Marc Chandler

November 10, 2018

SNB & CHF

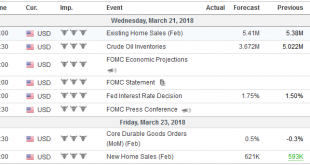

The Federal Reserve kept policy on hold, and its sparse statement gave little clue as to what it makes of the pressures in the money markets or the weakness in the housing market. The effective Fed funds rate is bumping against the cap provided by the interest rate on reserves. Some repo rates, like SOFR (the intended replacement for LIBOR), have on occasion poked above what should be the ceiling. The housing market is...

Read More »

Jeffrey P. Snider

September 28, 2018

SNB & CHF

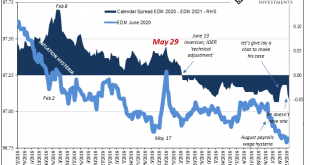

June 13 sticks out for both eurodollar futures as well as IOER. On the surface, there should be no bearing on the former from the latter. They are technically unrelated; IOER being a current rate applied as an intended money alternative. Eurodollar futures are, as the term implies, about where all those money rates might fall in the future.

Still, the eurodollar curve inverted conspicuously starting June 13. That was...

Read More »

Jeffrey P. Snider

September 16, 2018

SNB & CHF

Cushing, OK, delivered what it could for the CPI. The contribution to the inflation rate from oil prices was again substantial in August 2018. The energy component of the index gained 10.3% year-over-year, compared to 11.9% in July. It was the fourth straight month of double digit gains.

Yet, the CPI headline retreated a little further than expected. After reaching the highest since December 2011 the month before,...

Read More »

Marc Chandler

August 3, 2018

SNB & CHF

There was little doubt in the market’s collective mind that the Federal Reserve, which hiked rates in July, would stand pat today. It did not disappoint.

The statement itself was almost identical. Growth was said to be “strong” instead of “solid,” for example, a nuance to be lost on most observers. It recognized that the unemployment rate stabilized after falling.

Most notable is what is not included. The June minutes...

Read More »

Marc Chandler

June 13, 2018

SNB & CHF

The US dollar is trading firmly as the FOMC decision looms. In many ways, the actionable outcome of this meeting has hardly been in doubt this year. By all accounts, the Fed will deliver its second hike of the year today.

The question is not so much about the next meeting in August. The Fed has only hiked rates at meetings that a press conference follows. This is the source of one of our persistent criticisms of the...

Read More »

Marc Chandler

May 21, 2018

SNB & CHF

There are several trends in the capital markets at a high-level. The euro and yen’s decline has coincided with sustained rallies in European and Japanese equity benchmarks. Emerging market equities and currencies have been trending lower.

There are two other trends that arguably are reinforcing if not causing the other trends. Both oil prices and U0S interest rates have been trending higher. It is unusual but not...

Read More »

Marc Chandler

May 5, 2018

SNB & CHF

The US jobs report was broadly disappointing. However, the Federal Reserve will look through it and investors should too. A June hike is still by far the most likely scenario.

The US created 164k net new jobs in April, and when coupled with the 32k upward revision in March, it was near expectations. The source of disappointment hourly earnings. March’s 2.7% year-over-year pace was revised to 2.6%, and there it remained...

Read More »

Marc Chandler

March 19, 2018

SNB & CHF

The most significant event in the coming week is the first FOMC meeting under the Chair Powell. At ECB President Draghi’s first meeting he cut interest rates. He cuts rates at his second meeting as well, underwinding the two hikes the ECB approved under Trichet. At BOJ Governor Kuroda’s first meeting, an aggressive monetary policy was announced that was notable not only in its size, but also in the range of assets to be...

Read More »

Jeffrey P. Snider

January 22, 2018

SNB & CHF

There’s nothing especially special about 2.62%. It’s a level pretty much like any other, given significance by only one phrase: the highest since 2014. It sounds impressive, which is the point. But that only lasts until you remember the same thing was said not all that long ago.

Back last March, the 10-year yield had then, like now, broke above 2.60%. In doing so, it surpassed the previous recent high set in December...

Read More »

Jeffrey P. Snider

January 19, 2018

SNB & CHF

When Federal Reserve officials first started last year to mention wireless network data plans as a possible explanation for a fifth year of “transitory” factors holding back consumer price inflation, it seemed a bit transparent. One of the reasons for immediately doubting their sincerity was the history of that particular piece of the CPI (or PCE Deflator). To begin with, the unlimited data plan wars that kicked off...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org