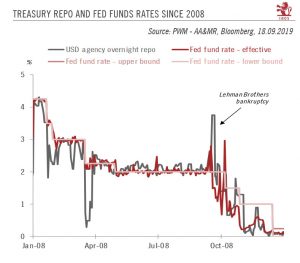

Following this week’s sharp movement in the USD overnight repurchase agreement (repo) rate, people are wondering what the US Federal Reserve (Fed) can do to counter a similar event in the future.One measure of the USD overnight repo rate (there exist several) spiked to 6% on Tuesday 17 September, probably due a scarcity of bank reserves at the Fed at a time when US corporates needed cash to pay their taxes as did investors/banks (probably to absorb strong US Treasury issuance. Hence, cash became dearer, and its scarcity led to a spike in the overnight repo rate. It is unusual to see such a spike in September, although it is quite normal at the end of each calendar year. There was a similar sharp rise in September 2008, coinciding with the Lehman Brothers collapse. At this stage we do not

Read More »Goodbye quantitative tightening

September 20, 2019