It’s not recession fears, those are in the past. For much if not most (vast majority) of mainstream pundits and newsmedia alike, unlike regular folks this is all news to them (the irony, huh?) Economists and central bankers everywhere had said last year was a boom, a true inflationary inferno raging worldwide. For once, CPIs (or European HICPs) seemed to have confirmed the narrative. Unlike 2018 when inflation indices kept policymakers and their forecasts out in the cold, 2021 sure appeared to be different. Yet, it wasn’t. Apart from specific price behavior (supply shock, neither money printing nor an overheating economy), the underlying not-recovery pattern has repeated. Markets worldwide picked up on these key distinctions which, as usual, were never reported

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, currencies, ECB, economy, Europe, Featured, Federal Reserve/Monetary Policy, Germany, inflation, Markets, newsletter, PMI, rate hikes, Recession, sentiment

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| It’s not recession fears, those are in the past. For much if not most (vast majority) of mainstream pundits and newsmedia alike, unlike regular folks this is all news to them (the irony, huh?) Economists and central bankers everywhere had said last year was a boom, a true inflationary inferno raging worldwide.

For once, CPIs (or European HICPs) seemed to have confirmed the narrative. Unlike 2018 when inflation indices kept policymakers and their forecasts out in the cold, 2021 sure appeared to be different. Yet, it wasn’t. Apart from specific price behavior (supply shock, neither money printing nor an overheating economy), the underlying not-recovery pattern has repeated. Markets worldwide picked up on these key distinctions which, as usual, were never reported by any outlet. Because of this, the current levels of, and more so the well-established now-accelerating direction toward, weakness is to those unaware as if something new has happened. Blindsided by downturn and more, suspicion can only be cast upon the “hawkish” Fed (or ECB). What else could it be? |

. |

| Not a single central bank had been anywhere close to its current position(s) way back in the middle of last year. Powell’s FOMC hadn’t yet thought about the word taper, let alone the idea of several fifties maybe seventy-fives rate hikes added to hastened QT. Those latter are brand new, but, again, economic weakness and market projections for downturn go back to when policymakers were still more concerned about, well, weakness than inflation.

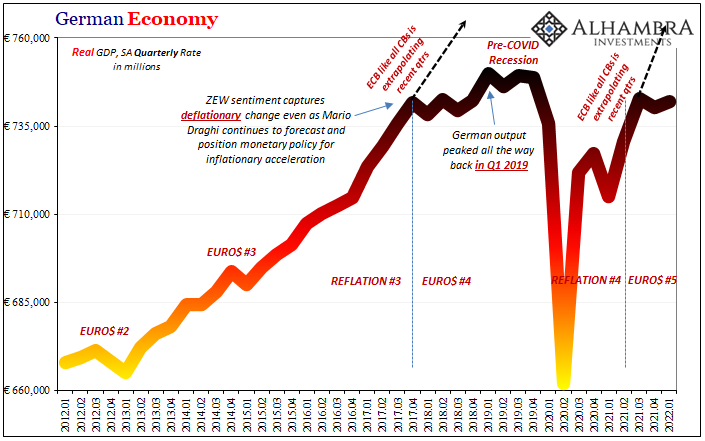

Doubly if not triply-so for the Europeans. That’s what makes Europe’s careening toward recession so important to appreciate. The ECB is only just this month starting to move more “hawkishly”, yet just like the US and Chinese downturn theirs goes back to the middle of last year, too. |

. |

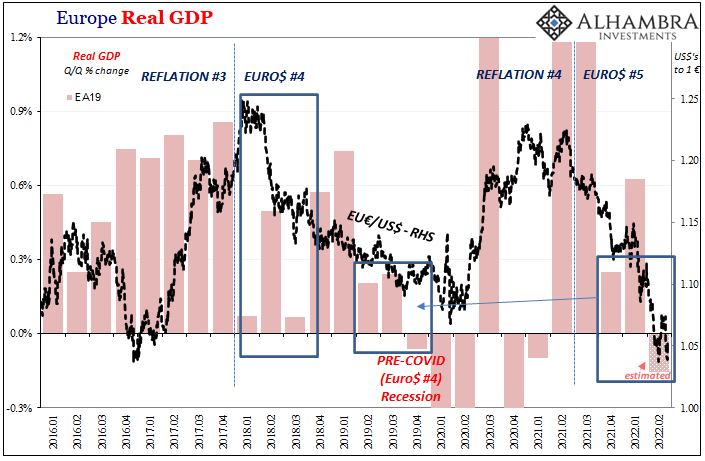

| April. May. June. 2021 when it all really began. Not 2022.

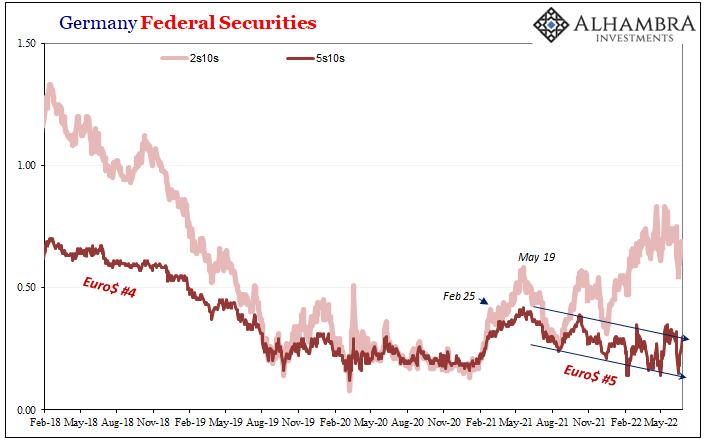

QE-on, QE-off. No rate hikes, rate hikes, extra-vulgar rate hikes. America, Europe. No correlation whatsoever with economic data nor market(s) behavior. This thing is globally synchronized Euro$ #5, the only factor which ties everything together and can explain all the facts everywhere around the world. Among those facts is a substantial further deterioration in sentiment first. PMI data for the US sank, as it has for European countries. Again, Fed vs. ECB, yet same result economy. |

. |

. |

|

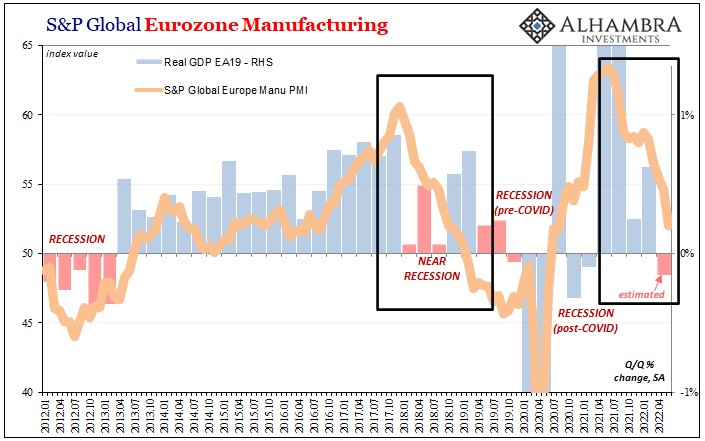

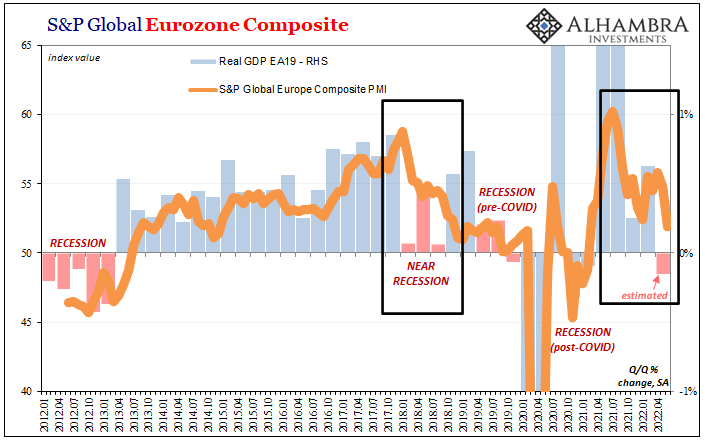

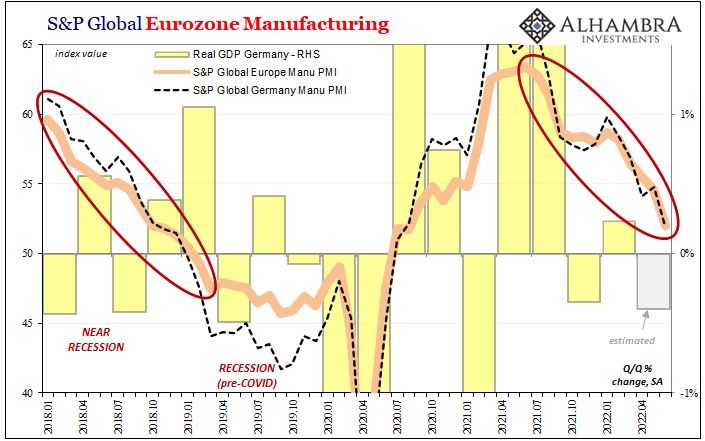

| S&P Global said its manufacturing PMI for Europe dropped sharply like its US counterpart, down to 52.0 in June from 54.6 May. Not only was that the lowest since August 2020, the output index fell below 50 for the first time since 2020 while the one for new orders fell further below the dividing line indicating the future direction is lower still.Their European composite fell below “omicron” afflicted January, though no pandemic panic to blame for this one.

That’s the thing about these indications; there are still those around who look at them like snapshots, focused on levels. In isolation, 52.0 for Europe doesn’t sound all that terrible. |

. |

| While it’s actually contraction territory, the more important and relevant emphasis is the trend and how quickly it has changed for the worse. |

. |

. |

|

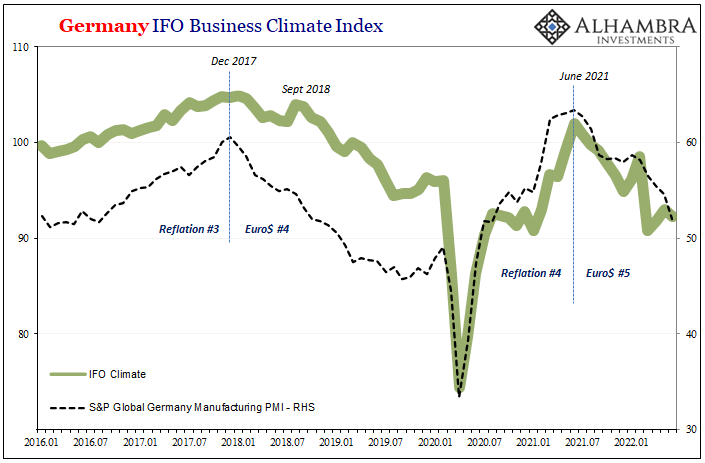

| The same goes for Germany, and not just S&P Global’s numbers on its bellwether manufacturing sector. Whether the most recent IFO numbers, or Industrial Production (and factory orders), you can clearly see how the economic “headwinds” developed, substantiated, then worsened from all the way back to the middle of last year.

Recession prospects have been rising for about a year already, so what we’re seeing in the data is merely confirmation of those. And while markets have been looking ahead for confirmation before now, they are from today looking ahead for confirmation of just how bad this thing might get going forward. To get some idea, just look at where all these datasets are pointing and ask just what might be out there which could stop these trends and turn them all the way around before it’s too late? Yeah, that’s why markets like eurodollar futures are betting near certainty on how it will be policymakers, not the economy, who performs the U-turn. |

. |

Just like last time, too.

Again, it’s not rate hikes. The media is only blaming them because they’ve confused consumer price action for economic strength which was just never there. In that sense, what’s different in June 2022 is how more in the mainstream are aware “something” is amiss.

From all around the world, data in every corner, market prices all over the place, it’s globally synchronized Euro$ #5 that’s just now starting to get nasty.

You Might Also Like

Sorry Chairman Powell, Even FRBNY Now Has To Forecast Serious and Seriously Rising Recession Risk

Sorry Chairman Powell, Even FRBNY Now Has To Forecast Serious and Seriously Rising Recession Risk

2022-06-20

At his last press conference, Federal Reserve Chairman Jay Powell made a bunch of unsubstantiated claims, none of which were called out or even questioned by the assembled reporters. These rituals are designed to project authority not conduct inquiry, and this one was perhaps the best representation of that intent. Powell’s job is to put the current predicament in the best possible light, starting by downplaying the current predicament.

Prices As Curative Punishment

Prices As Curative Punishment

2022-06-14

It wasn’t exactly a secret, though the raw data doesn’t ever tell you why something might’ve changed in it. According to the Bureau of Economic Analysis, confirmed by industry sources, US new car sales absolutely tanked in May 2022.

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.

2022-06-06

The fact that German retail sales crashed so much in April 2022 is significant for a couple reasons. First, it more than suggests something is wrong with Germany, and not just some run-of-the-mill hiccup. Second, because it was this April rather than last April or last summer, you can’t blame COVID this time.

President Phillips Emerges To Reassure On Growing Slowdown

President Phillips Emerges To Reassure On Growing Slowdown

2022-06-02

Just the other day, President Biden took to the pages of the Wall Street Journal to reassure Americans the government is doing something about the greatest economic challenge they face. Biden says this is inflation when that’s neither the actual affliction nor our greatest threat.

Another Month Closer To Global Recession

Another Month Closer To Global Recession

2022-05-26

We always have to keep in mind that the major economic accounts perform poorly during inflections. Europe in early 2018, for example, was supposed to have been just booming only to have run right into the brick wall that was Euro$ #4.

China Then Europe Then…

China Then Europe Then…

2022-05-08

This is the difference, though in the end it only amounts to a matter of timing. When pressed (very modestly) on the slow pace of the ECB’s “inflation” “fighting” (theater) campaign, its President, Christine Lagarde, once again demonstrated her willingness to be patient if not cautious.

Produzentenfenster Globale Rezessionsuhr

Produzentenfenster Globale Rezessionsuhr

2022-04-13

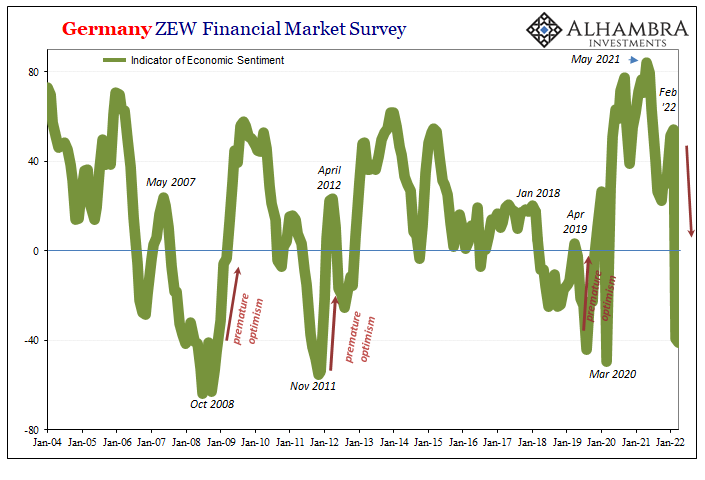

German optimism was predictably, inevitably sent crashing in March and April 2022. According to that country’s ZEW survey, an uptick in general optimism from November 2021 to February 2022 collided with the reality of Russian armored vehicles trying to snake their way down to Kiev. Whereas sentiment had rebounded from an October low of 22.3, blamed on whichever of the coronas, by February the index had moved upward to 54.3.

Goldilocks And The Three Central Banks

Goldilocks And The Three Central Banks

2022-04-07

This isn’t going to be like the tale of Goldilocks, at least not how it’s usually told. There are three central banks, sure, call them bears if you wish, each pursuing a different set of fuzzy policies. One is clearly hot, the other quite cold, the final almost certainly won’t be “just right.” Rather, this one in the middle simply finds itself…in the middle of the other two.Running red-hot to the point of near-horror, that’s “our” Federal Reserve.

Tags: Bonds,currencies,ECB,economy,Europe,Featured,Federal Reserve/Monetary Policy,Germany,inflation,Markets,newsletter,PMI,rate hikes,recession,sentiment