Last week was only four days due to the President’s day holiday but it was eventful. The big news of the week was the spike in interest rates, which according to the press reports I read, “came out of nowhere”. In other words, the writers couldn’t find an obvious cause for a 14 basis point rise in the 10 year Treasury note yield so they just chalked it up to mystery. Of course, anyone who’s been paying attention knows that rates have been rising for almost a year – and quite steadily since the beginning of August – so how this last 14 basis points qualifies as a surprise I’m not sure. What was an actual surprise was mostly missed by the market commentators – the rise in real rates. The 10 year TIPS yield closed the week at -80 basis points which says very little

Topics:

Joseph Y. Calhoun considers the following as important: 5.) Alhambra Investments, Alhambra Research, banks, bonds, commodities, Copper, currencies, economic growth, economy, employment, Featured, growth stocks, inflation, jobless claims, Labor market, Markets, newsletter, stocks, TIPS, US dollar, value stocks, Yield Curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Last week was only four days due to the President’s day holiday but it was eventful. The big news of the week was the spike in interest rates, which according to the press reports I read, “came out of nowhere”. In other words, the writers couldn’t find an obvious cause for a 14 basis point rise in the 10 year Treasury note yield so they just chalked it up to mystery. Of course, anyone who’s been paying attention knows that rates have been rising for almost a year – and quite steadily since the beginning of August – so how this last 14 basis points qualifies as a surprise I’m not sure.

What was an actual surprise was mostly missed by the market commentators – the rise in real rates. The 10 year TIPS yield closed the week at -80 basis points which says very little good about the US economy. On the other hand it is 26 basis points higher than it was a mere 6 trading days ago so it is – finally – moving in the right direction. Or so it would seem. The press was right about one thing – there really wasn’t much on the economic front to explain the move in real or nominal rates. The selloff in the long end of the nominal curve may be more a function of bank balance sheet capacity than anything else. If so, the implications are probably not as positive as the market, the Fed and the financial press would have us believe. And if the coming end of the Fed’s SLR reprieve is affecting nominal Treasuries it seems likely it is affecting TIPS as well, maybe more so given more limited liquidity in that market.

Whatever the cause, it is generally a good sign when real rates are rising, an indication that inflation fears are waning and real growth expectations are rising. But arguably better news is that the real yield curve moved in a positive way last week. There has been plenty of commentary recently about the nominal yield curve steepening but very little about the real yield curve. Both have been steepening but in different ways with conflicting messages. A steepening curve is generally taken as a positive, an indication that growth expectations are rising.

The nominal curve has been steepening recently because long term rates have been rising while short term rates have stayed the same (or fallen depending on where you are looking). But that, by itself is not an argument for better economic growth. In this case, because long term TIPS yields have been falling, the steepening of the nominal curve has actually been all about rising inflation fears. To get an indication of real growth expectations you need to watch the real yield curve too.

| The TIPS curve has been steepening too but not in the same way. Short term TIPS yields have been falling faster than long term TIPS yields, the curve steepening as a result. Why would that be? Well, it isn’t from anything good I can tell you that. Falling short term rates is generally associated with deteriorating economic growth conditions not improving. We’ve seen this recently in the short end of the nominal curve too with T-Bill rates falling. The difference is that TIPS yields have no problem going negative and they have in a big way.

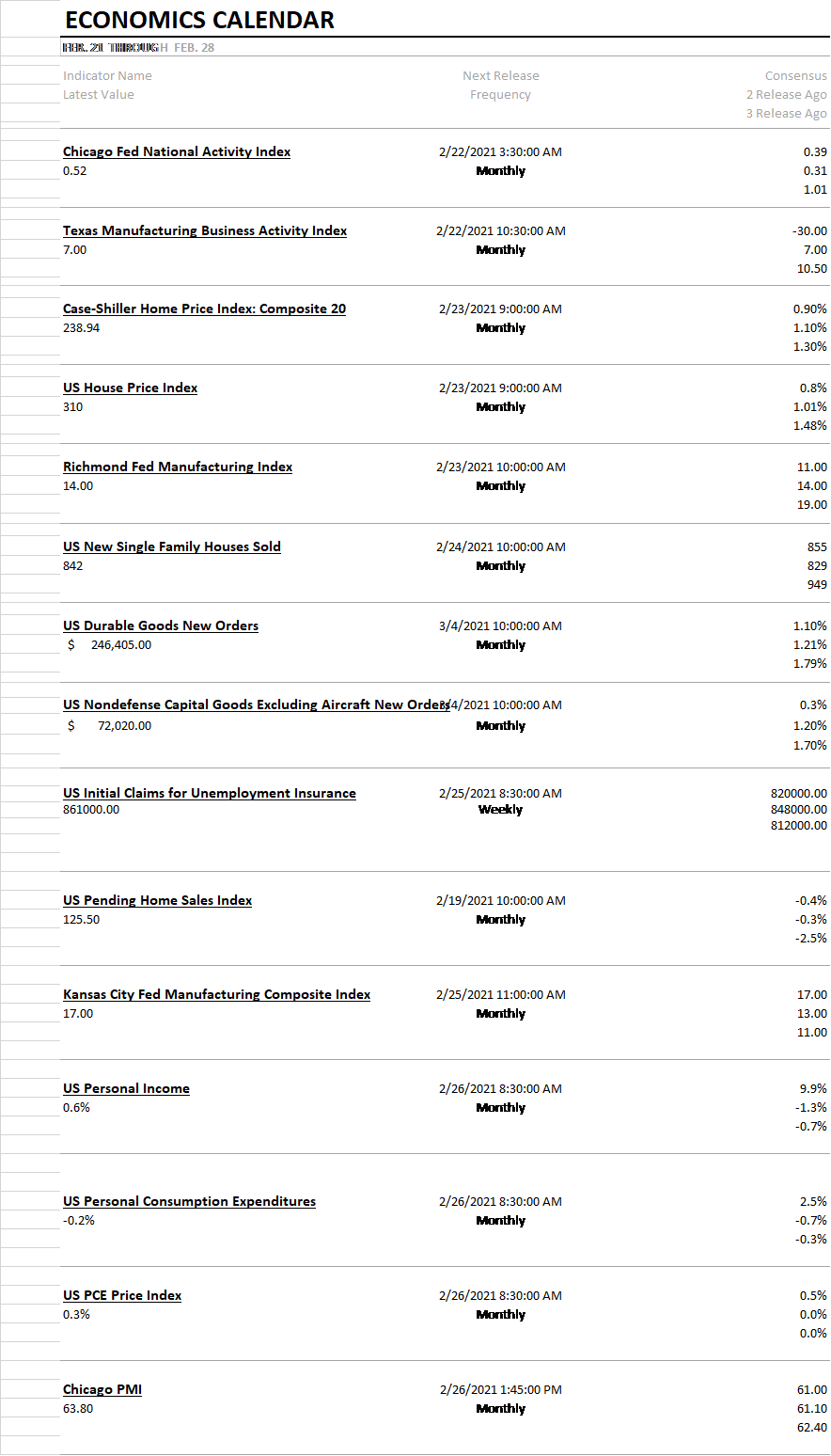

But last week saw some improvement in growth expectations as both long and short term TIPS yields rose. More importantly I think, long term rates rose more than short term rates, further steepening the curve. It is ironic that much of the commentary last week that did attempt to place blame for rising nominal rates fingered inflation fears. Ironic because rising TIPS yields is an indication that markets are becoming less concerned about inflation not more. And if the market commentators had taken a few minutes to compare real and nominal bond yields they would have noticed that inflation expectations actually fell last week. Longer term, I have serious concerns about growth not least because of that bank balance sheet capacity problem I mentioned above. Bank balance sheets are currently stuffed with Treasuries and the Biden administration seems intent on making sure that doesn’t change any time soon. Believing that government spending can create lasting, sustainable growth is the ultimate triumph of hope over experience. For now, markets are happy that the virus is ebbing and government spending is still ramping up but I do wonder what the Biden administration will do for an encore. The most interesting reports for next week will probably be the Dallas Fed since Texas has been shut down for the last week, new home sales since housing starts were down last week and personal income and spending because of the recent government transfers and the surge in retail sales reported last week. And of course, jobless claims are anybody’s guess at this point. |

. |

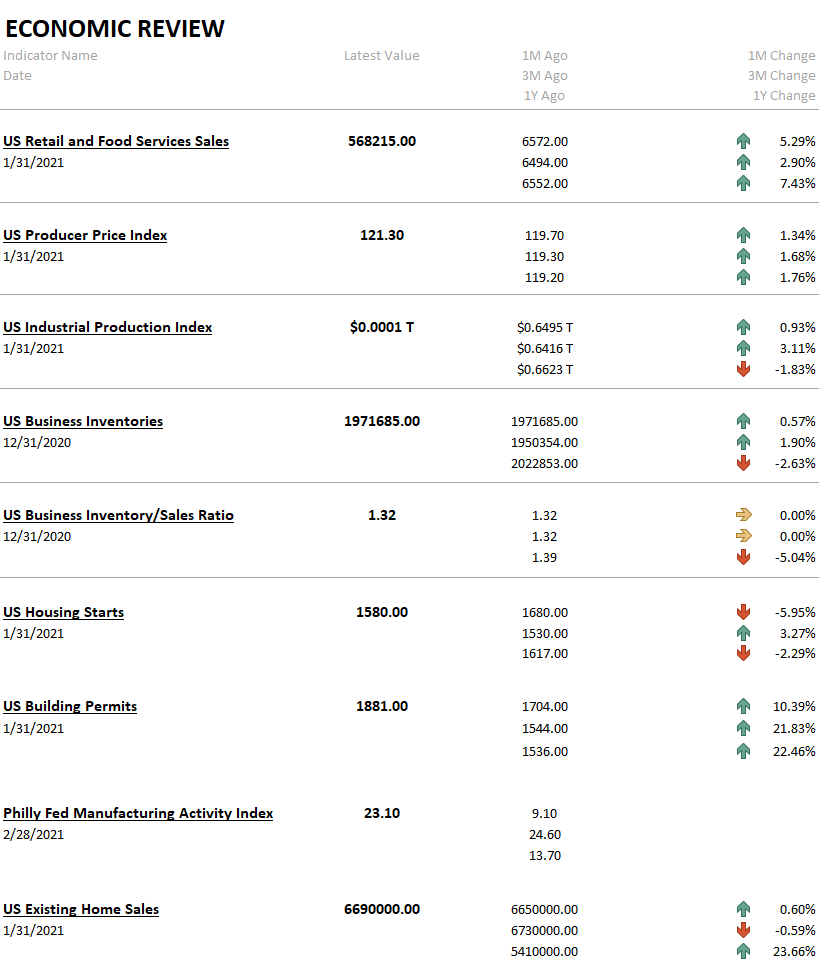

| Last week’s economic reports were mostly positive and better than expected. Retail sales were up much more than expected and that seems great on the surface but it is also a bit depressing. I suspect that retail sales were up so much because a lot of people had put off shopping – maybe important necessary shopping – waiting for government assistance that didn’t pass until late December. In the past, one time tax rebates like the $600 checks, have been saved not spent. I suppose that could be changing but if it is, that would not seem to be a good sign.

Producer prices were up more than expected and several other measures of inflation not listed here were also said to be hot but I didn’t see much to worry about – yet. The inventory report was a non-event. The inventory/sales ratio shows things well under control. Housing starts were a bit disappointing but permits surged by 10%. The Philly Fed report was better than expected and existing home sales surprised to the upside. The housing market remains on fire just about everywhere. Jobless claims continue to be the insect in the bouillabaisse when it comes to economic stats. Weekly claims over 800k just isn’t healthy and points to continued weakness. But the labor market is very confusing right now. Blue collar jobs in certain industries are booming and Midwest cities are kicking the coasts behind for a change. There are big changes afoot in the labor market and I’m not sure we’ll know for some time exactly what they are and how the economy will change as a result. We know, for instance, that labor market participation has fallen but whether that is good or bad is harder to predict. Are we better off as a society with fewer people working and more parents staying home? In a way, isn’t that what we should be trying to do as a society? Is maximizing output the only worthy goal of our economy? If the pandemic forced companies and individuals to be more creative and productive isn’t that good thing? Maybe fewer people in the formal workforce and more in the family/home sector will prove beneficial to society and economic output. Just a few things to ponder before we just assume that all the lost jobs of the last year really need to be replaced. Maybe extending unemployment benefits repeatedly is just a test run of a universal basic income. Economics is about human behavior and one thing I know for sure is that predicting it is near impossible. |

. |

| I continue to see the economic environment as one characterized by a weak dollar and rising growth. The dollar is trying to stabilize though and rising real rates should help in that regard (and is generally a negative for gold). Growth prospects continue to improve but the long term trend for growth is probably worse today than it was prior to COVID. But it will likely be quite a while before the crowd recognizes that fact. |

. |

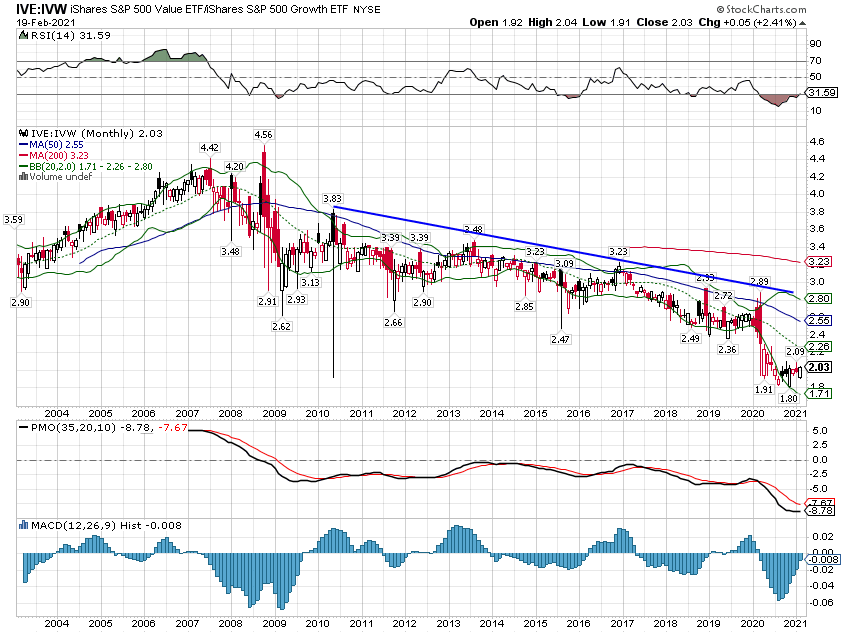

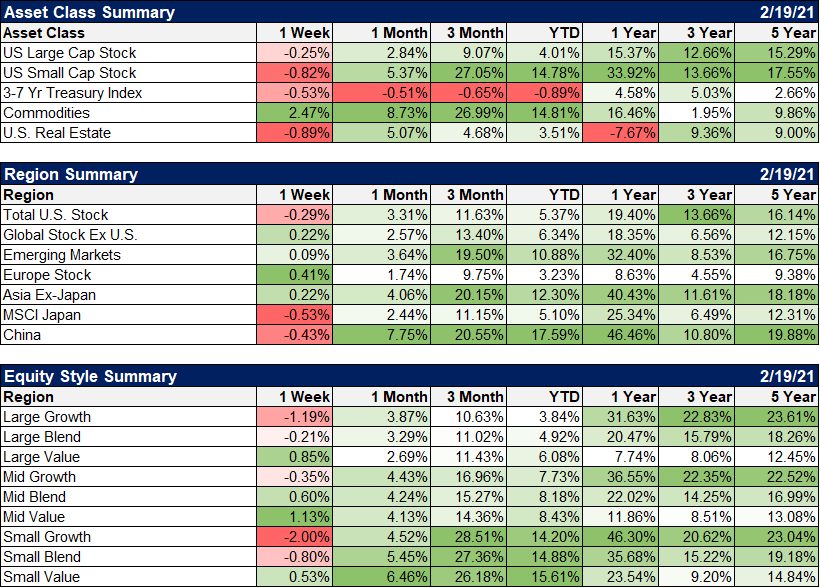

MarketsUS stocks took a breather last week but global stocks managed a small gain. Europe turned in a good week and Asia was higher although Japan and China both fell slightly. EM also managed a small gain and continues to lead over the last year. But last week was a great big nothing in the big picture. Value was the clear winner last week and that is a trend I expect to continue. It is what we generally expect in a weak dollar environment and at least for now that’s where we are. There are also ample fundamental and technical reasons to expect a reversion, at least, to the previous trend. Don’t make it more complicated than it is; momentum has been shifting in favor of value since the fall. When it gets back up to the old trend we’ll face a decision but for now, value is the obvious choice. |

iShares S&P 500, 2004-2021 - Click to enlarge |

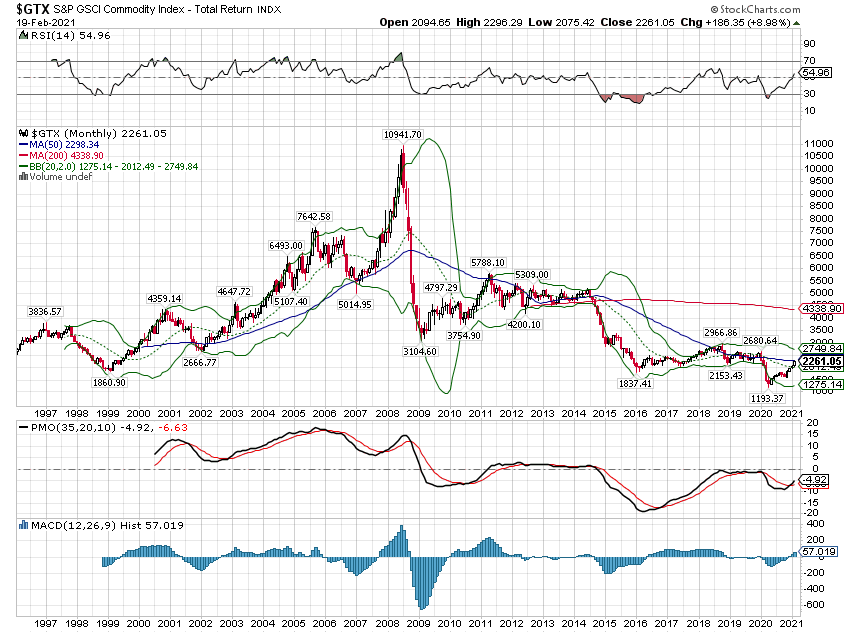

| Of the five major asset classes in our portfolios, commodities were the only winner last week. Most commodities, even after the big recent moves, are nowhere near their all time highs. Crude oil at $60 is less than half its peak. Platinum has made a big move recently but it’s a $1000 below its all time high. Copper is near a 10 year high but that is a bit of an outlier. Overall, the recent move up in commodities came from such lows that we haven’t even broken the 2018 highs. And the 2018 highs were not very high. All the talk about inflation and commodity super cycles is wildly overblown at this point. We may indeed be on the cusp of a very big move in commodities but we aren’t there yet. Not even close. |

S&P GSCI Commodity Index, 1997-2021 - Click to enlarge |

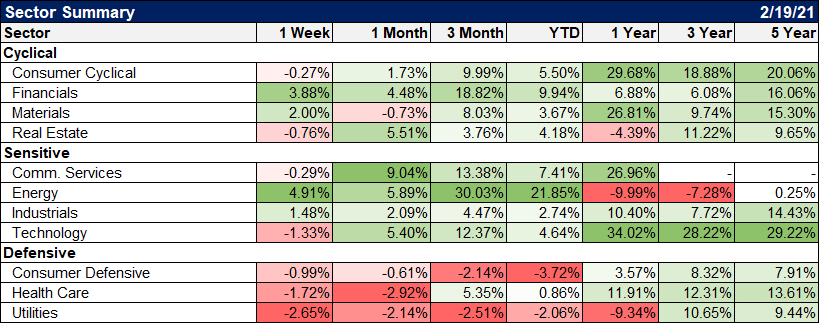

| The winning sectors last week were financials and energy, two value sectors. Utilities were the big losers but I’m not sure if that was because it is a defensive sector or because they performed so poorly in Texas. Maybe a bit of both. |

. |

. |

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

2021-02-22

Update February 22 2021: SNB intervening. Sight Deposits have risen by +0.1 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +0.1 bn. compared to last week.

Two Seemingly Opposite Ends Of The Inflation Debate Come Together

Two Seemingly Opposite Ends Of The Inflation Debate Come Together

2021-02-19

It’s worth taking a look at a couple of extremes, and the putting each into wider context of inflation/deflation. As you no doubt surmise, only one is receiving much mainstream attention. The other continues to be overshadowed by…anything else.

Politics Get Weird, Markets Don’t Care

Politics Get Weird, Markets Don’t Care

2021-01-19

A mob, led by a shirtless man wearing a Viking helmet, stormed the Capitol building a couple of weeks ago and five people died before order was restored. A man from upstate New York sat in a Senator’s office and smoked a joint. Another roamed the halls of Congress with a Confederate flag.

Don’t Really Need ‘Em, Few More Nails Anyway

Don’t Really Need ‘Em, Few More Nails Anyway

2020-12-06

The ISM’s Non-manufacturing PMI continued to decelerate from its high registered all the way back in July 2020. In that month, the headline index reached 58.1, the best since early 2019, and for many signaling that everything was coming up “V.”

Monthly Macro Monitor – September 2020

Monthly Macro Monitor – September 2020

2020-09-30

The economic data over the last month continued to improve but the breadth of improvement has narrowed. Additionally, while most of the economic data series are still improving, the rate of change, as Jeff pointed out recently, has slowed. I guess that isn’t that surprising as the initial phase of the recovery comes to an end.

Uh Oh, The Dollar Has Caught A Bid

Uh Oh, The Dollar Has Caught A Bid

2020-09-24

Anyone who follows Alhambra knows that we keep an eye on the dollar. It is a very important part of our process of identifying the economic environment. A rising dollar, when combined with a falling rate of growth, can be a lethal combination. That was the situation in March and of course during the financial crisis of 2008.

Tags: Alhambra Research,banks,Bonds,commodities,Copper,currencies,economic growth,economy,employment,Featured,growth stocks,inflation,jobless claims,Labor Market,Markets,newsletter,stocks,TIPS,US dollar,value stocks,Yield Curve