intuition:

During the time of high real interest rates — when the nominal rate has risen, but inflation has not yet caught up — consumption must grow faster [the Euler equation, DN]. … Since more consumption pushes up prices, giving more inflation, inflation must also rise during the period of high consumption growth.

Also:

I really like that the Phillips curve here is so completely old fashioned. This is Phillips’ Phillips curve, with a permanent inflation-output tradeoff. That fact shows squarely where the neo-Fisherian result comes from. The forward-looking intertemporal-substitution IS equation is the central ingredient.

A slightly more plausible model with an accelerationist Phillips curve and very slowly adjusting adaptive expectations yields the following responses to an increase in the nominal interest rate:

John writes:

As you can see, we still have a completely positive response. Inflation ends up moving one for one with the rate change. Consumption booms and then slowly reverts to zero. …

The positive consumption response does not survive with more realistic or better grounded Phillips curves. With the standard forward looking new Keynesian Phillips curve inflation looks about the same, but output goes down throughout the episode: you get stagflation.

A November 2015 paper on the topic by James Bullard.

A critique by Mariana García-Schmidt and Michael Woodford in an NBER working paper. Abstract:

We illustrate a pitfall that can result from the common practice of assessing alternative monetary policies purely by considering the perfect foresight equilibria (PFE) consistent with the proposed rule. In a standard New Keynesian model, such analysis may seem to support the “Neo-Fisherian” proposition according to which low nominal interest rates can cause inflation to be lower. We propose instead an explicit cognitive process by which agents may form their expectations of future endogenous variables. Under some circumstances, a PFE can arise as a limiting case of our more general concept of reflective equilibrium, when the process of reflection is pursued sufficiently far. But we show that an announced intention to fix the nominal interest rate for a long enough period of time creates a situation in which reflective equilibrium need not resemble any PFE. In our view, this makes PFE predictions not plausible outcomes in the case of such policies. Our alternative approach implies that a commitment to keep interest rates low should raise inflation and output, though by less than some PFE analyses apply.

On his blog, Stephen Williamson addresses “Neo-Fisherian Denial.” Williamson starts with the model analyzed by Cochrane (see above) featuring a Mickey Mouse Phillips curve. He argues:

[This] NK model actually doesn’t conform to conventional central banking beliefs about how monetary policy works. What’s going on? … an increase in the current nominal interest rate will increase the real interest rate, everything else held constant. This implies that future consumption (output) must be higher than current consumption, for consumers to be happy with their consumption profile given the higher nominal interest rate. But, it turns out that this is achieved not through a reduction in current output and consumption, but through an increase in future output and consumption. This serves, through the Phillips curve mechanism, to increase future inflation relative to current inflation. Then, along the path to the new steady state, output and inflation increase.

Williamson recalls the “perils” of Taylor rules. And he addresses the critique by Garcia-Schmidt and Woodford:

Some people (e.g. Garcia-Schmidt and Woodford) have argued that Neo-Fisherian results go out the window in NK models under learning rules. As was shown above, these models are always fundamentally Fisherian in that any monetary policy rule has to somehow adhere to Fisherian logic on average – basically the long-run nominal interest rate is the inflation anchor. But there can also be learning rules that give very Fisherian results. …

Williamson also argues that other (non-Keynesian) monetary models give neo-Fisherian results as well.

A few years ago, also on his blog, Stephen Williamson argued that lowering the interest rate (by engaging in QE) might also affect the real interest rate:

… short-run liquidity effects are short-lived. Further, my work shows that there is another liquidity effect, associated with the interest bearing liquid assets, that causes the long run real rate to increase as a result of QE. … which implies lower inflation.

Further, there are other forces in play … The destruction of private sources of collateral and the shaky state of sovereign governments in parts of the world gave U.S. government debt a large liquidity premium – i.e. those things reduced real interest rates. As those effects go away over time, real rates of return will rise, shifting up the long-run Fisher relation, and reducing inflation if the Fed keeps the nominal interest rate at the zero lower bound.

In a paper, Peter Rupert and Roman Sustek dig deeper. In the abstract they write:

The monetary transmission mechanism in New-Keynesian models is put to scrutiny, focusing on the role of capital. We demonstrate that, contrary to a widely held view, the transmission mechanism does not operate through a real interest rate channel. Instead, as a first pass, inflation is determined by Fisherian principles, through current and expected future monetary policy shocks, while output is then pinned down by the New-Keynesian Phillips curve. The real rate largely only reflects consumption smoothing. In fact, declines in output and inflation are consistent with a decline, increase, or no change in the ex-ante real rate.

Addendum (May 11–12, 2016): In the abstract of their NBER working paper, Julio Garín, Robert Lester and Eric Sims write:

Increasing the inflation target in a textbook New Keynesian (NK) model may require increasing, rather than decreasing, the nominal interest rate in the short run. We refer to this positive short run co-movement between the nominal interest rate and inflation conditional on a nominal shock as Neo-Fisherianism. We show that the NK model is more likely to be Neo-Fisherian the more persistent is the change in the inflation target and the more flexible are prices. Neo-Fisherianism is driven by the forward-looking nature of the model. Modifications which make the framework less forward-looking make it less likely for the model to exhibit Neo-Fisherianism. As an example, we show that a modest and empirically realistic fraction of “rule of thumb” price-setters may altogether eliminate Neo-Fisherianism in the textbook model.

In his 2008 textbook, Jordi Gali discusses the role of the persistence of monetary policy shocks (page 51). If it is sufficiently persistent, a contractionary monetary policy shock raises the real rate (and lowers output) but decreases the nominal rate, due to the

decline in inflation and the output gap more than offsetting the direct effect [of the shock].