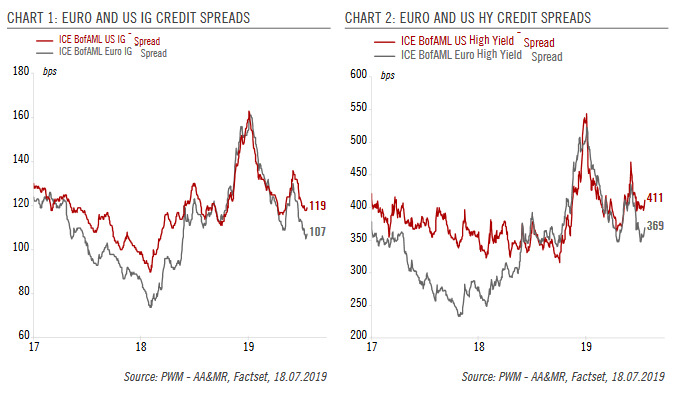

Despite the impressive year-to-date performance of corporate credit, we remain prudent about prospects in the remainder of 2019. Corporate bonds have posted stellar total returns year to date, thanks to the positive combination of lower sovereign yields and tighter credit spreads. While high yield (HY) bonds have performed slightly better than investment grade (IG) ones on both sides of the Atlantic, the additional return from taking more risk remains thin. As cracks continue to appear in both the US and Europe, with the manufacturing sector facing a global slowdown, it becomes all the more important to look at corporate fundamentals. In this regard, one notes a rise in the leverage ratio across the board from

Topics:

Laureline Chatelain considers the following as important: 2) Swiss and European Macro, corporate debt, DM credit, euro investment grade, Featured, Macroview, newsletter, Pictet Macro Analysis, US high yield

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

Despite the impressive year-to-date performance of corporate credit, we remain prudent about prospects in the remainder of 2019. Corporate bonds have posted stellar total returns year to date, thanks to the positive combination of lower sovereign yields and tighter credit spreads. While high yield (HY) bonds have performed slightly better than investment grade (IG) ones on both sides of the Atlantic, the additional return from taking more risk remains thin. As cracks continue to appear in both the US and Europe, with the manufacturing sector facing a global slowdown, it becomes all the more important to look at corporate fundamentals. In this regard, one notes a rise in the leverage ratio across the board from already high levels in Q1 2019. It remains to be seen whether the Q2 earnings season underway confirms this negative trend. Adding to concerns, default rates have gone up in both the US and Europe, although the rate remains very low in euro HY (1.1% in June). Finally, after a drop in gross issuance in 2018 versus 2017, issuance has risen this year so far in two segments, US HY and euro IG, a trend we expect to continue in H2. |

EURO AND US IG CREDIT SPREADS - Click to enlarge |

Overall, we remain prudent on corporate debt, favouring quality. We expect credit spreads to remain broadly in line with current levels. Despite rising support from the Federal Reserve (which we expect to cut rates twice this year) and the European Central Bank (which should re-start QE and cut the deposit rate once before the end of 2019), we see limited space for significantly tighter spreads as long as economic growth continues to slow in both regions.

We are neutral on US and euro IG bonds. We have recently turned neutral from underweight on euro HY bonds due to our expectations of renewed quantitative easing from the European Central Bank and relatively favourable fundamentals. By contrast, we remain underweight on US HY.

Tags: corporate debt,DM credit,euro investment grade,Featured,Macroview,newsletter,US high yield